Yes correct, it was 51 Capital that first mooted this point:

Here is a subset of the original article that pertains to your question.

Full link below. this excerpt: ----------------------

PARADIGM - SO MUCH MORE THAN A ONE HIT WONDER

Paradigm announced on the 22nd of November that they have In-Licensed a treatment for Mucopolysaccharidoses (MPS). MPS is a group of metabolic disorders caused by the inherited absence or malfunctioning of lysosomal enzymes that are needed to break down large complex sugar molecules like Glycosaminoglycans (GAGs). Basically, people with this disorder don’t produce enough of these enzymes and over time it causes joints to become stiff and painful. This disease has a lot of symptoms that are commonly associated with OA. This is a very rare disease, however, it is estimated around 1:26,000 births would have one of the MPS types. This would mean that across the world, an estimated 300,000 people would have a type of this disease. There is currently no cure for MPS, only symptomatic treatment to try and improve the persons quality of life. Currently the only treatment involves enzyme replacement therapy (ERT) which has been useful in reducing non-neurological symptoms and pain. However, the ERT does not treat the accumulation of GAGs which are stored in the cells and tissues (joints). This accumulation of GAGs lead to inflammation in the joints causing pain and immobility. A recent Phase 2a study (Hennermann et.al.) was undertaken using iPPS (Pentosan) to treat the accumulation of the GAGs and associated pain in patients with MPS - which yielded significant results. The iPPS has already been granted orphan designation status (by both the US FDA and European EMA) in the treatment of MPS and as such has an expedited pathway to market. We anticipate Paradigm will conduct a double-blind, placebo-controlled Phase 2b trial in order to commercialise the drug. As the disease is an orphan indication and very rare, it’s likely the size of this trial would not be excessive. It is unlikely a Phase 3 would be needed to bring this to market due to the severity of the disease. This means that the drug could be commercialised, and sales ramped up very quickly. We weigh any trial in this indication with a high probability of success based on the data released to date from the MPS animal studies, MPS Phase 2 clinical study and from Paradigm’s SAS results in patients with moderate to severe knee Osteoarthritis. The below results are taken from the recent MPS study (Hennermann et.al.) and show the positive effects for treating MPS with iPPS.

