Altura Mining (OTCPK:ALTAF)

This isn't what we expect from a company that has gone bust.

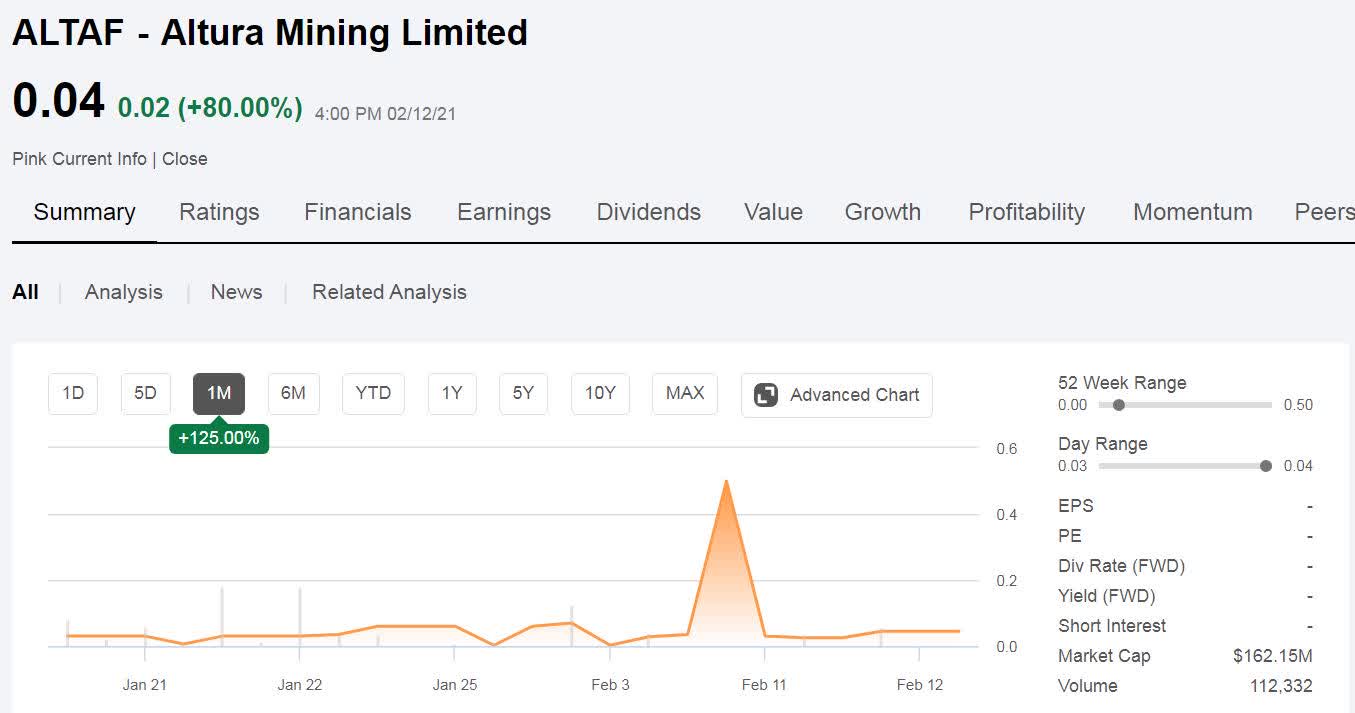

(Altura Mining share price from Seeking Alpha)

(Altura Mining share price from Seeking Alpha)

But Altura has gone bust, properly so, resoundingly so. Those movements in the stock price are from that new sport of speculating upon near anything as with Wirecard and Hertz.

There are no fundamental reasons to have anything at all to do with this stock. It is, of course, possible to bet and speculate but that's all that is being done. Further, if one is betting at random then one is likely to be taken advantage of by more informed players in that speculation. Other than those wishing to bet on the turn of a coin this is not a stock to be playing in.

This is compounded by the fact that it's foreign quoted (Australia) and only just over the $100 million definition of being a microcap. Oh, and, obviously, the fact that it's bust.

There is though an interesting lesson here for us all. Even being in the right sector, a sexy sector like lithium right now, doesn't guarantee success. Those old fundamentals of cashflow and basic value do, always, reassert themselves.

