below is study guide

2023.02.15Historically, all junior resource companies can be evaluated and ranked utilizing four criteria: share structure, people, project and working capital.

None however, is more accurate for evaluation purposes, than “insitu metal value”.

That’s because an early-stage explorer has no tangible value, it isn’t until a junior has established a resource that an informed evaluation can be assigned to what has become an advanced exploration/ development company with a deposit.

One way to determine the value of a junior is comparing the price of the metal(s) in the deposit to the value of the company’s metal in the ground, whether its copper, gold or silver etc. Doing so can sometimes reveal huge discounts.

For example in 2019, Wall Street firms Cantor Fitzgerald and GMP Research spotted Euro Sun Mining, owner of the biggest undeveloped gold mine in Europe. Cantor Fitzgerald placed a short term price target of $2.10 a share, implying an upside of 406%, while GMP’s $3.00 target implied a 641% increase.

Why the huge upside? Because the gold in the ground was cheap. Euro Sun Mining reportedly had over $10 billion of gold equivalent on its books, but the modest market capitalization of $30 million valued each ounce of gold at just $3. The huge delta made for a compelling investment case: why buy gold at the 2019 price of $1,342 an ounce, when you can purchase a tiny gold junior for pennies on the dollar, with $10 billion in gold equivalent (gold + other metals) and the potential for a 6-bagger?

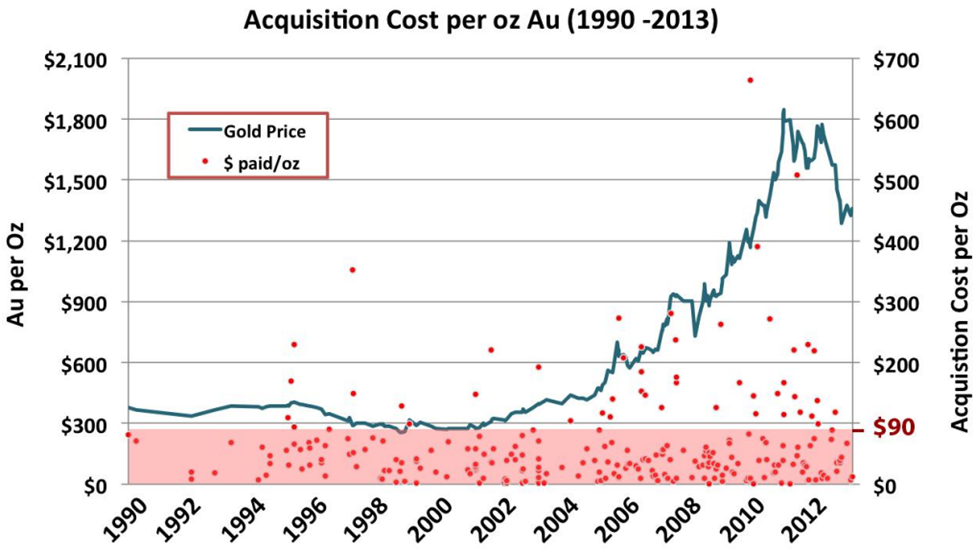

A Cipher Research Report published in 2015 examined a 24-year history of mergers and acquisitions to determine the real value of gold in the ground and to incorporate that value into their project and company valuation models.

Cipher determined that in the most basic terms, the value of a gold mineral project is equal to the number of ounces in the ground that will be potentially extracted times the value or price of an ounce in the ground.

Value = Quantity x Price

Cipher examined 253 transactions involving gold projects or companies owning a gold project, which were acquired in the period 1990-2013.

The conclusions drawn from their statistical analysis include:

- 80% of all transaction occur at $90/oz or less, over half (56%) occurred below $45/oz

- With the exception of a few outliers, there is little or no correlation to the price of gold

- The average price paid for gold in the ground was $63/oz

- The median price was $39/oz

- Slightly higher premiums were paid for projects in development or production versus resource definition stage. Average price is 33% higher ($52 vs $69/oz), Median is 18% higher ($34 vs $40/oz)

- There was surprisingly little difference in prices based on geographical location

- The size of the resource was not positively correlated to the price paid (In other words miners pay for the quality of the project not the quantity of oz)

Add to My Watchlist

What is My Watchlist?