Looks like a deliberate soak TBH. If you want to sell you place smaller orders up the buy cue. You don't put 2 x 500k sell order after the S/P has pulled back by 20% into upcoming major news. IMO.

I've been here for a few months actually. Initial positions were around 10.5c back in april just using current pricing to drag my average down into the 9's. Post #:52807718

"Near term production create short term valuation upside.

CR recently completed.

Low capex hurdle rate for production

Upside to NPV/revenue through resource expansion.

Bugger all HC traffic

Low EV

500% ROI in shortish term time frame

Solid top 20.

Then it has a secondary value creation via exploration where results look good.

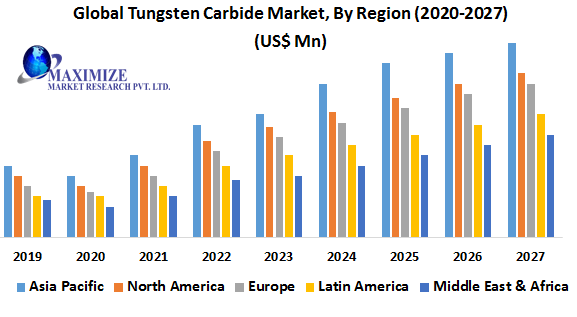

Tungsten is a good sector and Tin also a critical material. Expect these 2 to be at the forefront over the next couple years so expect revenue streams will flex.

NPAT is 40M across 5 years so 8M annually. Not a bank breaker but PE of 10 mean 80M MC potential IMO.

DFS with resource upgrade should extend LOM easily and hopefully further robust economics but still see short term upside and any stock you can get into cash flow positive in the short term is usually sure bet.

Possible 5 times upside on the one the santa comba project. more upside pending exploration on the other."

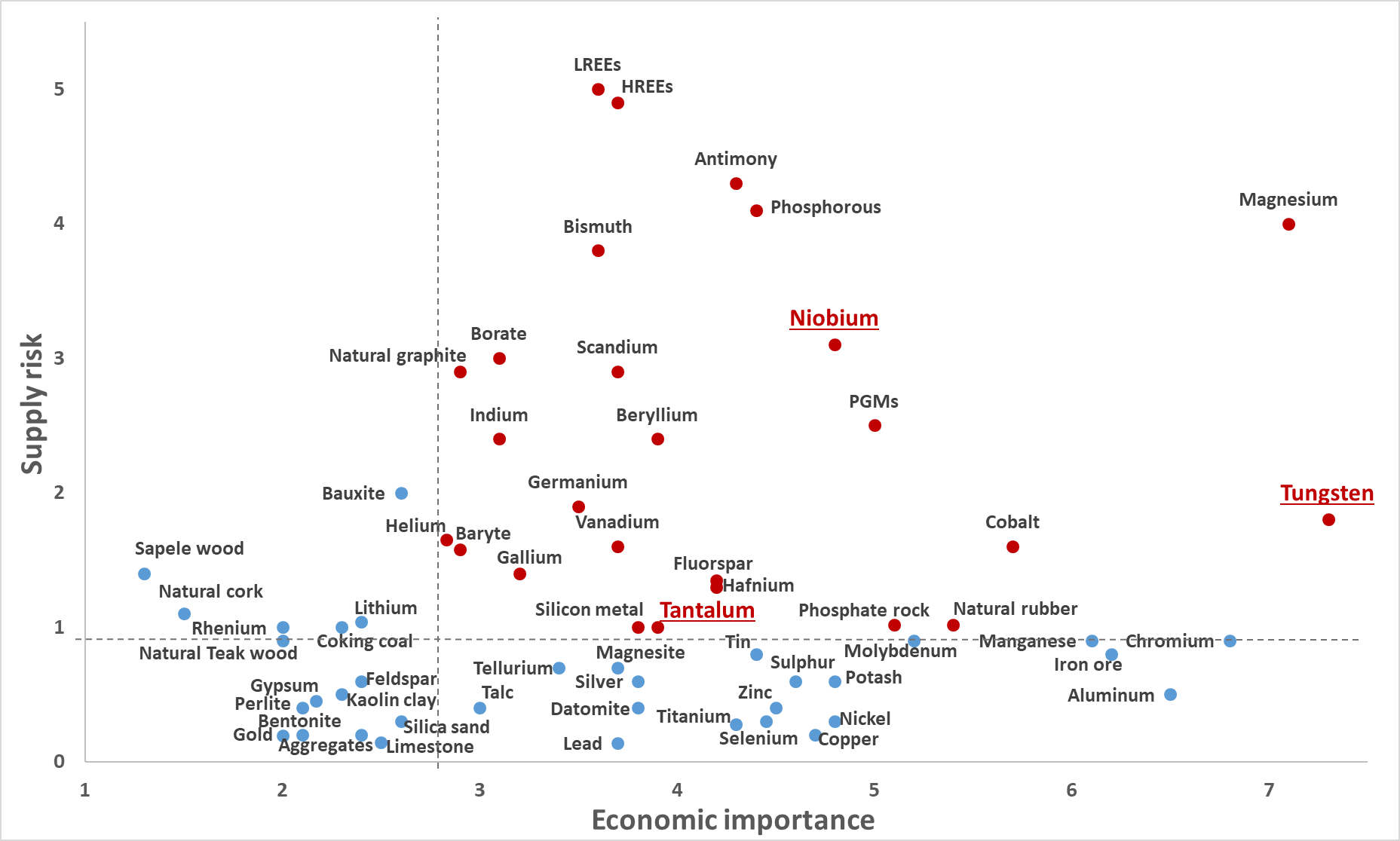

Tungsten isn't quite on everyone radars yet because the price hasn't started taking off, but make no mistake is probably the most at risk commodity currently.

When I looked into the current supply, (which is mostly china based) I found that their deposits are actually depleting. Similar to lithium, rare earth etc, when it's controlled by china there's an interest for the ROW to capture supply outside it. Secondly, when the supply dries up there's usually a massive price squeeze. Tungsten doesn't actually have many substitutes for many applications, so even if the price increases it's not like they can switch to alternative materials at a cost benefit.

85% of world production. It's no wonder people are getting 10M grants to develop the projects.

I'm bullish on the commodity price in the medium/long term, china are snapping up most stuff outside china which is generally what they do to maintain their stranglehold.

Irrespective LOM APT price of 240USD/mtu was used here in the PFS current price is 270USD mtu. With an AISC of 116usd mtu tungsten price need to drop by 60% to be underwater. I give it more chance to go higher than i do to go lower in the medium/long term. Margin is very nice.

We'll see

SF2TH

Add to My Watchlist

What is My Watchlist?