Exciting to see AVZ picking up a greater proportion of the project.

Waiting on the sidelines for an entry at 1.5c but I don't see it getting there for another 6 months or so.

Key risks to AVZ:

1. High valuation - I don't think the project at its current stage can justify this market cap.

2. High CAPEX - near impossible to finance over half a billion USD in this environment - I assume a spod concentrate only scenario in my analysis as I think this is realistically how it will be developed in the end if the stars fall into alignment. IMO sulphate is wishful thinking and a hail mary strategy from management as it is apparent that selling spod alone isn't economical for the project due to the combination of high CAPEX & OPEX.

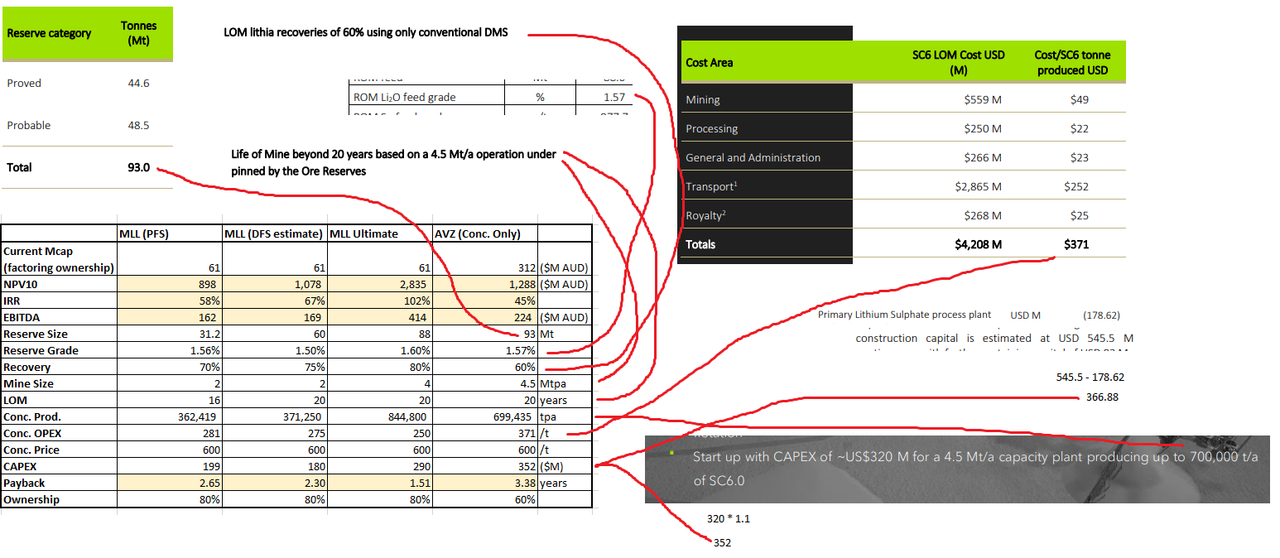

3. High OPEX - $371/t is on the high end and this is already at 4.5Mtpa scale. Doubt it can be reduced much more with further scale. Even if this is scaled to say 10Mtpa - who will purchase all of that spod while the market is currently in oversupply?

See comparison to AVZ's closest African peer below which quite clearly demonstrates the disadvantages to AVZ's project and the lack of upside at current prices:

*This is an old screenshot, need to add an additional $20M to the above for AVZ's CAPEX to acquire the total 75% of the project.

The problems noted above can be condensed down to the following question: why would someone pay $4 for AVZ's lithium when they could buy it for $1 elsewhere? And this ignores the multitude of additional risks that come with this project that have been discussed to death.

As I say, there is value here but not at these prices. I will wait on the sidelines accordingly.

Ann: AVZ to increase equity stake in Manono Project to 75%, page-207

Add to My Watchlist

What is My Watchlist?