Real production costs at ASX lithium miners will shock you: Just one mine is profitable

By Carl Capolingua

Tue 03 Sep 24, 12:59pm (AEST) Key Points

Share prices of ASX lithium companies have come under severe selling pressure as many have found themselves operating at a loss at current market prices

Many assumed that as lithium minerals prices plummeted, producers would scale back to rebalance the market – so far this has not occurred

We look at a research note from major broker Citi that proposes all but IGO’s Greenbushes mine are operating at a loss

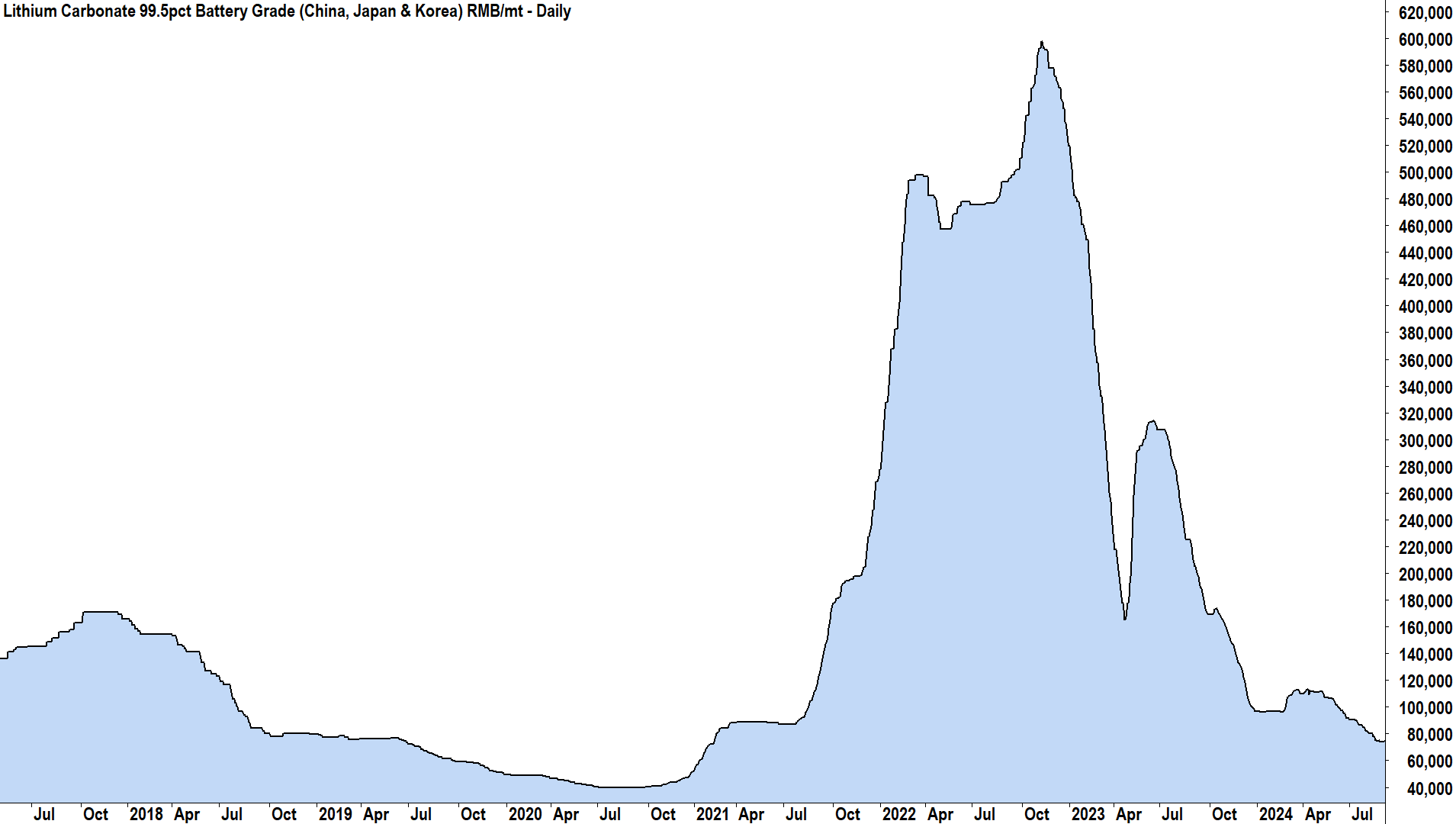

The prices of most lithium minerals are down nearly 90% since 2022, as a glut of supply has hit the market at the same time demand growth from the EV industry has slowed. Many analysts have been trying to calculate the point at which lithium minerals producers respond to prevailing lower prices by reducing their supply, and therefore potentially rebalancing the market and prices. Lithium carbonate price cycle last 7-years: Bust-boom-bust (Click here for full size image)

Despite the price of lithium carbonate falling back to near-pre-bull market levels, so far, the supply response has been limited. In their latest lithium industry research report, major broker Citi has posed some serious questions regarding supplier cost bases and supply intentions.

By Citi’s calculations, every Australian hard rock (spodumene) mine, apart from Western Australia’s massive Greenbushes, is operating at a loss. Further, the broker questions whether supply cuts are being prevented by faulty management team thinking. Let’s investigate the reasons for Citi’s claims, as well as the real cost of producing lithium in Australia – how many miners are losing money at the current price? Exactly where is the “lithium cost curve” anyway?

