@Jens, you really aren’t helping your case, all you do is throw stones, despite living in the biggest, most homogeneous, uncommitted glass house, globally.

How many Chinese groups have walked from AVZ? How many war crimes are going on in the DRC right this second? Just give it a rest.

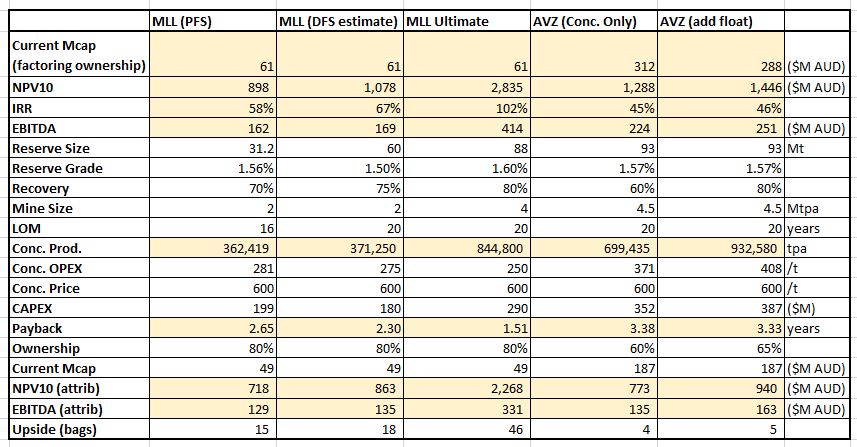

AVZ currently own 60%, so I don’t think it’s incorrect to use that figure, but sure let’s bump it to 65%. The SEZ discussions have fallen over despite the cheer squad saying it was in the bag, so let’s not get too carried away with optimistic assumptions of >75%, with free capital from Elon Musk to build the mine. He may as well build a hyperloop to Shenzen for you while he’s at it (sorry for stealing your pump tweet material for next week).

Your comments inferring that the quality of MLL ore is gravel in comparison to AVZ’s miracle spod that can cure cancer are ridiculous. Goulamina can produce an extremely high quality spodumene concentrate >6% with low iron and low mica well within spec thanks to the deposit being high grade with very low deleterious elements - hence why MLL's operating costs ($281/t) are almost $100 lower than AVZ ($371/t). A study has also proven that Goulamina 6% ore can produce >99.50% lithium carbonate (battery grade).

@Scarpa, if it makes sense economically for AVZ add in a floatation circuit to increase recovery, why didn’t they do it in the DFS?

The enormous start up CAPEX required for DMS alone already kills the project. Adding floatation will increase this further as well as the operating costs which are already much higher than MLL.

I have excluded the sulphate for the purpose of comparing apples to apples, as in my opinion, this is a pipe dream. It requires even more CAPEX, there is no market for this product, and it introduces significant additional risk to the whole project.

The reality is, they have added the sulphate option because the project doesn’t stand up on its own as a spodumene concentrate project, despite how much “biggest in the world, widest in the world, most homogenous in the world” rubbish rhetoric is thrown around by the cheer leaders who drank the Kool aid supplied by MineMark and got hung out to dry by the ex MD Klaus who sold out at 15c.

The 4Mtpa analysis of MLL was to compare (almost) apples to apples – 4Mtpa vs 4.5Mtpa, even with a slightly smaller plant, it blows AVZ out of the water on a fundamental basis, there is no way around that, AVZ is fatally flawed due to it’s isolated location in a jungle, no infrastructure, sovereign risk, 3000km from a port with no realistic way of moving millions of tons of product.

You can investigate 20Mtpa all you like but how much further can costs be reduced? Who is going to buy all of that concentrate? And how much CAPEX will be needed to do it? AVZ already have to split the product over two ports, how are you going to feasibly move all of that product?

See below, if we assume AVZ adds a floatation circuit, which increases recoveries to 80%, and assume that it increases OPEX and CAPEX by 10% which I think is more than fair, the effect is negligible and basically cancels out the increased concentrate produced, even with ownership increased to 65%, which brings me back to my point that AVZ is fatally flawed:

Add to My Watchlist

What is My Watchlist?