The lithium bear market marches on and things might be set to get worse. Alita Resources (formerly known as Alliance Mineral Assets) entered into a trading halt this week, and there are growing concerns that the operator of the Bald Hill Mine (which produces spodumene concentrate), located in Western Australia, could be "the first casualty".

Source: Australian Financial Review

Source: Australian Financial Review

As it pertains to lithium oversupply, at least so far in 2019, Morgan Stanley has been right on the money with their original call from February 2018.

Lithium Prices Keep Going Down

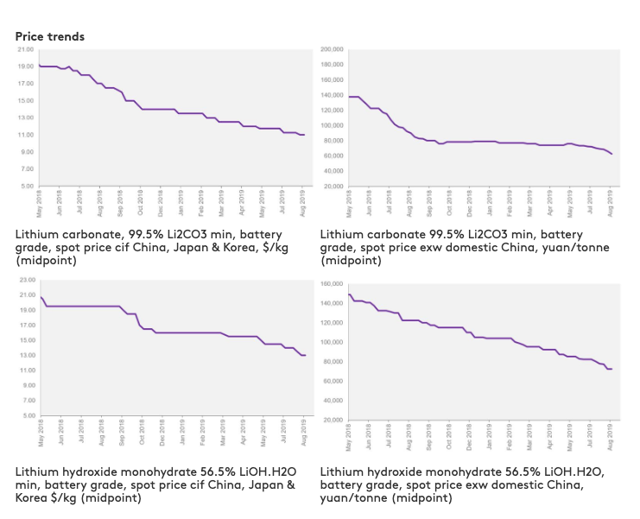

The trend has certainly not been a friend of lithium's over the past year or so, as the following price charts will show (dating back to May 2018).

Source: Metal Bulletin

Source: Metal Bulletin

In regards to where lithium prices are at the moment, Fastmarkets notes the following:

Further, Fastmarkets offered up a few thoughts, in regards to the struggles going on at Alita Resources:

As noted in the last paragraph above, in regards to lithium prices, the decline in spodumene concentrate pricing down to $585-650/t range has to be especially concerning for market producers, given the fact that, even in a bull market, this feedstock material used for secondary processing to produce lithium chemicals (e.g., lithium carbonate, lithium hydroxide) was never really considered a high-margin product to begin with.

Most recently, Mineral Resources (OTCPK:MALRF) made an announcement disclosing the pricing they were receiving for their 6% spodumene concentrate produced at their Mt Marion Lithium Mine, which shows prices have fallen to $608.95/t for Q3 (compared to $682.38/t in Q2).

Source: Mineral Resources July 2019 Press Release

Source: Mineral Resources July 2019 Press Release

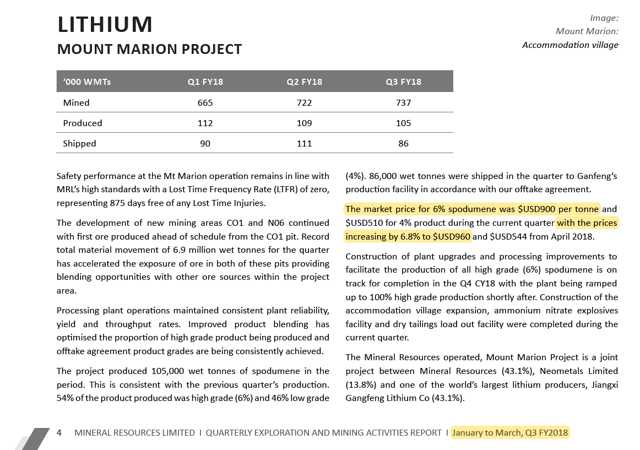

For context on just how badly spodumene prices have fallen over the last year, the following slide shows that Mineral Resources was able to sell the same 6% spodumene concentrate produced at Mt Marion (referenced above) for $900-960/t during Q2-Q3 of 2018.