Citi notes that unlike other commodity mining sectors like gold, there’s “no industry standard for reporting costs” in the lithium sector. Gold miners work out their costs based upon the concept of “All-in Sustaining Cost” (“AISC”. The World Gold Council describes AISC as the “full cost of keeping the mine in business”.

In the lithium industry, producers typically report “cash costs”, and they may also report free on board (“FOB” costs which add in the cost of loading ore onto a transport vessel. The main issue, contends Citi, is that there are subtle variations in what each producer considers valid cash costs, as well as a pervasive lack of reporting of sustaining costs. This means the concept of an all-in-sustaining cost in the lithium industry simply just doesn’t exist. ASX Lithium Miners Production Costs (C1 FOB):

Greenbushes: A$338/t (i.e., approx. US$220/t at AUD/USD 0.65)

Liontown Resources (LTR) (Forecast in Project Update, September 2023)

Kathleen Valley: US$651/t

Mineral Resources (MIN) (FY25 guidance)

Bald Hill, Wodgina: A$800-$890/t (i.e. approx. US$520-$578/t at AUD/USD 0.65)

Mt Marion: A$870-$970/t. (i.e., approx. US$565-$630/t at AUD/USD 0.65)

Pilbara Minerals (PLS) (Q4 FY24)

Pilgangoora: US$390/t

Citi says their methodology for calculating the AISC of Australian lithium takes into account the cash costs regularly reported by local producers, as well as:

Royalties

Port access and freight

Sustaining capital used for regular mining costs like waste stripping, maintaining and replacing equipment and infrastructure

Project or growth capital (e.g. costs of new infrastructure or expansions)

