Summary

Auteco Minerals reported a maiden resource estimate Monday at its new Pickle Crow Project, where it can earn up to 80% of the project.

The maiden resource estimate has defined nearly 1 million ounces of high-grade gold with a significant amount of existing infrastructure in place.

While this is an exceptional start for Auteco, the valuation is no longer that attractive at A$0.175.

Based on the relative overvaluation to peers, I believe investors would be wise not to chase the stock here above A$0.175.

It's been an exciting start to the year for the gold explorers, with several names putting up triple-digit returns, and massively outperforming the gold (GLD) price. Auteco Minerals (OTC:MNXMF) is one of the top-performing gold stocks in the sector, up 1500% year-to-date, after turning in a lifeless performance the past several years. The catalyst for the reinvigorated interest in the stock is new appointments to the board of directors and the acquisition of an earn-in agreement on the Pickle Crow Project just east of the Red Lake District in Ontario. However, while the company has defined a substantial resource here of nearly 1 million ounces of gold, the valuation is no longer attractive at over US$150 million. Therefore, I believe investors would be wise not to chase the stock here at A$0.175 after a more than 1500% run in less than six months.

(Source: Company Presentation)

Auteco Minerals released a maiden resource estimate at its Pickle Crow Project just east of Red Lake, Ontario, and the junior miner has defined a substantial high-grade resource of nearly 1 million ounces. The initial resource estimate completed at the project came in at 830,000 ounces of gold at an average grade of 11.6 grams per tonne gold, an exceptional grade in line with many high-grade projects in the area like the past-producing Madsen and Red Lake mines. It's worth noting that Pickle Crow benefits from existing infrastructure, including 38 kilometers of underground development and two 1,000 meter shafts.

The story is a little reminiscent of an early stage Pure Gold Mining (OTCPK:LRTNF) as it was just seven years ago that Pure Gold picked up a 1.2 million ounce resource at 10 grams per tonne gold with an existing mill and shaft just 300 kilometers west at Madsen. Thus far, the resource estimate is undoubtedly a step in the right direction to build out a similar storyline. The recent board additions should increase investors' confidence in expanding this resource. Before digging into what makes the board special, and the potential for resource expansion, let's take a quick bird's-eye view of the Pickle Crow project below:

(Source: Company Presentation)

