Greetings everyone,

I've been carefully considering Entyr as an investment opportunity, and while the technology and value proposition are intriguing, certain aspects related to management decisions give me pause, despite the attractive low valuation.

I'm here to seek insights and constructive criticism on my analysis. Below are the areas where I've noticed some red flags:

Senior Personnel Changes:

Since Mr. Wheeley assumed leadership, there has been a significant turnover in upper management, including two CFOs in less than two years. While some changes are common, this level of turnover may raise concerns.

Includes time under Mr. Wheeley’s leadership

* Information gathered from ASX announcements and LinkedIn profiles

Senior Personnel Appointment:

Replacing the operations manager, who was praised for their extensive industry knowledge and experience*, with a person who’s only work experience is related to highschool education^ seems like a challenging transition. Going from an R&D plant to a commissioning plant without relevant experience could be difficult.

*Announced to the ASX 28/07/22

^ Information obtained from LinkedIn profile

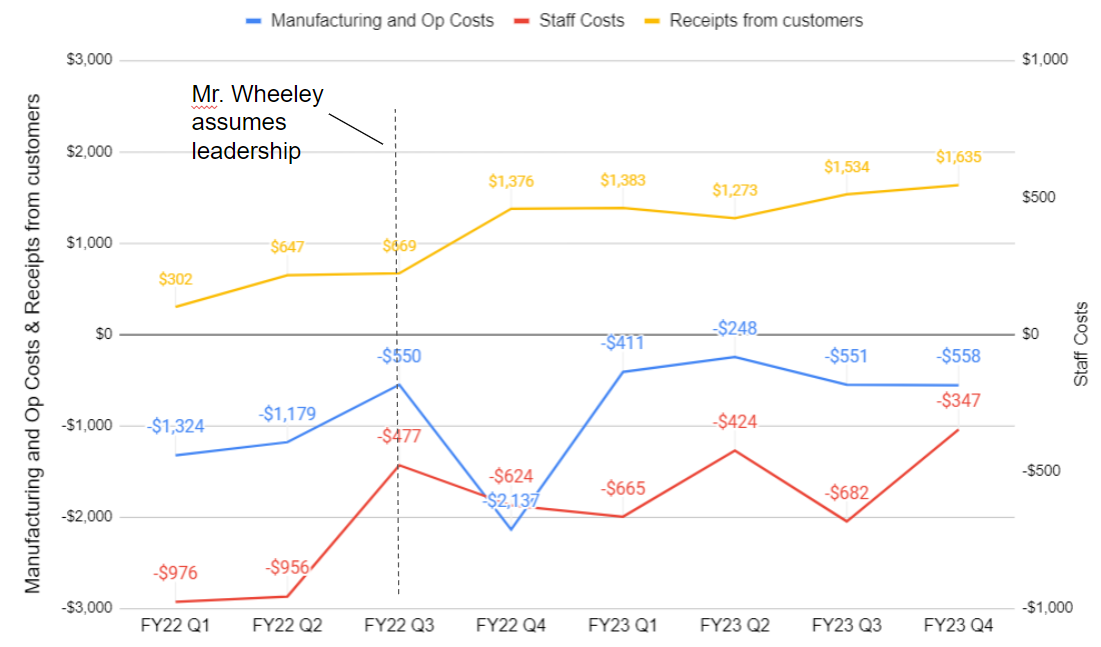

Cost Control:

There appear to be fluctuations in operational and staff costs despite stable customer receipts, suggesting potential issues in cost control or overall strategy*.

*Data obtained from 4Cs

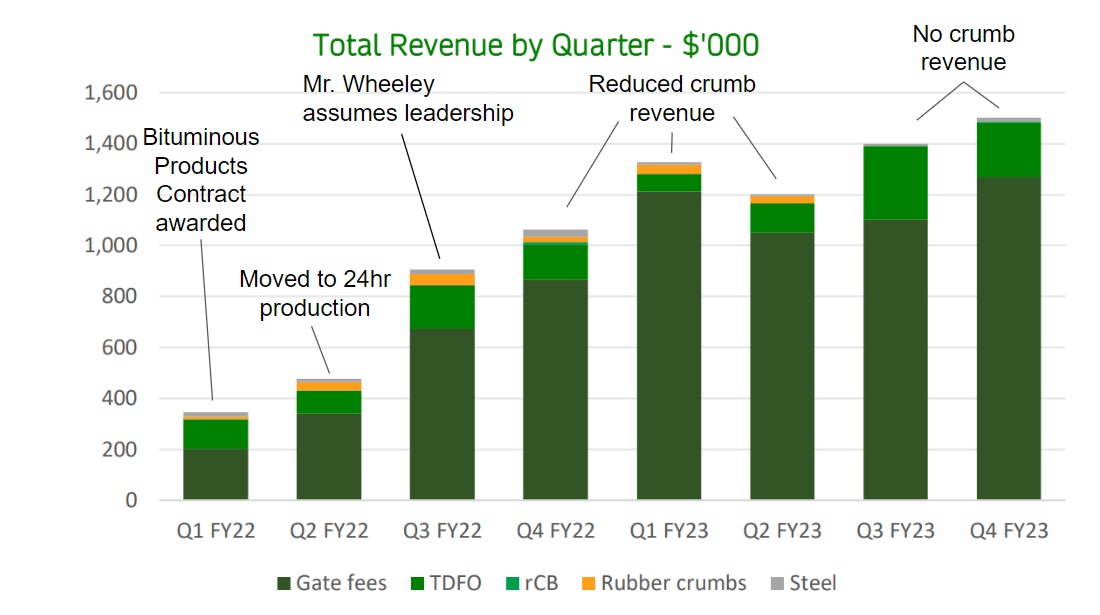

Crumbing Plant:

The crumbing plant investment (375k)^, the move to 24hr crumb production*, the contract from Bituminous Products ($750k/pa @$500/tonne)’, along with the projected $3.7m revenue pa seemed promising~. However, under Mr. Wheeley's leadership, volumes have decreased, and the situation seems unclear.