Source: Mineral Resources March 2018 Quarterly Activities

Source: Mineral Resources March 2018 Quarterly Activities

Now, we are talking about 6% spodumene concentrate selling closer to ~$600/t, and as noted by Fastmarkets earlier, the downtrend looks to still be very much intact as prices in the sub $600/t range are now being cited.

The Trend is Not Your Friend

Due to the various prevailing headwinds impacting the lithium market at the moment, and as I noted in another article, both industry leading producers Albemarle (ALB) and Livent (LTHM) have gone on record saying that they aren't expecting the supply vs. demand dynamic to really tighten up until possibly sometime in 2020, which as a consequence, could cause the current price slump to carry on.

In the case of spodumene concentrate, the glut of excess supply came in the form of "too many" new hard rock mines opening up in recent years.

Source: PV Magazine

Source: PV Magazine

As such, as tempting as it may be to jump into the fray right this very moment due to the decimation seen in share prices across the universe of lithium stocks (particularly among spodumene producers who have been hit the hardest), speculators who insist on playing should know that the chances of "catching a falling knife" (which has been the recurring theme for lithium stocks over the last ~1.5 years) could still very much be in play here.

The trend is not your friend.

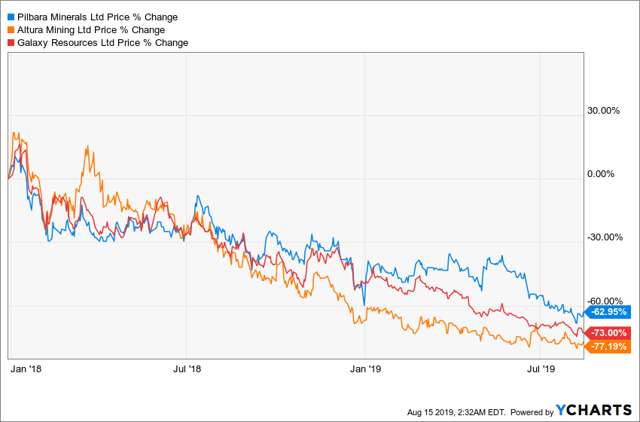

For example, in Australia, some of the top spodumene producers have seen their share prices absolutely annihilated, since January 1, 2018.

In terms of risks, speculators need to be keenly aware that in a "low price" market environment, the ability for a spodumene producer to be able to generate positive free cash flow is something that is a lot easier said than done.

Slow and Difficult Ramp-Ups

To be even more specific, it would seem to me that the companies most at risk in the current landscape are the new up-and-coming spodumene producers, as companies like Pilbara Minerals and Altura Mining have demonstrated over the last year, commissioning a new mine up to nameplate capacity is a non-trivial task.

It will take a lot of time, and then some more.

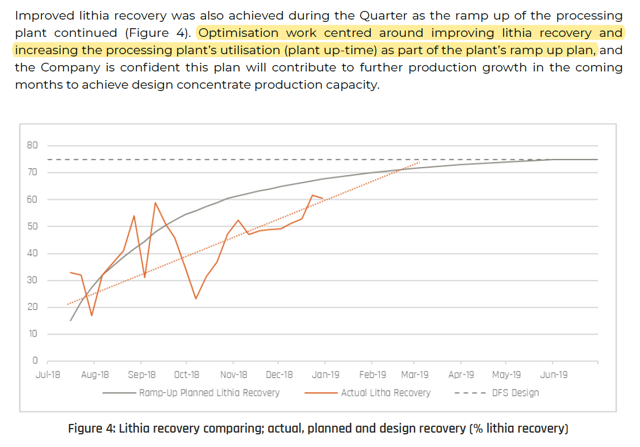

As shown below, Pilbara Minerals began spodumene concentrate production at their Pilgangoora Lithium Mine, located in Western Australia, around July 2018, and just trying to meet the "DFS Design" target for recoveries (75%) has been a non-linear work-in-process (with volatile spikes exhibited in both directions) since the beginning.