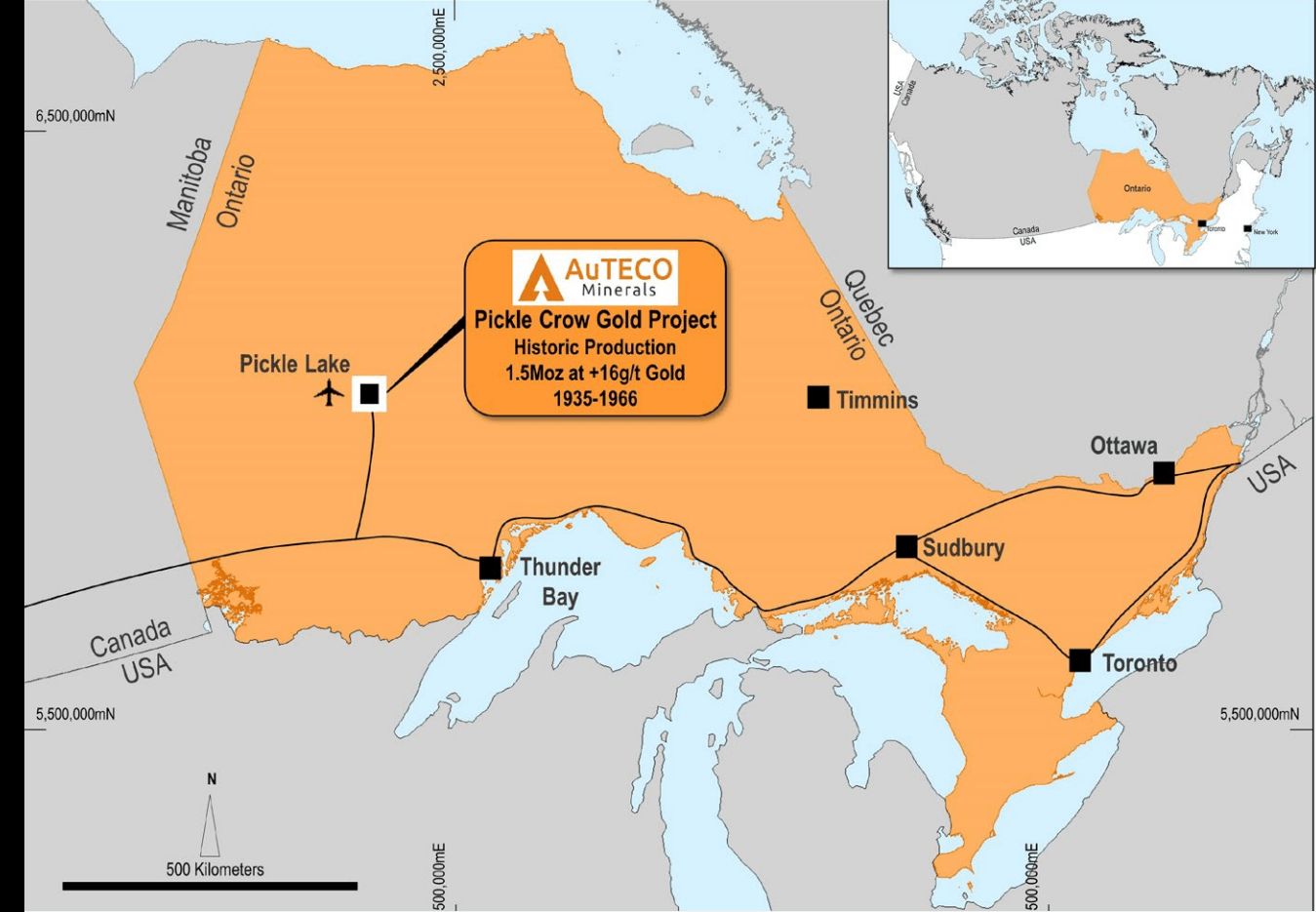

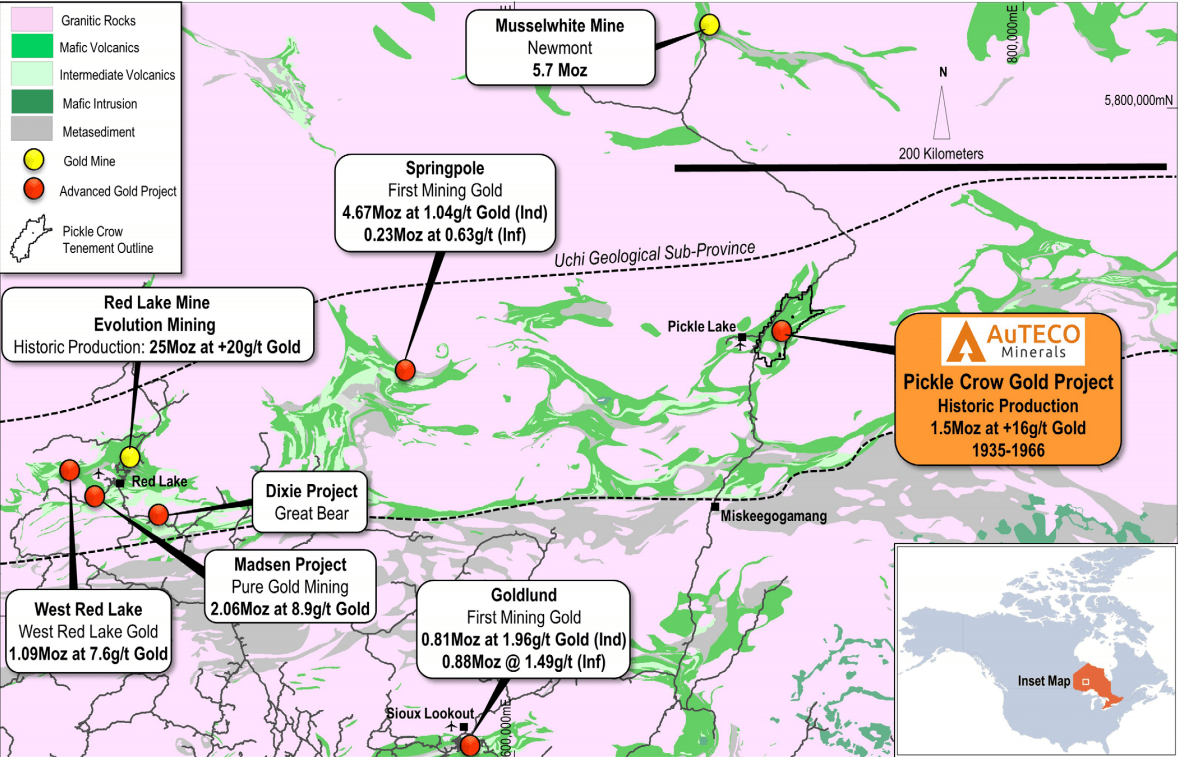

As we can see from the above map, Auteco Minerals' Pickle Crow Project is located in Ontario, Canada, one of the best addresses for mining, right near Pickle Lake, which is east of the prolific Red Lake District. The district is known for significant gold endowment with several million-ounce gold projects in the area, including Evolution Mining's (OTCPK:CAHPF) recently acquired Red Lake Mine (formerly held by Goldcorp), First Mining's Springpole Project, and the newest discovery in the district, Great Bear's (OTCQX:GTBAF) Dixie Project. Auteco Minerals has secured a 320 square-kilometer land package in the region, where we previously saw historical gold production of over 1.5 million ounces between 1935 and 1966.

Due to low gold prices at the time, any material below 8 grams per tonne gold was left behind given their 8 gram per tonne cut-off, meaning that there could be strong potential for a significant resource that's slightly lower grade than past grades of 16 grams per tonne gold. This is the same model that Skeena Resources (OTCQX:SKREF) employed, acquiring Barrick Gold's (GOLD) past-producing Eskay Creek Mine which also had a very high cut-off grade. Skeena has since found 4 million medium-grade ounces left behind. Let's take a closer look at the project and recent resource estimate below:

(Source: Company Presentation)