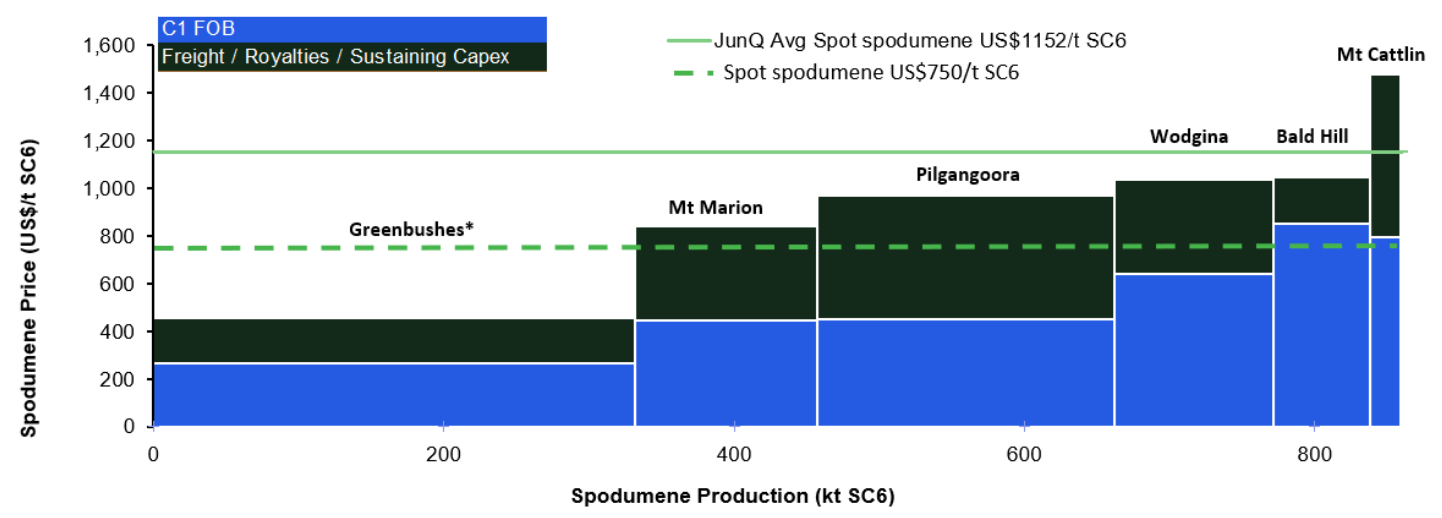

Figure 1. For the JunQ, producers enjoyed positive AISC margins. Spot pricing has since declined US$400/t from the JunQ average to US$740-780/t. Source: Citi Research, Company Reports (From “Australia Specialty Chemicals ASX lithiums: 2Q/ FY25 spodumene cost curve”, Citi Research, 2 September 2024) (Click here for full size image)

The above mine cost schedule adds “Freight / Royalties / Sustaining Capex” to producers’ typically reported cash FOB costs (“C1 FOB”. Citi notes that the above chart accounts for around 35% of global lithium minerals supply.

