Did FDA just approve Exondays 51 because of no other drugs available for DMD?

Exondays 51 ($300,000-per-year drug) has still not been established “clinical benefits” but achieved USD$84m revenue in a quarter.

@Davisite, what’s your opinion on ATL1102?

Thanks mate.

Sarepta: Risks Are Priced In, Valuation Is Compelling

Sarepta market cap: USD$6.3B

The company's most immediate pipeline is focused on the

Duchenne Muscular Dystrophy (DMD) disease, a rare genetic disorder that causes progressive weakness and wasting (atrophy) of the muscles. DMD is caused by an absence of dystrophin, a protein that protects muscle cells. The absence of dystrophin in muscle cells leads to significant cell damage which ultimately causes muscle cell death and fibrotic replacement.

The company's first commercial product

Exondys 51/Eteplisen was granted accelerated approval by the FDA in 2016. Exondys is considered a viable treatment for patients with a confirmed mutation of the dystrophin gene amenable to exon 51 skipping, which is roughly

13 percent of the population with DMD. Although the FDA granted accelerated approval in 2016, a clinical benefit of Exondys 51

has not been established.

Fast-forward nearly three years later, in 2019 a clinical benefit has still not been established. In simple terms "clinical benefit" means a positive effect of a therapeutic intervention. By approving Exondys, the FDA is basically saying that the treatment can be considered safe but its effectivity is unknown at this point. Therefore continued approval may be contingent upon verification of a clinical benefit in a confirmatory trial. Given the fact that DMD is a rare disease, I can see why the FDA decided to fast-track the approval for Exondys, however, it is unknown how much latitude the FDA will continue to give to the company.

The company is seeking accelerated approval for two other RNA related treatments (Golodirsen and Casimersen) in 2019 and 2020. Golodirsen and Casimersen both use the same PMO chemistry and exon-skipping technology as Eteplirsen. Last August, the company received a "

complete response letter" from the FDA citing two concerns; i) the risk of infections related to intravenous infusion ports and ii) renal toxicity seen in pre-clinical models of Golodirsen and observed following administration of other antisense oligonucleotides.

While the FDA's concerns are valid, there are two flaws with this line of thinking. First, the risk of renal toxicity was observed in doses that were 10x higher than the dose administered in the clinical studies. Staying within the recommended therapeutic dosage is extremely important as toxicity may occur at doses exceeding this. Even your everyday over-the-counter medications can have toxic adverse effects when taken beyond the recommended dose, so this should not be a major impediment to approval. Second is that risk of infection is a typical concern for most drugs delivered via intravenous infusion ports (such as chemotherapy and some antibiotics). Given these two facts, it is confusing as to why the FDA refused to fast-track Golodirsen given that it has a similar, but not identical, mechanism of action as Eteplirsen. One can speculate that the overhang of the lack of a confirmatory trial to establish clinical benefit for Eteplirsen is at least partially driving the FDA's concern.

Valuation

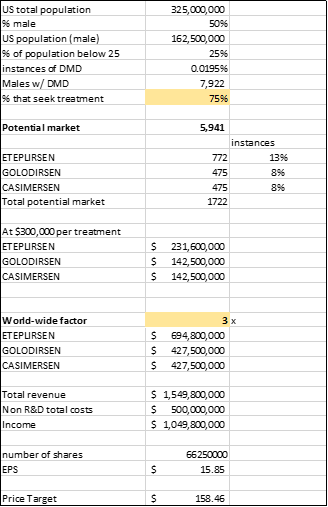

I've crunched some numbers to get some idea of the total revenue for Sarepta's current pipeline. So we know that the US has a population of roughly 325 million and that DMD affects mostly male and occurs

15.9 to 19.5 per 100,000 live births. I am assuming that 75% of people with DMD seek treatment with Sarepta and we know that Eteplirsen, Golodirsen, and Casimersen treat 13%, 8% and 8% of the DMD population respectively. At

$300,000 treatment price and a world-wide factor of 3x, this translates to a revenue of about $700 million for Eteplirsen and $420 million each for Golodirsen and Casimersen. (Note: I've defined a world-wide factor to account for the fact that the treatments are available not just in the US, I've given Sarepta a lower factor given that the cost of treatment is extremely expensive so a limited population worldwide could afford such a treatment).

I wanted to get an idea of the current value of Sarepta strictly limiting it to Eteplirsen, Golodirsen, and Casimersen. So I took my total estimated revenue of $1.5 billion subtracted $500 million which represents non-R&D related total costs and arrived at a Net income of roughly $1 billion. I got my estimated non-R&D related total costs by doubling Sarepta's 2018 non-R&D related total cost. Using a P/E of 10 and by changing my estimate of the percentage of the population that would seek treatment, I was able to arrive at a price range of 80 - 158.

Source: Author's calculations

Taking the mean of that price range gives us a price target of about 120 for Sarepta which translates to a 41% upside. The recent downturn of the stock has given us a buying opportunity as the stock has practically lost half its value from its July highs of 150. In my view, it is most likely that Golodirsen will get FDA approval as the concerns raised in the CRL are relatively minor. The bigger overhang though is the continued lack of a clinical benefit test associated with Eteplirsen. My guess is this issue will pop up once again once Casimersen seeks FDA approval. In my calculations, I've only taken into account Eteplirsen, Golodirsen, and Casimersen exclusively, therefore, the overhang to the rest of Sarepta's pipeline has already been factored in. I believe the risks are already baked into the stock price thus Sarepta is a buy in my books.

https://seekingalpha.com/article/4291885-sarepta-risks-priced-valuation-compelling

(20min delay)

(20min delay)