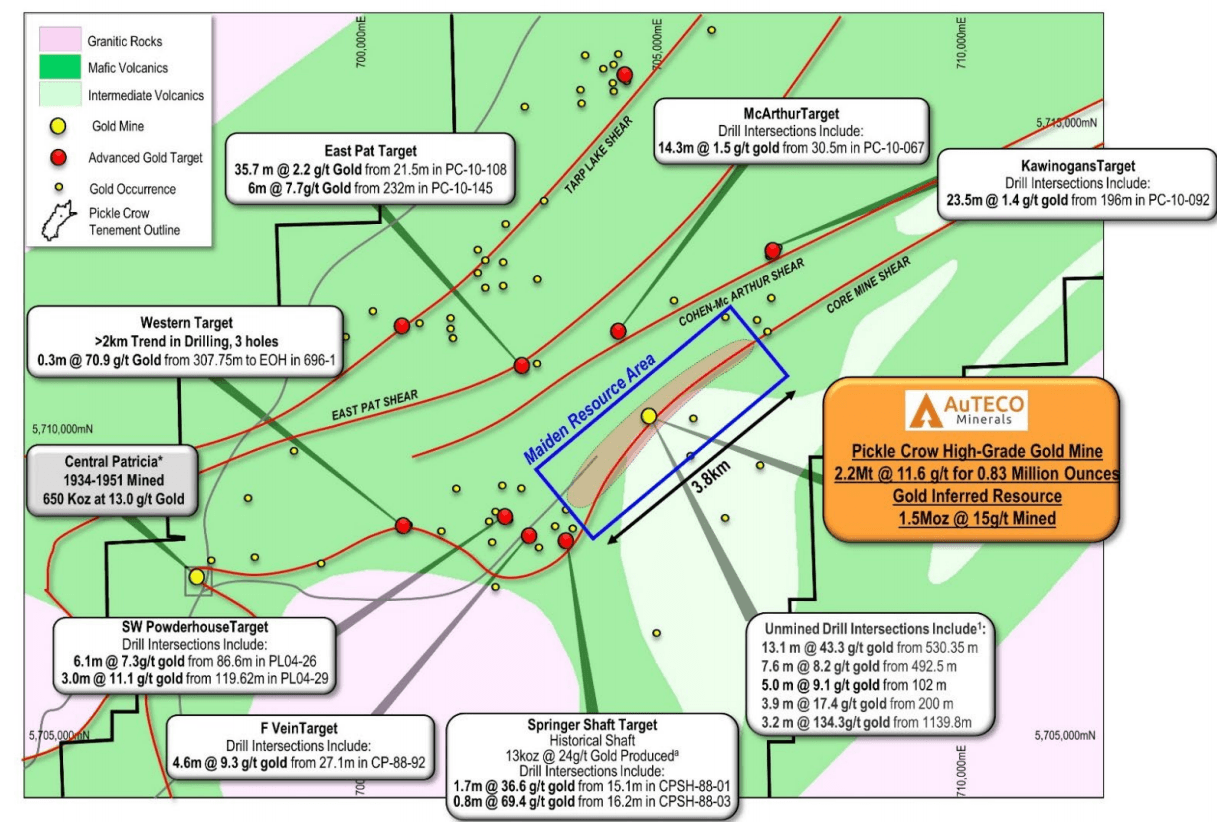

If we take a look at the below long section, we can see that the maiden resource area has been delineated over a 3.8-kilometer strike length, but several untested targets are surrounding the deposit in each direction. The East Pat Target, which is directly northwest of the resource area, looks to be a potential bulk tonnage target with a historical intercept of 35.7 meters of 2.2 grams per tonne gold. Meanwhile, the Southwest Powderhouse Target is near the Central Patricia Zone, where we saw over 600,000 ounces of historical gold production and a historical intercept here of 6.1 meters at 7.3 grams per tonne gold.

These are just two of several targets within a 10-kilometer radius of the mine, and one or two should likely yield some solid results. However, it's also worth noting that there are un-mined intercepts at the current resource area, with 13.3 meters of 43.3 grams per tonne gold and 3.2 meters of 134.3 grams per tonne gold. Therefore, there's certainly a reasonable possibility that Auteco could build on the current 830,000-ounce resource here with the current drill program. For now, the company has begun with two drill rigs on the property to test new targets.

(Source: Company Presentation)

While a prospective land package is excellent, it's the team that's directing the drill bit and mapping out targets that ultimately determines whether a junior miner will be successful. Fortunately, we saw the addition of Bellevue Gold (OTCPK:BELGF) Managing Director Steve Parsons to the board recently, who has led the team to make major discoveries near the past-producing Bellevue Gold Mine in Australia. Also, Bellevue Gold Chairman Ray Shorrocks joined the board earlier this year, and most importantly, Sam Brooks, Bellevue's Chief Geologist.

Given that we have more than half of the Bellevue Gold team with a US$500 million market cap and incredible share price performance as a direct result of their successful delineation of the Bellevue Gold Project, this bodes well for Auteco's drilling success. However, while I have high hopes for the project, the stock looks like it's already pricing in a discovery before it's happened here, with the valuation climbing to US$155 million this week. This is not ideal for a smaller explorer with a sub-1-million ounce resource, and I would argue that valuation would become a headwind at A$0.18. Let's take a closer look below:

(Source: Author's Photo)