Source: Pilbara Minerals December 2018 Quarterly Activities Report

Source: Pilbara Minerals December 2018 Quarterly Activities Report

As of the latest March 2019 Quarterly Activities Report, it looks like recoveries of Pilbara's Pilgangoora Lithium Mine have still "only" reached ~65% or so, which is still short of the "DFS Design" target of 75%.

Source: Pilbara Minerals March 2019 Quarterly Activities Report

Source: Pilbara Minerals March 2019 Quarterly Activities Report

Operating a plant at non-optimized levels will inevitably lead to higher operating costs, and in some cases, more capital will need to be deployed in order to remedy the situation. Again, for speculators, the key risk is that free cash flow generation will be difficult (if not impossible to come by), which can start to quickly drain the cash balance on a financial statement.

Strapped for Cash

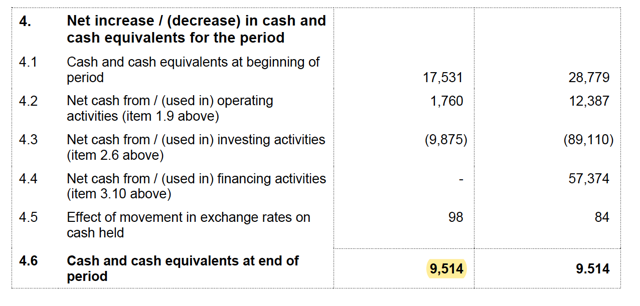

For example, at the end of Q2 2019, Altura Mining, who is the operator of the Altura Lithium Mine, located in Western Australia, had ~A$9.5 million of cash in the bank.

Source: Altura Mining June 2019 Quarterly Cash Flow Report

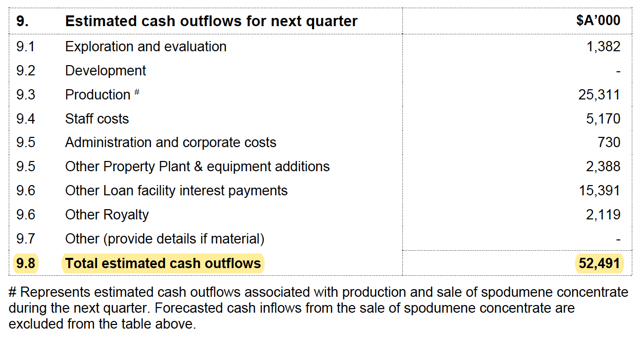

And because a mine in production (e.g., Altura's Lithium Mine) will always have fixed costs associated with it, this could lead to situations where the next quarter's estimated cash outflows > cash balance at the end of a reporting period, like in the case for Altura Mining.

Source: Altura Mining June 2019 Quarterly Cash Flow Report

Source: Altura Mining June 2019 Quarterly Cash Flow Report

Which in turn can prompt more (dilutive) financing events, that can't help but to erode away the equity value of shares already held by longer-term shareholders.

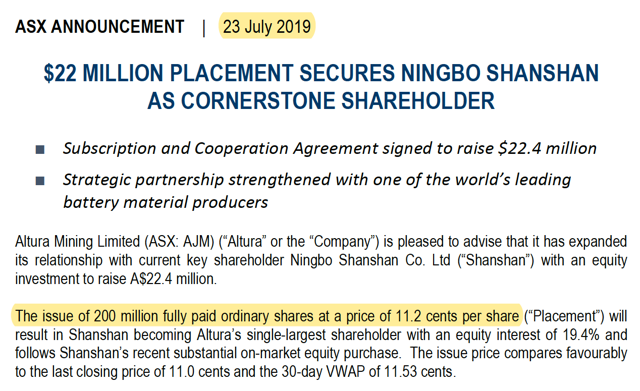

For instance, Altura Mining raised A$22.4 million in July.

Source: Altura Mining June 2019 July 2019 Press Release

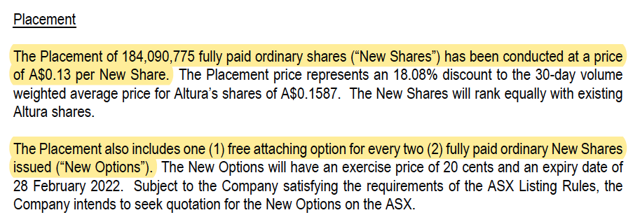

However, worth noting, the most recent capital raise came on the heels of a previous one from earlier this year, when Altura Mining raised A$28 million, back in February.

