Saxo believes 2024 could mark the ‘Year of the Metals’, with a focus on outperformance in gold, silver, platinum, copper and aluminium.

In precious metals, we believe the prospect for lower real yields and a reduction in the cost of holding a non-interest paying position will support demand, especially through exchange-traded products, where investors have been net sellers for the past seven quarters.

Industrial metals also stand to benefit from supply disruptions, industry restocking as funding costs come down, and continued demand growth in China offsetting global weakness. This will, not least, be driven by the green transformation, which will keep gathering momentum and in some cases replace demand for copper and aluminium from traditional end users, who could suffer from a deteriorating economic outlook.

Gold & silver to benefit from lower real yields, funding costs

Following a surprisingly robust performance in 2023, we see further price gains for gold and silver in 2024.

These gains will derive from the ‘trifecta’ of momentum-chasing hedge funds, central banks continuing to buy bullion at a record pace, and renewed demand from Exchange-Traded Fund (ETF) investors, such as asset managers (who’ve been absent in this space for almost two years amid the rise in real yields and increased carry costs).

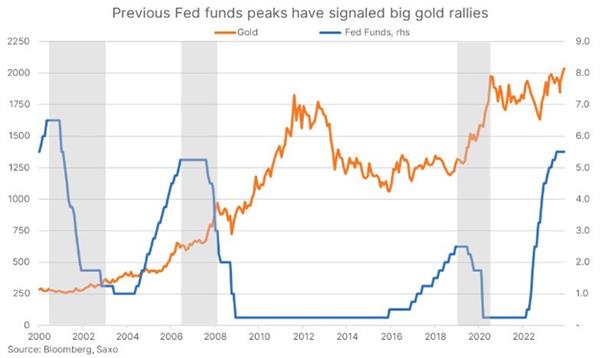

The US Federal Reserve is pivoting towards rate cuts in 2024, and an economic ‘hard landing’ or recession (if it occurs) would necessitate even more rate cuts than the market has priced in. Record central bank buying in the past two years was the main reason gold managed to rally – despite surging real yields – and why silver suffered more during periods of correction. It did not enjoy that constant, underlying demand.

With ETFs, underlying demand is likely to return in 2024. This fact, alongside continued central bank demand (potentially supported by a weaker US Dollar), could see gold reaching a fresh record high at US$2300. Silver may also find additional support this year from the expected rally in copper to challenge its 2021 high of US$30, signalling a fall in the gold-silver ratio below the 10-year average around 78.3.

In platinum, the combination of largely inelastic demand and risks to supply have the potential to exacerbate deficits and tighten market conditions. This would enhance a recovery in ETF holdings from a four-year low and, as with silver, create the prospect of platinum outperformance vis-à-vis gold. It could potentially drive a US$250 reduction in its discount towards the five-year average around US$750 an ounce.

Copper & aluminium supported by supply disruptions, green transformation

The industrial metal sector also stands to benefit this year from the prospect of lower funding costs, driving an overdue period of industry restocking from China to the rest of the world.

Copper – the so-called ‘King of Green Metals’ due to its multiple applications – remains Saxo’s favourite industrial metal for the year ahead, due to robust demand expectations as seen in China over the past year. We‘ve also seen major supply disruptions, led by the government-enforced closure of the First Quantum Minerals (TSX:FM)-operated Cobra Panama mine in Panama. Other mining companies such as Rio Tinto (ASX:RIO), Anglo American (LON:AAL) and Southern Copper (NYSE:SCCO) have also made production downgrades, primarily due to rising challenges in Peru and Chile. Overall, it paints a picture of a mining industry challenged by rising costs, lower ore grades and increased government intervention.

Given the wide spectra of challenges mining companies will face in the coming years, some of which raise the all-in costs of production and reduce their profitability, we prefer direct exposure to the underlying metals, primarily through ETFs.

Disclaimer: Saxo Capital Markets (Australia) Limited (Saxo) provides this information as general information only, without taking into account the circumstances, needs or objectives of any of its clients. Clients should consider the appropriateness of any recommendation or forecast or other information for their individual situation.

The material provided in this article is for information only and should not be treated as investment advice. Viewers are encouraged to conduct their own research and consult with a certified financial advisor before making any investment decisions. For full disclaimer information, please click here.