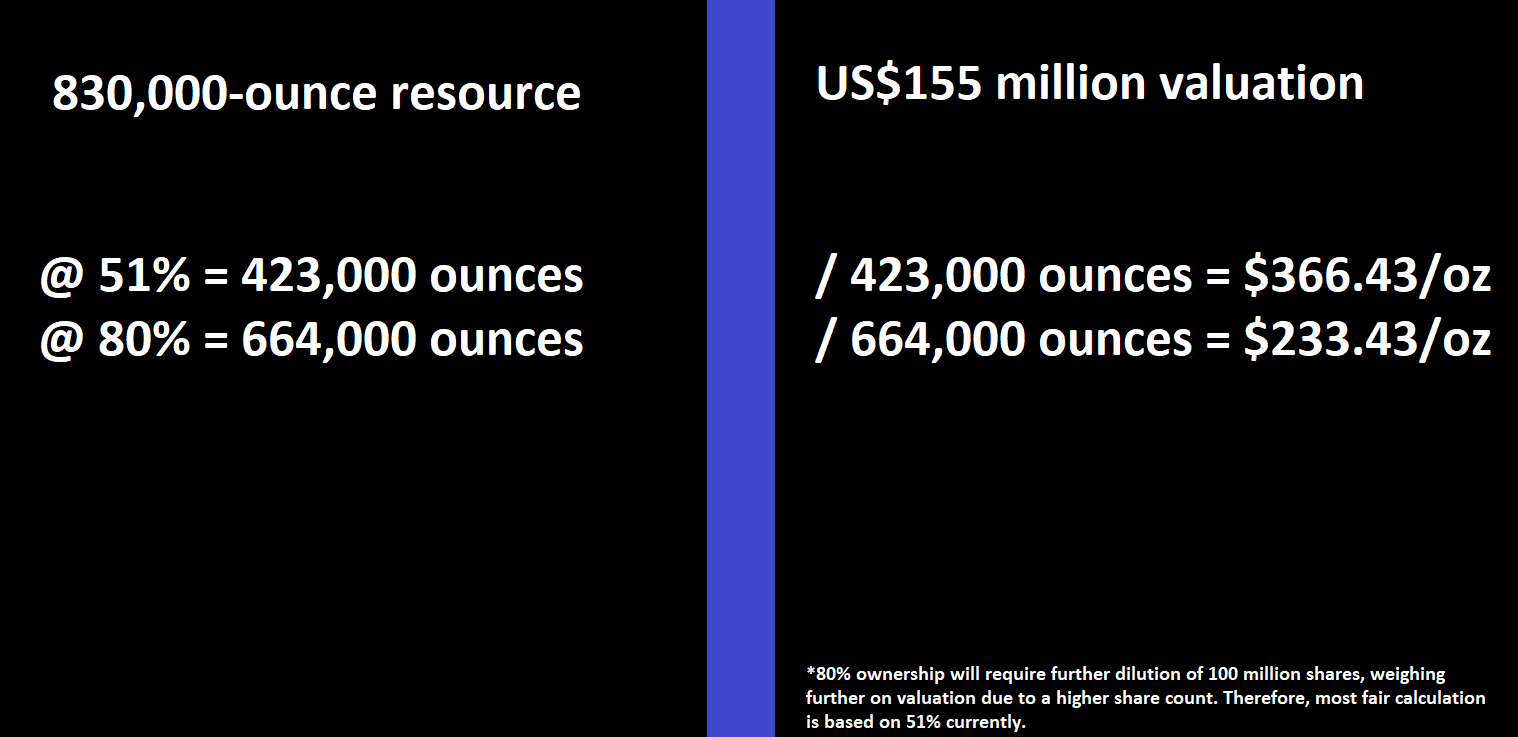

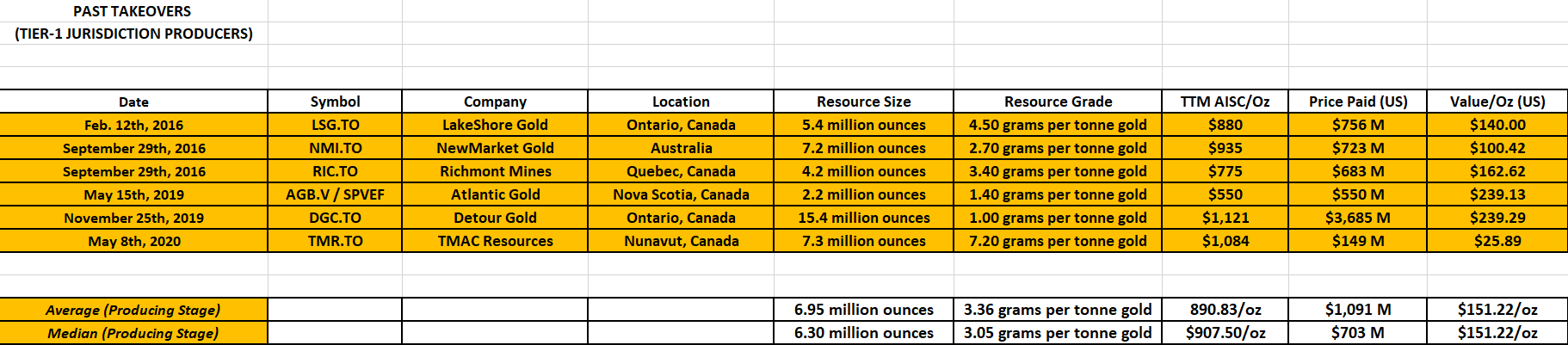

Based on Auteco's 1.3 billion shares outstanding and a share price of A$0.17, the company is currently valued at A$221 million [US$155 million], a hefty price to pay for an early exploration stage company that's just begun drilling. While Auteco has a robust resource of 823,000 ounces, it's important to note that they've only earned 51% of the project to date, with just 423,000 ounces attributed to them. This means that the company is currently valued at US$366.43/oz, a figure that is well above the US$125.00/oz paid for Tier-1 explorers with high-grade resources and prior infrastructure, and well above the US$150.00/oz paid for gold producers in Tier-1 jurisdictions. (Source: Author's Chart)

To put this in perspective, Bellevue Gold's enterprise value per ounce is US$200.00/oz with a 2-million ounce resource that's higher-grade and much closer to the development stage. Therefore, the current valuation is getting a little frothy above A$0.17. Even if we give Auteco the benefit of the doubt and assume 80% ownership of the project, which is the maximum under the earn-in agreement, this still values Auteco at US$233.43/oz double where high-grade explorers are currently valued. This valuation headwind is not to point out that the stock will drop 50%, or that the stock can't go higher, it's merely to point out that investors paying up above A$0.175 are buying very expensive ounces. Therefore, while there's a lot to like about Auteco Minerals, it's hard to be bullish at the current valuation.