Source: Altura Mining June 2019 February 2019 Press Release

Over time, the lack of positive free cash flow coming in to pay for expenses will only lead to more pain (covered in the next section), with no gains to show for it.

Endless Dilution

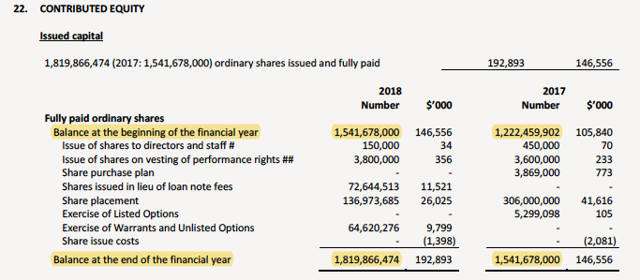

The following slide highlights just how badly a company like Altura Mining has been diluted down in recent years.

Source: Altura Mining 2018 Annual Report

- Start of 2017: ~1.2 billion shares issued

- Start of 2018: ~1.5 billion shares issued

- Start of 2019: ~1.8 billion shares issued

Things have only gotten worse this year, as collapsing lithium prices (covered previously) have compressed/eliminated essentially any profit margins.

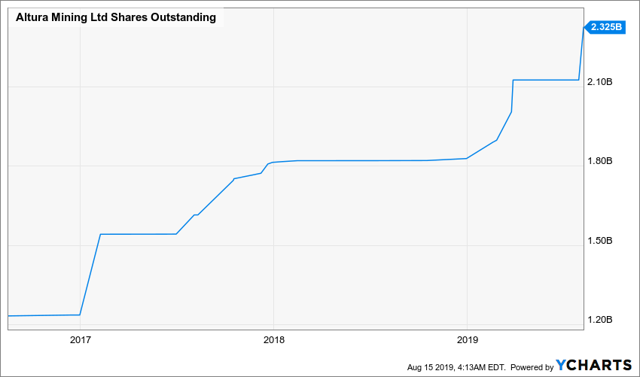

Now, more than halfway through 2019, and the share count for AJM.AX/ALTAF has swelled to over 2.3 billion shares issued.

Which will no doubt make the prospect of trying to climb all the way back up to previous all-time highs that much more difficult of a task.

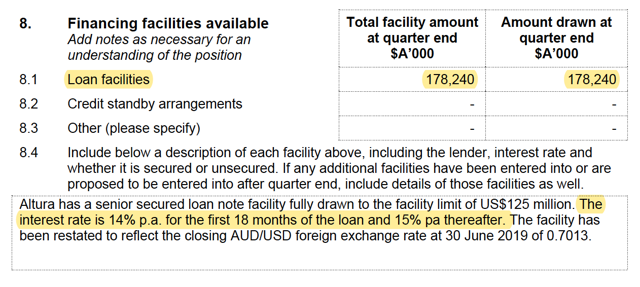

Further, if the risk of excessive dilution wasn't scary enough, for some companies which took on onerous debt financing (e.g., 14-15% interest rates), such as Altura Mining, there's also the even scarier proposition of having to pay it back (when you're already struggling mightily to generate any kind of positive free cash flow).

Further, if the risk of excessive dilution wasn't scary enough, for some companies which took on onerous debt financing (e.g., 14-15% interest rates), such as Altura Mining, there's also the even scarier proposition of having to pay it back (when you're already struggling mightily to generate any kind of positive free cash flow).

Source: Altura Mining June 2019 Quarterly Cash Flow Report

Which, if there are any additional major operational hiccups/issues down the road, could lead to some rather disastrous consequences.

Risk vs. Reward

As such, speculators who insist on dabbling in shares of spodumene producers at this juncture need to be on high alert because the risks are sky high at this time.

