...contrary to some on HC forum who say China is subsidising lithium mines, no China is not subsidising lithium mines.

...China used to focus on policy (subsidising new starts in EVs and lithium) but is now focused on product, which has resulted in EV makers producing cheap EVs with great features.

...those who thrash China's stranglehold over lithium fail to realise:

1) China is able to secure cheap lithium because the big boys like BYD and CATL are vertically integrated and Ganfeng also being the largest lithium producer also produces batteries

2) It controls a well diversified source of lithium from all over the world

3) It can produce lithium cheaper than anywhere else because of a) economies of scale b)proximity to market (large domestic market) c) low energy costs d) cheaper but better trained human resource in the lithium space

Chinese stranglehold over EVs and lithium globally ensures that it plays the Volume game, and will maintain low EV and lithium price for as long as possible for world domination.

Tariffs on Chinese EVs in US and EU will not help Australian lithium miners because China will only buy Australian lithium that it needs over and above what is being produced in China, Africa and South American mines that they control. Lower EV global sales (see earlier post) would mean

lower demand for lithium and would do no favours for lithium spot pricing over time.

For a given fixed SC6 production in LTR as an example, their revenues can't be higher unless market price for lithium improves considerably. That won't happen anytime soon.

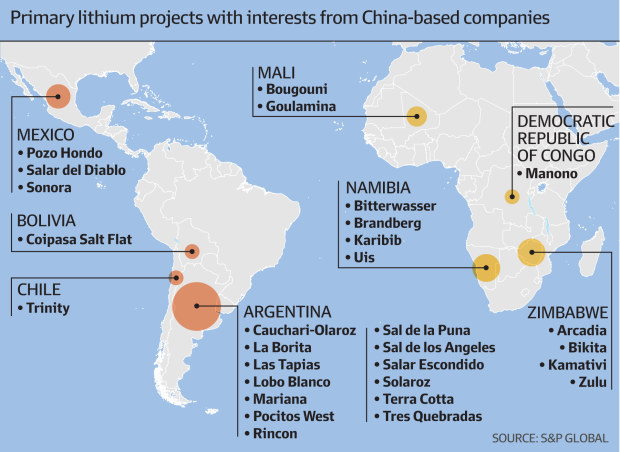

China’s global tentacles

China has more than half of the world’s lithium refining capacity, but relies on imports for about

two-thirds of the raw material, according to a recent study by the Institute of Energy Research.

Most of this comes from Australia, Africa and South American’s lithium triangle comprising Chile, Argentina and Bolivia.

Australia, Chile and Argentina together account for about 80 per cent of raw lithium extraction from salt pans, rock and clay, much of which is sold to China for processing. Chinese companies, in turn, are also directly invested in South American, Australian, Canadian and African lithium deposits.

Chinese-controlled mines around the world will account for 705,000 tonnes of battery-grade processed lithium by 2025, from just 194,00 tonnes in 2022, UBS analysts estimate. This would give it control of 32 per cent of global lithium supply, from 24 per cent last year.

Recent interest from

global lithium giants Albemarle and SQM in Australian miners reflect this fight to secure battery minerals.

Decades of planning and formidable government backing have allowed Chinese companies to first develop and then grow their processing plants. According to the International Energy Agency, China now processes more than half of the world’s lithium.