SFR

March 2, 2022 FAT-MIN-807AUD$6.22SpeculativeBSFR Snapshot

1H22; good year

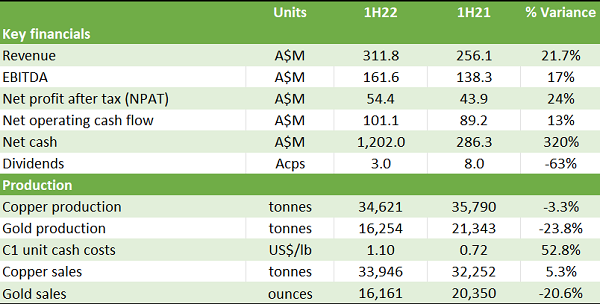

Sandfire Resources has reported its 2022 interim financial result, and in doing so has revealed a good set of headline numbers, as records fell. Net profit surged in the first half, on rising revenue. Mine operating costs were a drag, with freight also a pressure point in the half. Cash flow from operations came in higher, while the balance sheet was in a state of flux, given a major acquisition was pending completion but retains a sound structure post. Shareholders saw the interim dividend fall, despite an excellent financial performance. The following table shows a summary of Sandfire’s key interim metrics (EBITDA – earnings before interest taxation depreciation amortisation, cps – cents per share):

Source: Sandfire Resources

We view the result as a good one, given Sandfire leveraged into a firm copper price environment with higher copper sales. The balance sheet was pending completion of a major acquisition but retained a sound structure, while the interim dividend although lower was not a real disappointment (more on this later in this review.)

Sandfire deliver a surge in its interim NPAT, with the following chart showing interim NPAT:

Source: Sandfire Resources

On a firmer realised copper price and higher copper sales, Sandfire reported an interim NPAT of A$55.2 million, representing a rise of 24.4% year-on-year (yoy). Revenues reported a 21.7% rise yoy, to an interim record US$311.8 million.

Turning to Sandfire’s EBITDA line, and it came in higher by 17% yoy, to A$161.6 million. The following chart shows the factors that impacted on Sandfires’ interim 2022 result:

Source: Sandfire Resources

As Members can see from the above chart, higher realised copper prices and copper sales added US$54.9 million to Sandfires’ EBITDA line. This compares to US$39.6 million attributed to the same metrics for a year earlier. Sandfire does not disclose pricing data, but on a representative copper price, it was trading around US$4.29 a pound as of 30 June 2021 and six-months later was trading around US$4.44 a pound as of 31 December 2021, representing a 3.5% price rise over the course of the interim period. We have a positive view on copper prices going forward and we premise this view on a weaker US dollar on rising debt, ongoing global infrastructure spending and rising inflation.

Copper production was a headwind in the interim period, while copper sale provided a sturdy tailwind. Gold production and sales delivered headwinds in the first half. Members can see from the above table the interim operating performance. Focusing on sales, copper reported sales of 33,946 tonnes, representing a 5.3% yoy increase, with strong demand requiring Sandfire to draw on inventories in the first half. Gold sales totalled 16,161 ounces, representing a 20.6% yoy fall.

Production guidance numbers for 2022 are forecast to be in the range of 64,000 to 68,000 tonnes of copper and 30,000 to 34,000 ounces of gold.

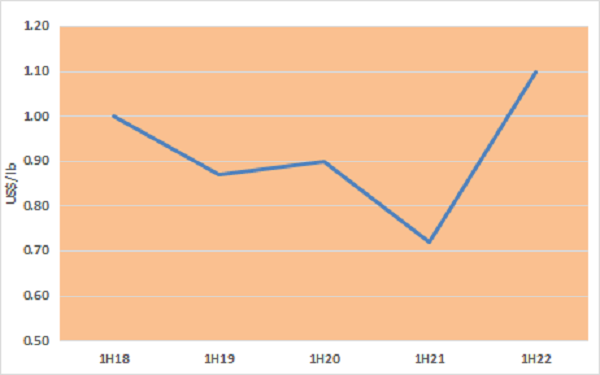

Overall, operating costs were a headwind, contributing US$23.5 million to Sandfires’ EBITDA line. Mine operating costs rose by a modest 3.8% yoy, to US$52.9 million on general inflation driven input costs and lower production numbers. Freight, on soaring fuel costs can be singled out, after reporting a 79% surge yoy, to US$28.3 million. On a unit basis, C1 unit cash costs surged 53% yoy, to US$1.10 per pound. The following chart shows interim C1 unit cash costs:

Source: Sandfire Resources

Costs pressure pressures may persist in the second half of 2022, but 2022 C1 unit cash costs guidance was left unchanged in the range of US$1.10 to US$1.20 per pound. With copper currently trading around US$4.57 per pound, operating margins remain robust.

Sandfire increased its exploration and evaluation spending in the first half of 2022 to US$22.6 million, representing a rise of 4.1% yoy. Black Butte and Motheo reported spends of US$6.1 million and US$5.4 million respectively for the half and US$11.1 million was spent across the rest of Sandfires’ portfolio. Guidance for 2022 exploration and evaluation activities remained unchanged at circa US$55 million. We are pleased that Sandfire continues with brownfield exploration opportunities at Black Butte and Motheo.

Net cash flow from operations for the first half was a healthy US$101.1 million, representing a 13% yoy increase. The primary driver was the 29.2% yoy increase in cash receipts from customers on higher sales revenue, to US$321.9 million. A partial offset was the 13.3% yoy rise in cash paid to suppliers and employees, to US$129.5 million. Pleasingly, commodity prices rose at a greater pace than cost outlays.

A real feature of Sandfires’ 2022 interim results was its balance sheet that as of 31 December 2021 showed a net cash position of US$1.01 billion, on debt of US$145 million. From a year earlier, Sandfire carried no debt and showed cash of US$291.1 million. The balance sheet as of 31 December 2021 was prepped for the settlement of the US$1.86 billion MATSA acquisition that completed post balance date on 1 February 2022. On a proforma basis as of 1 February 2022 the balance sheet including the MATSA transaction showed a net debt of US$473.7 million. Debt at the proforma date stood at US$795.1 million and cash US$321.4 million, including US$50 million of cash brought over from MATSA.Certainly, we have no concerns with the structure of Sandfire’s proforma balance sheet, and in fact we had been looking to it to convert cash into future earnings growth. MATSA is expected to be earnings accretive immediately. We covered off on the MATSA acquisition in FAT-MIN-787 and this report can be viewed here. We consider the MATSA acquisition to be a major game changer for Sandfire.

Sandfire cut its interim dividend to 3.0 cents per share fully franked from the 8.0 cents interim dividend paid a year earlier. We are not disappointed in the cut,instead, we are of the view, Sandfire withholding part of its interim dividend to ensure the smooth integration of MATSA financially as prudent. We expect MATSA will be value accretive well into the future and will easily compensate shareholders for the loss in value in not receiving a higher 2022 interim dividend.

We are of the view, that the decline in the share price, provides an ideal opportunity to acquire a position in Sandfire Resources. We believe Sandfire Resources is well positioned, operationally and financially, to challenge share price highs, especially given our positive view for copper and now also with MATSA under its belt.

Consequently, our recommendation for Sandfire Resources as a buy for Members with no exposure.