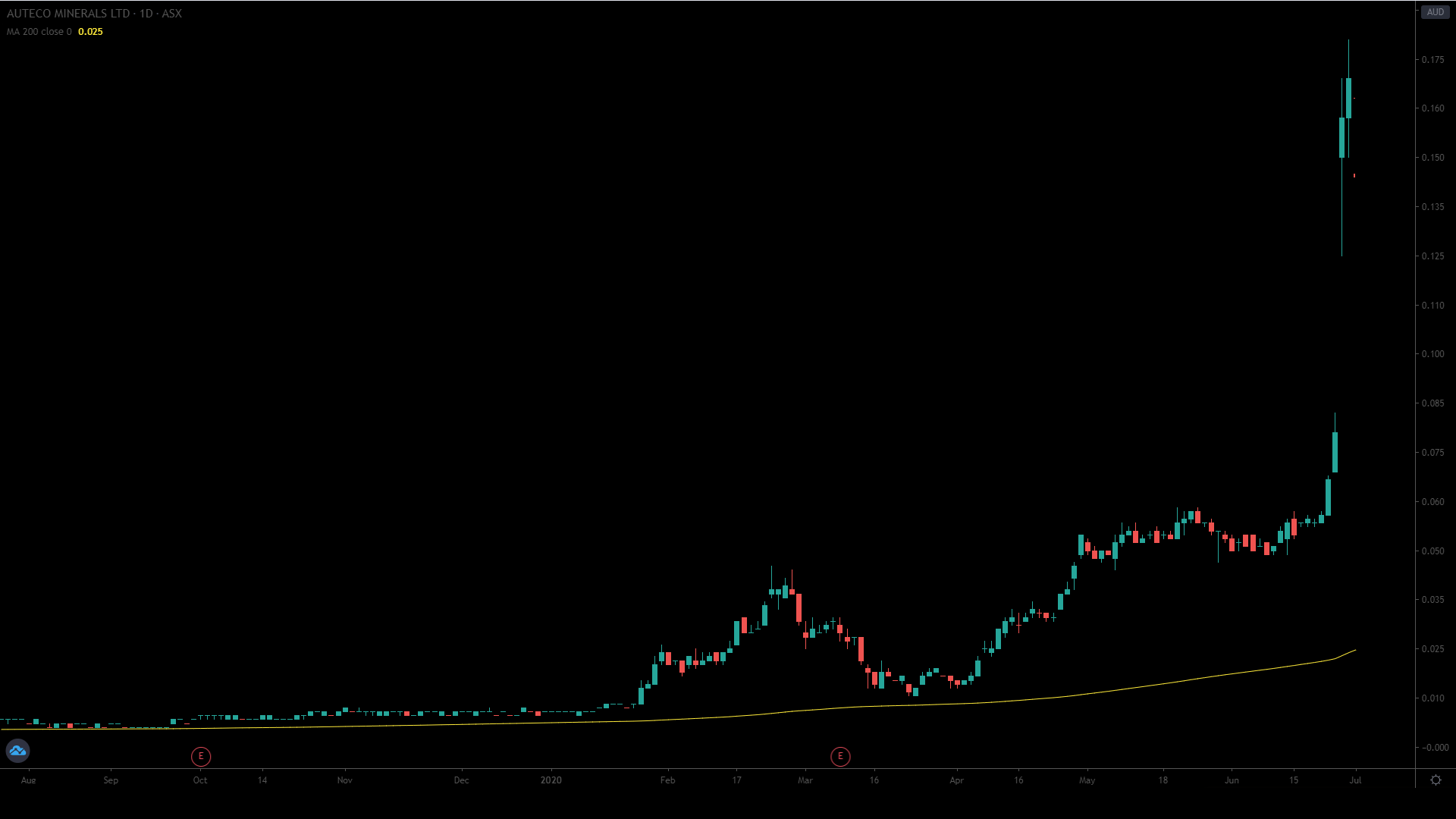

(Source: TradingView.com)

Auteco Minerals is an interesting new story in the junior gold space, but after a 1500% run in less than six months and graduation to a US$150 million market cap, I don't see a ton of upside left here short term. At the current valuation, the company is pricing in a resource of over 1.5 million ounces of gold vs. the current 830,000-ounce resource, and it's going to take quite a bit of drilling and luck to prove up a resource of this size. Therefore, while I think the story is an interesting one to watch for investors, I do not believe it's wise to chase the stock at current prices. If we were to see Auteco Minerals head above A$0.22 before September, I would view this as an opportunity to book some profits.

Auteco Minerals trades significant volume each day on the Australian Stock Exchange but trades very limited volume on the OTC Market. Therefore, the best way to buy the stock is on the Australian Stock Exchange and there is significant risk to buying on the OTC due to wide bid/ask spreads, low liquidity, and no guarantee of future liquidity.

AUT Price at posting:

16.0¢ Sentiment: Buy Disclosure: Held

(Source: Company Presentation)

(Source: Company Presentation)

(Source: Company Presentation)

(Source: Author's Photo)

(Source: Author's Chart)

(Source: TradingView.com)

(20min delay)

(20min delay)