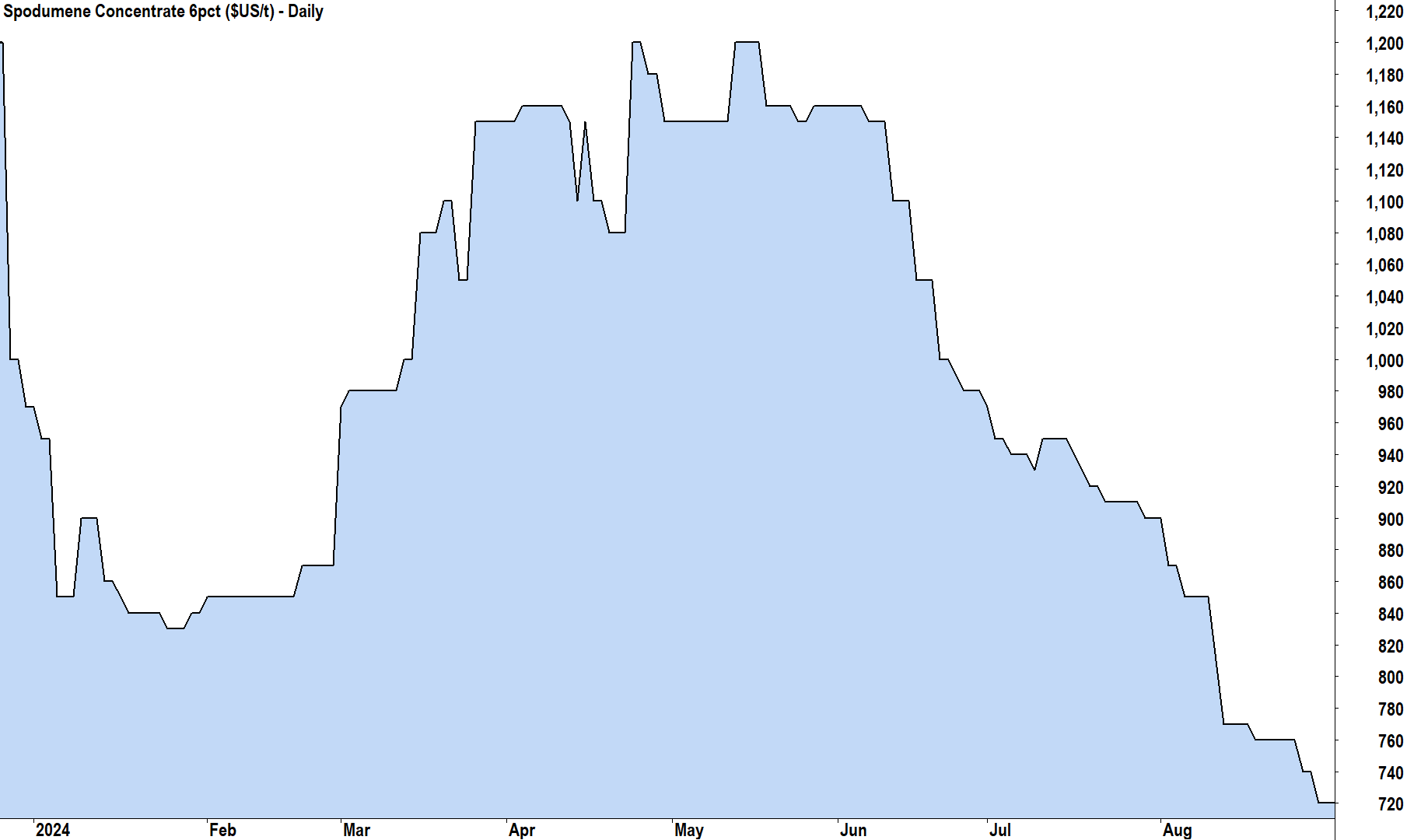

It is clear from the chart that at the dashed line, that is, at the current spot price of spodumene of US$750/t for 6% grade spodumene concentrate (“SC6”, all major Australian lithium mines apart from IGO’s 24.5% owned Greenbushes mine are presently operating at a loss. Note also, that the most recent print for S&P Global Platts Australian SC6 price is US$720/t, some US$30 below Citi’s proposed spot price – and the trend is very much set to the downside. S&P Global Platts Australian SC6 price (Click here for full size image)