PEER COMPARISONS

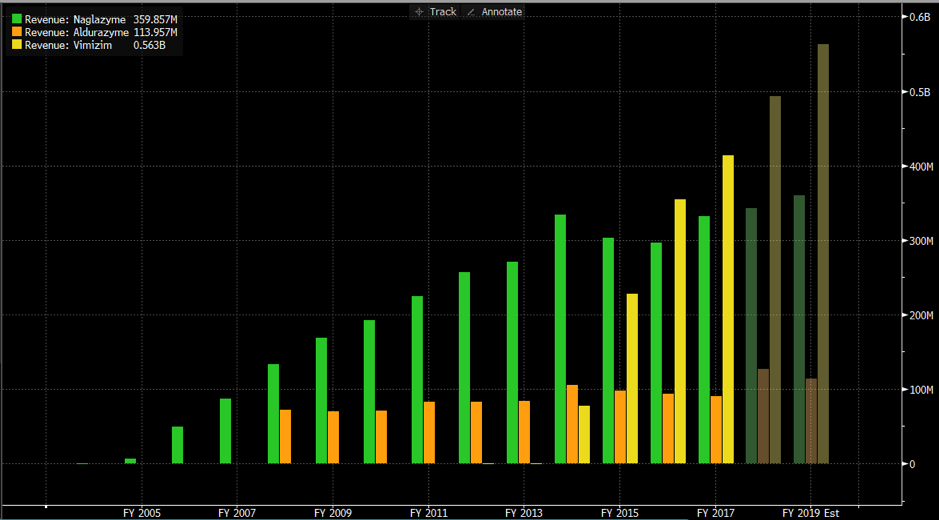

Orphan indications are very small markets, and MPS is a great example of a small market where successful drugs can have a material impact on a patient’s health, while generating significant revenues for the owner of the drugs patent. In our research and discussion with key opinion leaders, we believe Paradigm is likely to have a product that will be able to treat most of the MPS genetic variants. Initially the MPS variants 1, 2, 6 and 7 and second line for MPS 3 and 4. However, given the results seen to date, it could be argued that any lysosomal storage disease that has associated joint mobility, stiffness and pain issues associated with inflammation and GAGs may see benefit from treatment with PPS. Working on the ratio of 1:26,000 births for MPS and only looking at the developed world, we estimate the total addressable market of ~50,000 people. Discussions around pricing at these early stages is always difficult. However, the initial indication from key opinion leaders ranged from $50,000 to $100,000 per year per patient for treatment. The current therapies we explore further on typically cost between $200,000 & $400,000 per year (depending on the patient’s weight). It is worth noting that iPPS won’t replace the current therapy but could be used concurrently with ERT (as demonstrated by Hennermann et.al.) or as a mono-therapy in MPS sub-types where ERT is not approved for use. To outline further the revenue opportunity, it is worth exploring the current Enzyme Replacement Therapy (ERT) used for MPS. These are drugs made by NASDAQ listed BioMarin. BioMarin is valued at ~US$18 Billion and focuses on enzyme technology for rare diseases. The 3 drugs BioMarin have on the market for MPS treat only 3 of the 7 MPS strains. These are:

Aldurazyme (MPS 1)

Naglazyme (MPS 6)

Vimizin (MPS 4)

Below is a graph showing the revenue each one of these product lines generate for BioMarin(Note Aldurazyme is a 50/50 JV with Genzyme (Sanofi) – sales of Aldurazyme were $207m in 2017). Total revenue from these 3 drugs was US$952.5m in 2017. The pricing for each drug varies based on the patient’s weight, however through our research we determine the average cost is around $200,000 per year.

BioMarin revenue earned from MPS ERT drug. We estimate this US$952.5 million in revenue was generated from between 4,000 – 6000 patients. Ascribing value to these drugs, we look at BioMarin’s 3 MPS drugs as a percentage of total revenue and a percentage of their enterprise value (EV). This shows a value of US$10.5b that is attributed to these 3 MPS drugs.

The key difference between BioMarin’s drugs and Paradigm’s will be price. So, depending on the sensitivity we need to discount back this potential value as it will ultimately sell for a lower price. However, it must also be remembered that the addressable market for Paradigm’s drug could be far larger than the three being sold by BioMarin and Genzyme – which probably adds significant value, but for the sake of conservatism we will assume no additional patients to be treated. Assuming this is the addressable market (5,000 people) for Paradigm’s potential new drug, this would generate the following revenue at the below price points:

On our most conservative estimates (treating only current ERT patients and at a price point of only $25k) we estimate Paradigm could generate around US$125m per year. Although we believe pricing is more likely to be around $50,000 per year per patient on average, which would generate $250m on only the existing patients being treated with ERT. Revenue of $750m could be earned assuming treatment of a larger patient population using this same price point. Upon a successful Phase 2b trial and commercialisation of the product, the value could increase materially. Should Paradigm achieve revenue/EV valuations similar to BioMarin the valuation could be somewhere in the range of $2b to $10b based on the above sales range. Although we believe it will be on the lower end of this range given ERT is a higher priority treatment. The real question investors should ask: What is the discovery and potential commercialisation of this drug worth to BioMarin or Sanofi -(Sanofi acquired Genzyme for US $19.6b in 2011). Paradigm’s PPS doesn’t compete with these companies, rather it is used concurrently with ERT, so it would not cannibalise sales. Not everyone is eligible for ERT treatment. ERT hasn’t been shown to reduce the joint pain and dysfunction in MPS so this is complementary to the ERT as demonstrated by Hennermann et.al. As a result, Paradigm’s PPS likely has a far larger addressable market. Another likely benefit to BioMarin is the possibility of a ramp up in sales very quickly given their existing patient population. So, what is this worth to BioMarin? Realistically, we believe the addressable market is far larger than BioMarin’s existing patients, and the drug would be priced more aggressively than our lower estimates.In terms of revenue, this is potentially a recurring revenue opportunity of >US$500m to BioMarin once commercialised.Given Vimizin has an attributed value of an estimated US$5b on sales of similar magnitude, it could be argued BioMarin could pay a significant premium for such a product. We think Paradigm will undertake the necessary steps to reach commercialisation. At that point we think BioMarin or Sanofi would be very interested in doing a deal for this drug. Given the recurring nature of this revenue, orphan status of the drug (giving a monopoly) and demand from these big pharma, this deal could easily exceed US$1b in total deal size. We estimate the deal might look similar to the Aldurazyme deal whereby Paradigm would supply the drug and receive a 50% margin on sales.

-------------------------------------------- FULL LINK:

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.

(20min delay)

(20min delay)