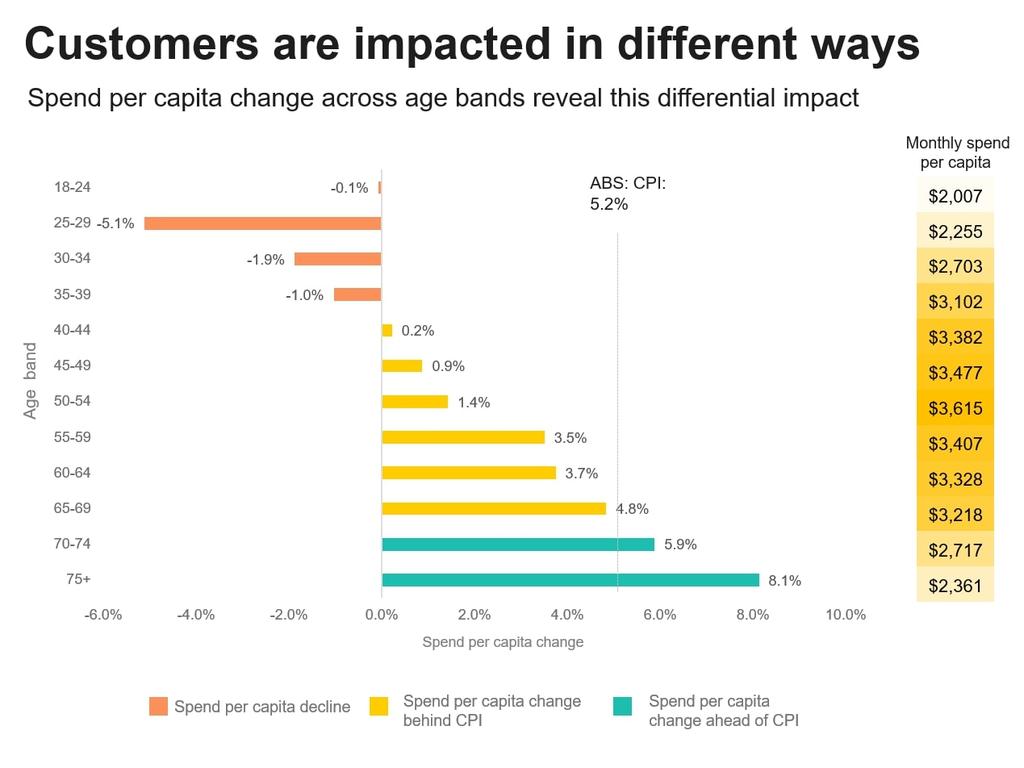

Households over 65 years are the only cohort, in general, to have more cash than debt.

“What that means when rates go up is that they get more interest income,” says Guesnon. “Everyone else throughout the income distribution has net debt, so they lose disposable income via higher interest paid.”

Those older households are also far wealthier than ever before. Across the age groups, the ratio of wealth to income is about 10. But for the 65-and-old group, that figure exceeds 20 and rising.

That means the benefit to income from a small increase in asset values or yields is far greater than any tightening of financial conditions, says Guesnon.

Another factor to consider is the fact that the pool of super savings is growing faster than the economy. Even if draw-down rates continue to average 4 per cent a year, an assumption UBS makes, super’s impact on consumption will only escalate, adding upward pressure to inflation.

Drawdowns from super are expected to increase from around 2.4 per cent of GDP in 2022-23 to 5.6 per cent of GDP in 2062-63.

Little wonder retirees are still in a mood to spend big, even as those with mortgages suffer. It’s a significant reversal from just a few years ago when ultra-low interest rates switched the dynamic.