As cautioned by Fastmarkets:

The above sentiment is not lost on companies such as Pilbara Minerals which has been actively looking into partnering up with other third parties to get into the downstream lithium chemical business (e.g., selling lithium carbonate, lithium hydroxide), which on paper should do wonders for both expanding profit margins and mitigating risks against price volatility.

It should be worth noting at this time that the lithium industry is a nascent one, so speculators should expect to see a lot of drastic changes over the coming years, as companies work to figure things out and evolve.

Still, at this point in time, quite frankly, in my own humble opinion, the juice simply isn't worth the squeeze going down the path of speculating on spodumene producers; the risk vs. reward isn't all that compelling when even near-flawless execution likely won't lead to ample positive free cash flow generation at these low lithium prices (but any significant slip up could lead to a catastrophic outcome).

With that said, another viable alternative for eager speculators looking to go the spodumene producer route would be to turn to companies who have especially strong balance sheets and should in theory be better able to stand up and weather the storm.

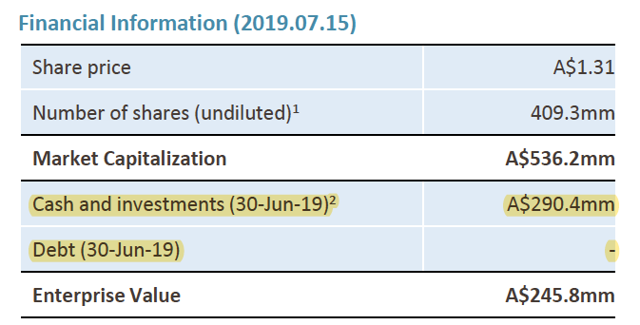

For example, Galaxy Resources currently has ~A$290 million of cash and zero debt on its books.

Source: Galaxy Resources July 2019 Corporate Presentation

Source: Galaxy Resources July 2019 Corporate Presentation

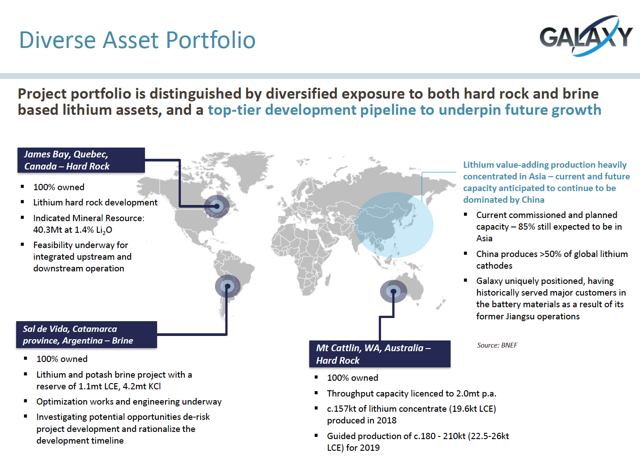

Further, the company controls 3 separate "core" lithium assets (two of which will be focused on selling much higher margin lithium carbonate/hydroxide), which presents a way for speculators to hedge/diversify.

Source: Galaxy Resources July 2019 Corporate Presentation

Source: Galaxy Resources July 2019 Corporate Presentation

Global X Lithium and Battery Tech ETF (LIT)

Arguably, an even more prudent approach for lithium bulls who are after "deep value" opportunities at this time would be to construct their own personal ETF, to hedge risks, or turn to a well diversified product, such as the Global X Lithium and Battery Tech ETF (LIT), which is anchored by industry leading producers Albemarle and Sociedad Química y Minera de Chile (SQM).