Graph from latest capital raise presentation dated 10/05/23

^ASX investor presentation 02/08/2021

*Announced to the ASX 29/10/21

‘ Announced to the ASX 31/08/20

~ASX investor presentation 02/08/2021

Compensation:

Mr. Wheeley's 2022 base salary of $425,000*, comprising 14.8% of 2022’s revenue ($2.87m), appears relatively high, and the lack of performance-based options adds another consideration. Mr. Wheeley’s compensation comprises a base salary and time-based options.

Assumed 2% increase in base salary per year

Option pricing and vesting dates obtained from FY 2022 report

*Announced to the ASX 01/12/21

Project Completion:

Entyr's leadership has encountered challenges in project completion, evident from the notable delays observed in the major projects since Mr. Wheeley assumed leadership, specifically in the projects named rasper, tank farm, and shredder

Rasper project started in June 2022

ASX Announcement Completion Date Change from original date

21st June 2022 End of July

28th July 2022 First week of August 1 week

24th August 2022 Middle of october 10 weeks

31st October 2022 In November 14 weeks (assumed middle)

31st January 2023 Commissioned in Dec 18 weeks

Tank Farm project started in Q4 2021

ASX Announcement Completion Date Change from original date

28th July 2022 In August

24th August 2022 End of August 2 weeks

31st October 2022 In November 12 weeks (assumed middle)

31st January 2023 Commissioned in Dec 16 weeks

Shredder

“Shredder project behind by approx. 8 weeks due to shipping and contractor delays”*

*Latest capital raise presentation dated 10/05/23

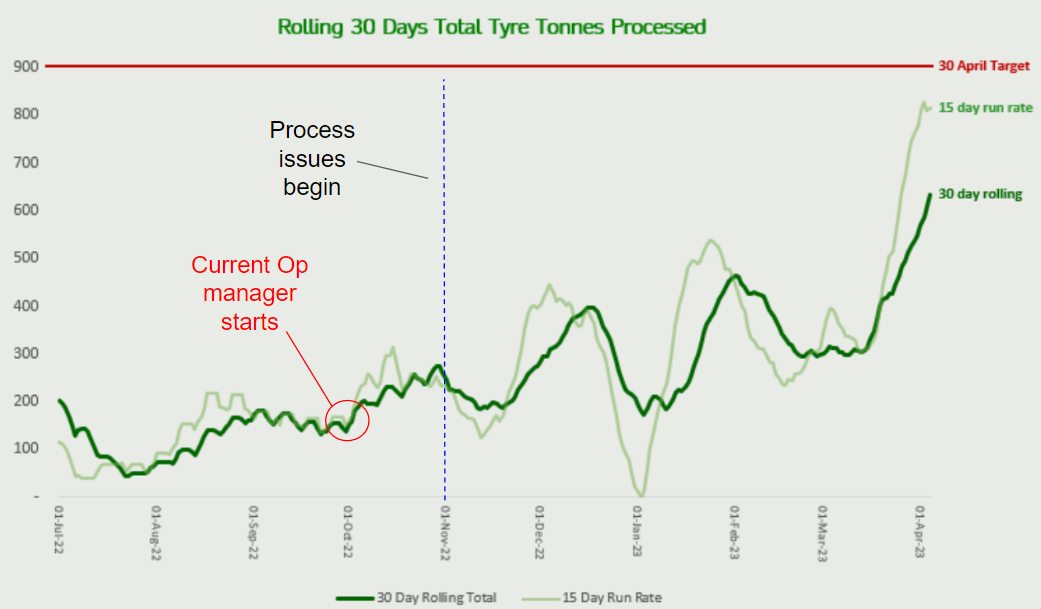

Processing issues

An observed divergence in the 15 and 30-day moving averages of tonnes processed, coupled with significant fluctuations in both, and the absence of April data, raises concerns about possible operational issues and machine reliability.

Graph from latest capital raise presentation dated 10/05/23

*Op manager start date from LinkedIn profile

Offices

It appears they have two sites: their primary location at U19/63 Burnside Road, Stapylton, Qld, which appears to have 2 office blocks on Google Maps, and another office situated in Ormeau, Qld, see below. While there's no explicit mention of them owning multiple offices or initiating a new lease, it's another red flag for me, especially considering the company's current financial status.

U19/63 Burnside road, Stapylton, Qld - Image from Google Maps

Entyr LinkedIn post

Conclusion

In conclusion, my analysis reveals several red flags under Mr. Wheeley's leadership, including personnel turnover, decision-making, cost control, infrastructure, compensation, project timelines, and operational performance.I welcome your comments and insights, as I'm eager to see if there's anything I might be overlooking. However, based on the current situation, I find it difficult to invest in a leader with these concerns, and it seems recent share price movements indicate others share similar sentiments.

Leadership Concerns

Add ETR (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

0.7¢ |

Change

0.000(0.00%) |

Mkt cap ! $13.88M | |||

| Open | High | Low | Value | Volume |

| 0.0¢ | 0.0¢ | 0.0¢ | $0 | 0 |

| ETR (ASX) Chart |

Day chart unavailable