The story

The basic thing we need to know is that Altura is bust. It's also not going to revive without a significant recapitalisation and that would mean a large dilution. The chances of such a recapitalisation are extremely low as there's not actually much left within the corporate shell.

Altura used to run a lithium mine - something we'll get to in a moment - but that has been sold. Lock, stock and barrel, it is gone. The money from that will pay off trade and other creditors and it's most, most, unlikely that there will be anything left for equity holders. The liquidators tell us this much:

21 January 2021 On 26 October 2020 Clifford Stuart Rocke and Jeremy Joseph Nipps of Cor Cordis (the Administrators) were appointed Joint and Several Voluntary Administrators of Altura Mining Limited (ASX:AJM)

OK, and:

At this stage there does not appear to be likelihood of a return to AJM’s shareholders, absent any future recapitalisation and/or restructuring proposal being received that provides for same.

That's, as I say, most, most unlikely to happen. Simply because all that's left there are some partly paid creditors and the listing itself. Yes, a listing has a value but not much of one given how easy it is to get a SPAC going these days.

The mine itself has gone:

The Share Sale Agreement provides for the acquisition of shares in ALO by Pilbara Minerals, which owns Altura's Pilgangoora Lithium Project ('Altura Project'), for US$175 million (or equivalent) total consideration. ALO is a wholly-owned subsidiary of AJM and owns and operates the Altura Project.

That $175 million doesn't pay off all the creditors. There is nothing left within Altura of any great value to produce any return to the equity, therefore.

The useful assumption is therefore that the stock will go to zero. These days that will happen in its own good time and we could have near any pattern of speculation - betting - in the interim. As none of us can know how the madding crowd will run with such speculation it's not possible for us to position ourselves in advance of it. Well, not unless we ourselves were to try and run a pump and dump and given the illegality of doing so we're obviously not going to.

As far as investment goes it's bust, it's gone, it's dead.

However, there is something of interest

No, not an investment of interest but a lesson for us as investors.

Lithium

Lithium's the hot new material, right? We're going to need, as a civilisation, ever increasing amounts of it to feed the EV revolution. Right? Elon's buying it, even has a new process to extract it. American Battery Metals is to recycle it. But as I said about Lithium Americas it's the whole picture that we must look at, not just the sexiness of the sector.

Altura being an excellent example of this principle. They were not just a junior lithium miner; they were actually producing lithium. They had production, sales contracts, they were positioned to ride the wave. So, what happened?

The specific problem at Altura was its financing costs.

(Altura P&L from Altura)

(Altura P&L from Altura)

Output had been ramped up, a gross profit was being made. It was around and about breakeven before financing costs. It wasn't at nameplate capacity yet either. It's those financing costs that killed the corporate structure. They'd taken on too much debt to be able to outrun it at a time of low lithium prices.

But this is a problem for the standard investment view. If lithium is about to soar in demand, is all sexy and all, then how can we be having low prices?

The lithium price is currently depressed. This is just how it happens with minor metals, at least it does often enough. It looks like a shortage is developing, the price rises strongly and much more exploration and production work gets done. Perhaps the estimates of future use were overcooked, or more new work gets done than was perhaps necessary, so a few years later the price dips again. This being what is happening with lithium. (Just to reference Wikipedia: "In 2016, the price was forecast to be $500-600/ton for years to come. However, price spiked above $800 in January 2018, and production increased more than consumption, reducing price to $400 in September 2020." That's for spodumene, a source of lithium., not a lithium itself price)

It might well be true that the EV battery revolution is going to require much more lithium. But that's at some future date, not today. Currently the price is depressed as a result of the thoughts about EVs and shortages several years back. Back when Altura gained financing for example.

It's also true that here with Australian lithium refiners we're talking about a different mineral. This is spodumene (which is, in the Australian deposits, associated with tantalum). Sure, the price is going to be related to that of lithium from other sources. But for the miners it's not directly related. For the miners sell a 6% concentrate from the spodumene to a processor who then upgrades to battery material. Yes, spodumene derived is often preferred, for trace element reasons, to brine derived lithium for battery applications but this extra level of processing does mean that prices don't move entirely in lockstep.