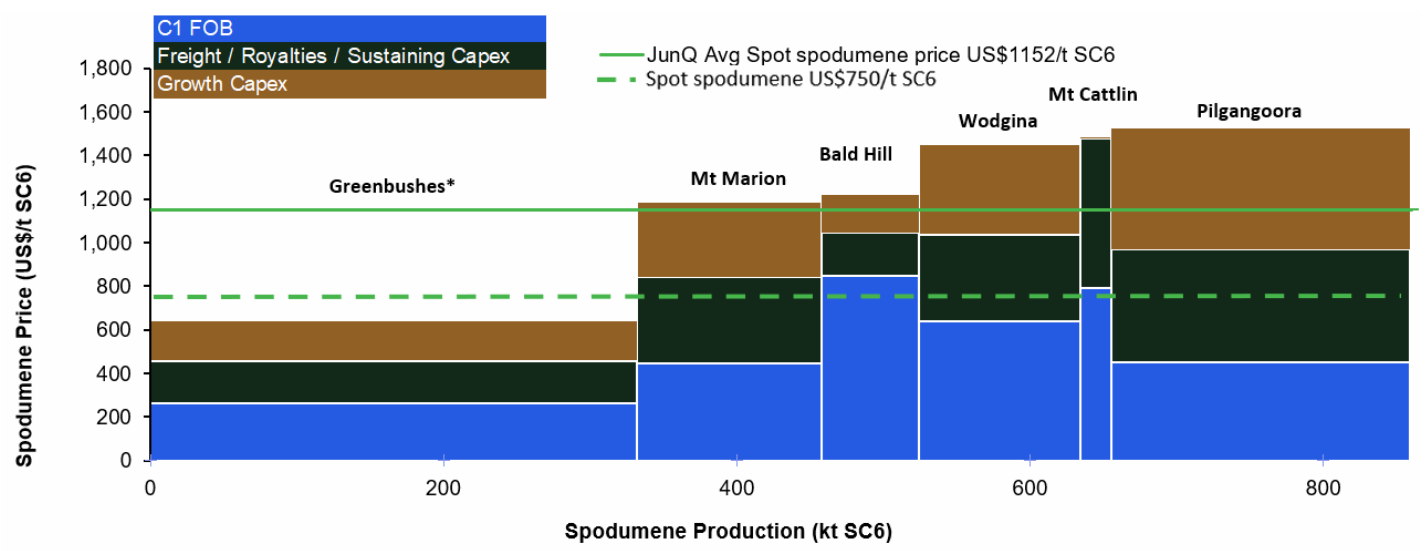

In reality, notes Citi, “break-even costs are higher when costs such as exploration, corporate overheads, financing charges etc are included”. Figure 2, below, adds these in and the picture appears to become even more dire for the profitability of Aussie lithium miners. Figure 2. For the JunQ, on an all-in basis including project capital, Greenbushes was the only mine to make free cash. Source: Citi Research, Company Reports (From “Australia Specialty Chemicals ASX lithiums: 2Q/ FY25 spodumene cost curve”, Citi Research, 2 September 2024) (Click here for full size image)

Figure 2 shows Citi’s best estimate for an AISC for Australian lithium producers. The broker notes that after accounting for growth capex, its coverage is “break-even to loss-making on spot spodumene of US$740-780/t”. This statement suggests that at current spot prices it is make-or-break time for Aussie lithium miners. Are we seeing any sign of a production response?

Looking abroad, Citi notes that other parts of the lithium minerals supply chain are yet to reach their tipping point, noting that several brine operations are still profitable. Citi cites Gangfeng’s Cauchari joint venture in Argentina as one example, as well as other projects Sociedad Quimica y Minr de Chile (SQM) is currently scaling up.

This may be part of the explanation for a lack of supply-side response to lower prices. Some converters have reduced utilisation, Citi notes, referring to companies involved in processing lithium minerals into precursors for the electric battery industry – but high-cost producers like China’s lepidolite industry are yet to implement “material” cuts, the broker notes.

China’s lithium minerals production is down just 10% (around 80 kt annualised) says Citi, suggesting that production and conversion have continued nearly unabated because while the costs of converted minerals such as lithium carbonate and lithium hydroxide have fallen – so too has the price of major input spodumene. This means margins at converters haven’t yet declined to a point that is disincentivising their production.

In the meantime, prices keep falling. Are Australian spodumene producers making a grave mistake?

Citi offers another reason why supply at Australian spodumene producers is yet to meaningfully scale back in response to present sliver-like margins.

“Long-term consensus spodumene pricing is US$1500/t”, the broker notes. By this, the broker is referring to many producers’ very long-term real (i.e. inflation-adjusted) estimates of the spodumene price. Management teams are looking past current pricing, putting it down to typical volatility experienced in any commodity price cycle. They’re effectively ignoring it on the basis that eventually prices will return to their long-run price estimate, and their profitability will recover.

Spot prices are half of managements’ forecasts, notes Citi, questioning whether the lack of supply-side response at Australian producers is simply due to them being “just poorly run”. Citi concedes that for some producers like Pilbara Minerals (Pilgangoora) and Mineral Resources (Wodgina), as their production ramp-ups proceed, economies of scale will likely shift their cost curves to the left.

It’s not all doom and gloom for the Australian lithium sector, though, notes Citi. The broker is tipping that lithium prices will “bottom in Q4”, but ironically this is predicated on supply cuts – “We need to see further supply cuts to re-balance the market”.

. The World Gold Council describes AISC as the “full cost of keeping the mine in business”.