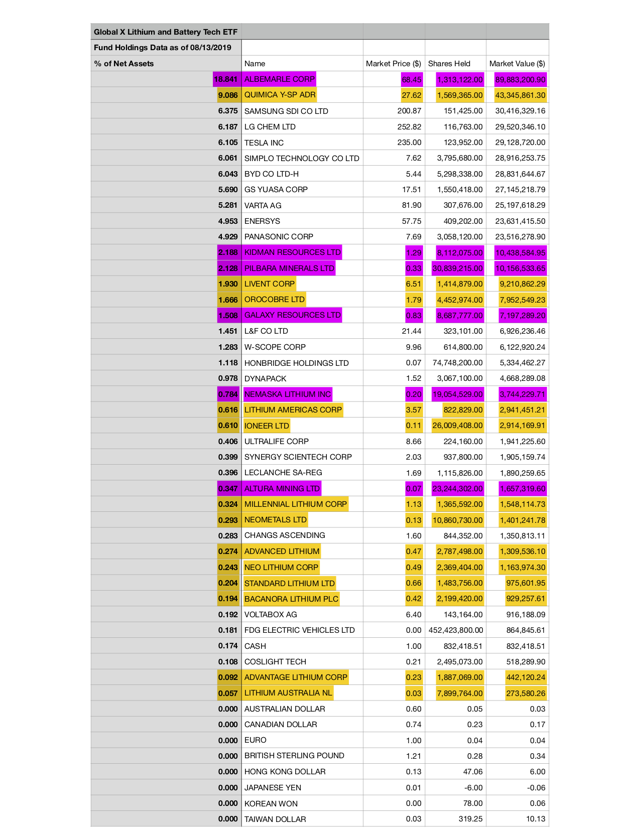

The following table shows the individual holdings that make up the LIT ETF, with companies involved in lithium mining/processing/extraction highlighted in orange, while spodumene-focused mining companies are highlighted in magenta.

Source: Global X Lithium and Battery Tech ETF

Source: Global X Lithium and Battery Tech ETF

Although the Global X Lithium and Battery Tech ETF may not be a perfect lithium fund, in recent years, the allocation/weighing has certainly increased in recent years to account for more mining companies (especially junior ones, who in theory should provide stronger leverage to rising lithium prices).

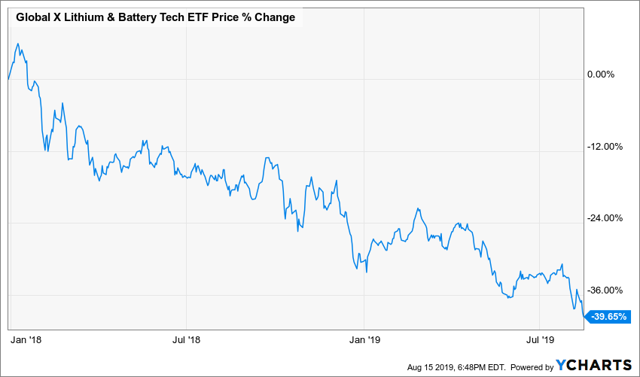

Shares of LIT are currently trading at $23.39/share. It's now sitting at a level not seen since before 2017.

Over a longer time horizon, we can see that shares of LIT are now down -39.65% since January 1, 2018.

Now, because shares of LIT are trading at its lows for the year (also at its ~3 year low) and is a well diversified product, in my eyes, it currently offers a better risk vs. reward proposition than going with individual lithium stocks, particularly spodumene producers.

Now, because shares of LIT are trading at its lows for the year (also at its ~3 year low) and is a well diversified product, in my eyes, it currently offers a better risk vs. reward proposition than going with individual lithium stocks, particularly spodumene producers.

To circle back, Alita Resources is currently in a trading halt, and things don't look good (the company has struggled for a while now trying to turn a profit in an environment where lithium prices have been in free fall). However, the industry on the whole may need to start seeing some of the more marginal spodumene producers start to close up shop before sentiment towards lithium (and lithium stocks) can start to improve again.

For the time being, the narrative (and evidence) seems to suggest that the lithium market (especially spodumene) is in a state of oversupply, so the relentless lithium bear keeps on marching on.

Currently, it does not look like brighter days are on the horizon, so it's time to batten down the hatches and wait for this severe storm to pass through.

Spodumene producers are having to continue to fight an uphill battle, so for now, the sidelines seem like a much safer place to be.