Here is the opinion piece for those interested.The case for shorting Macquarie Group

For over a decade the firm has been the jewel in the crown of Australian finance. But have its shareholders become too complacent about its premium status?

Jonathan ShapiroSenior reporterMay 15, 2025 – 11.40amListen to this article6 minThis week Macquarie has been making headlines for all the wrong reasons.

The corporate regulator came out all guns blazing on Wednesday with allegations the financial services giant had failed to properly report short-selling data for 14 years.

It was the latest in a series of mishaps for Macquarie, which has been basking in the glory of positive press and a solid share price for the past 10 years.

But is the shine of the silver donut finally dimming? Does Macquarie still warrant its reputation as a vestige for brilliant minds to flourish and make themselves and their bosses and shareholders a lot of coin? Is the pride of Australian finance, one of just a few local firms to build a global brand, itself worth shorting?

Macquarie chairman Glenn Stevens, chief executive Shemara Wikramanayake and chief financial officer Alex Harvey front shareholders at its annual general meeting. Peter Rae

We checked the official short-selling data to find out if anyone was betting against Macquarie. If we assume the numbers are correct, there doesn’t seem to be all that much enthusiasm to anticipate a decline in Macquarie’s fortunes.

Shorting Macquarie

At present, about 0.7 per cent of outstanding shares have been loaned out to short sellers, which is about the middle of the three-year range of 0.25 per cent to 1 per cent.

And long-term readers will remember that it’s been almost two decades since someone was brave enough to publicly proclaim a short position against Macquarie.

That was in 2007 when globally renowned short seller Jim Chanos of firm Kynikos pitched a bet against the firm at New York’s Sohn conference.

His claim was that the group overpaid for its assets and used inflated valuation techniques. That prompted a swift formal response from Macquarie, which naturally took exception to his claims.

We do not know if Chanos did profit from his short position, which would have made money during the global financial crisis.

But Macquarie survived thanks in part to a federal government guarantee, and ultimately prospered. Since then, Macquarie has solidified its reputation as an astute and opportunistic organisation with a culture that rewards risk-takers.

While the big four banks retreated into the safety of mortgages, Macquarie had a licence to go anywhere and do anything and become a global asset management and deal-making powerhouse.

But is Macquarie the same institution it was a decade ago? The market doesn’t doubt it, even if the facts don’t fully support it.

Macquarie has had a tough time hitting its numbers. The firm’s earnings have been downgraded eight times in the past two years.

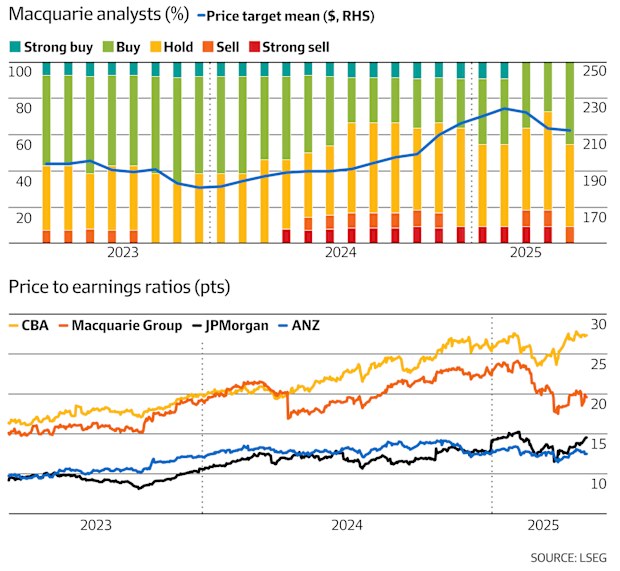

Macquarie has supporters on the street. Of the 11 analysts tracked by LSEG, five have a buy rating and just one has a sell. That compares to Commonwealth Bank which does not have a single buy rating.

And while active fund managers have been shunning Commonwealth Bank due to its excessive valuation, broker surveys suggest they’re happy to pay up to hold Macquarie.

However, the group has done very little of late to justify its lofty premium of 20 times next year’s earnings. And any analyst who doubts Macquarie’s shrewdness might struggle to endorse a buy recommendation at such a high multiple.

For starters, Macquarie has had a tough time hitting its numbers. The firm’s earnings have been downgraded eight times in the past two years, and it needed to pull a few levers – such as selling its helicopter leasing business and cutting compensation – to hit them this time around.

The narrative is that Macquarie is being conservative and that the numbers will improve, but that has not happened yet.

The group’s struggles are evident in a fall in its return on equity which has slid to around 10 per cent, well below the two-decade average of 14 per cent.

When compared to a cost of capital of about 9.5 per cent, it is hard to regard Macquarie as a money-making machine.

By comparison, Commonwealth Bank’s ROE is 14 per cent against a 7 per cent cost of capital, which based on those numbers is far worthier of trading at a premium to the market.

Difficult to value

Macquarie is notoriously difficult to value given its multiple businesses such as asset management, banking, and commodity trading. The latter has been a real money spinner but the volatility of earnings means they’re considered less valuable than more reliable, albeit lower income-generating businesses.

Yet on most measures, Macquarie trades at a substantial premium to its global and domestic banking peers despite its falling profitability.

Finally, Macquarie has a few problems. One is the $1.3 billion of green energy assets stuck on its balance sheet. There seems to be unwavering confidence that the market will recover, and the group can offload its exposures at the right price.

But the jury is out on green assets and in time the pressure will mount to prove the investments were sound.

The other new problem is that Macquarie is in the crosshairs of the Australian Securities and Investments Commission who has called it out for “complacency” and hubris”. That might result in big fines and could result in the prudential regulator taking a dim view of its banking operation, which needs capital to grow.

Analysts broadly remain confident that Macquarie will ultimately get back on track and restore profitability to levels that resemble its past glories.

There are sound reasons to believe it will. Macquarie has told investors it has been conserving capital and liquidity and so will be well-placed to take advantage of opportunities should they arise.

And the management pep talk to staff is that they’re operating in areas where there are huge runways for growth. In private assets they can muscle in on the turf of Blackstone, in Australian retail banking the Commonwealth Bank’s market share is up for grabs, and in deal-making they can dent the dominance of JPMorgan.

But can Macquarie lay claim to have an edge in any of these arenas? Is it still the best investor in infrastructure a decade on from its glory days? The foray into green assets suggests otherwise.

And after making a killing in commodities, their trading talent has been snapped up by aggressive competitors, such as Citadel and Millennium Management, which are playing to win. At best, it’s likely the returns will be lower in that area.

So that’s the short case for Macquarie: a good business valued as though it’s a great one that in time may fall back into the pack if it can’t lift its returns.

But good luck betting against it. Macquarie retains the unwavering faith of Australian investors. Underwhelming earnings, green energy woes and now a stoush with the corporate regulator are not enough to dim its sparkle.

Add to My Watchlist

What is My Watchlist?

(20min delay) (20min delay)

|

|||||

|

Last

$214.15 |

Change

0.310(0.14%) |

Mkt cap ! $81.62B | |||

| Open | High | Low | Value | Volume |

| $214.40 | $215.13 | $212.81 | $166.5M | 773.6K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 1 | 227 | $214.03 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $214.28 | 215 | 1 |

View Market Depth

| Last trade - 16.11pm 25/07/2025 (20 minute delay) ? |

| MQG (ASX) Chart |