What the capacity of the - largely Chinese - processors is matters to the spodumene price. This is not a particular problem, it's just something to keep in mind. There's a bottleneck between a mine for this mineral and the battery market.

What this does mean though is that the lithium concentrate is sold on long term contracts. For the processor wants to make sure that they have a continual supply, just as the miner wants to know that it has somewhere to send material. From Altura:

We have been able to attract quality customers due to the high quality of our lithium concentrate, with favourable attributes that are sought after by lithium converters and battery producers. The Binding Offtake Agreements contain a floor price of US$550 per tonne (FOB basis) for 6% Li2 O grade spodumene, and a ceiling price of US$950 (FOB basis) per tonne.

Different agreements will have different prices in them, of course, but the general idea will remain. A floor and a cap on the price.

This makes these spodumene miners an interesting little species. They're heavily geared to the lithium price but only over a certain price range. The current spot (in the jargon here, "not long term contract") price is below that agreed range:

Oversupply of lithium salts and subsequent price falls caused the upstream spodumene 6% Li2O min, cif China price to tumble over the past two years from $870-950 per tonne in January 2018 to $370-400 per tonne in the latest monthly assessment on September 30, 2020.

Prices move according to real supply and also demand. That demand is likely to rise is not enough to finance a mine.

Altura took on debt a few years back which was the last time lithium was the sexy beast we all couldn't live without. So did a number of other people and that meant supply rose faster than actual demand - thus the price fell. That killed off the finances of the mine.

Marginal producers

We can also make a point about marginal producers. In any market there will be low cost producers and then a succession of higher cost ones. As demand rises and so do prices then those higher cost producers start to make money or make sense to open for they can gain finance. But if the market then goes into reverse - as minor metals markets so often do given the swift rise in supply - then it will be exactly those higher cost producers who close down again. They are the "marginal" producers that is.

A useful rule of thumb with lithium is that the brine operations are the low cost producers and the Australian spodumene ones are the marginals. Greenbushes, which is the world's largest spodumene mine, went bust with Sons of Gwalia a couple of decades back even though it was regarded then as a tantalum mine rather than a lithium one - or at least valued that way. It's currently running just fine as a lithium mine and I don't mean to say that it has any problems. Only to emphasise that spodumene is the marginal production method for lithium, brines the base one.

That's the teaching moment here

It's entirely possible to have a perfectly fine deposit. To be mining it, to be doing so well and all that. But if you're a higher cost producer then when the price falls then it's you that gets it in the neck. This is true however fashionable the sector you're in.

We can also go one step further. The very idea of fashion for a mineral makes it likely - likely please note, not certain - that more than enough new sources will gain financing. It's those very insistences that future demand is going to rise that encourages a greater than demand rise in supply. This is not a certainty, not at all. But it is something we can note in market after market.

Here with lithium. The last surge in interest led to Altura gaining financing. But other supply rose enough that Altura couldn't outrun its financing costs. Thus, even though nothing in particular was done wrong the company failed.

My view

Altura is bust and there's not going to be a recovery for the equity holders. The stock is therefore going to trend to zero. The path from here to there well, given the adventures that speculators have been willing to have in things like Luckin Coffee and the rest I refuse to try to predict that path.

Over anything but the most random speculative horizon Altura is valueless. Given the exchange and market cap no, don't try to short it.

The investor view

There's nothing there on the bull side and I really would not recommend shorting given the price bounce we can already see above. Being on the wrong side of that one-day leap to 50 cents would have been very painful indeed.

The one value left to us is as a lesson. Base and basic analysis really does still matter. Altura was a perfectly fine company in a sexy market like lithium. It still failed - not because anyone failed directly but simply because making a profit really does still matter.

Further, the very excitement behind these smaller minerals can - often does - mean that new supply outstrips the projected new demand leading to falls in prices. This is what happened. Everyone was entirely right that more lithium was going to be used in batteries. But more lithium got mined than the rise in demand, thus the price fell, not rose. This is more common than you might think in minor metals markets.

Junior miners, minor metals, they're always a high risk game. The biggest risk being that a rise in demand calls forth, as a result of investment fashions, a more than proportionate rise in supply. We might want to apply this lesson to ideas about rare earths and other minor metals given those current investment fashions.