There's been a lot of banter around the US targeting the Chinese to lock in BTAs/ the trade war... we are certainly not solely reliant on their future business, although banking on to a certain degree!! European countries have signed BTAs or HOAs already with the US this year because of bargain pricing and future, worldwide options to guarantee reliable supply are thin. Norway, Algeria, Netherlands, UK are at near to full sales capacity and don't have the opportunity to greatly expand output down the track.

Qatar is a threat to US export hopefuls and China can take their "bucket and spade" there once the 23mt North Field expansion comes online in 2024. But, there are constraints on their production output! Rystad Energy estimates that the breakeven price for the Qatari brownfield expansion would be around $5.60 per MMBtu (including transport to Asia), which is around 34% below the breakeven price of the more competitive U.S. projects.

Breakeven prices for the U.S. projects are estimated to be between $7.50 and $9.10 per MMBtu (including transport to Asia). The main reasons for the Qatari project being more competitive are that natural gas production costs are below other regions and its proximity to the Asian markets.

Where else can the world turn to?? Russia obviously due to their pipeline connectivity to Europe and soon to be China but IMO will struggle to get new LNG projects off the ground - sanctions, massive EPC costs and financing! As at 2017, the country was at full sales capacity when taking into account their yearly field production and own consumption.

Australia will definitely not play a role in the next wave. Once Ichthys, 2nd train at Wheatstone and Prelude are all commissioned, a total of 12.mt of spare supply will be available for market... but future proposed export projects are nowhere to be seen. The country has a shortage of gas right now, struggling to support our domestic needs as well as LNG exports... hence the proposals of 3 import terminals which is crazy to think. Australia imported 4.3mt - 6.1mt over the last 3yrs via pipeline from Asia Pacific countries. We are 13th on the list of worldwide countries with proven natural gas reserves, 79% of world reserves belonging to Iran, Russia, Qatar, Turkmenistan, USA, Saudi Arabia, UAE, Venezuela, China & Nigeria... yet our reserves are stranded, predominantly on the NWS.

There are a couple of terminals that have gained attention - Browse, a $30 - $45B project with a partnership consisting of Woodside 30%, Shell 27%, BP 17%. Shell's focus and priorities are on LNG Canada & Lake Charles plus the project has been on the drawing board for years while at one point being scrapped. Peter Coleman has half heartedly targeted an FID by 2021, possibly earlier. Scarborough is a chance. Woodside has slapped an estimated $10 Billion price tag on the 3mt terminal... looking to start producing gas by 2023 then liquefying it from an expansion of the Pluto Plant by 2024.

In 2018, 283mt of LNG was traded. There was no glut. Shell reported that 1100 cargoes was sold on the spot market with a ratio being 1 standard cargo : 74,000 tonnes(approx) = 81.4mt.

I do find it somewhat bemusing when share holders ridicule GV while turning a blind eye to macro environment events that have been out of his control. The company has controlled what they've been able to control without a setback... actually going from strength to strength since 2015 - IDG being the "icing on the cake". There was zero chance of reaching FID in 2016 and 2017' while low odds for 2018'... the long shot possibility was there for late 2018 but my true belief for a long while has been... 2019 - the year we get to construction! Why? The boom bust cyclical nature of the industry. Referring back to my post on 16/1/2018, i gave a detailed account of all worldwide export projects that reached FID since 2002, in mt volumes. It was noted; during the boom times between 2002-2005 & 2011-2015, 106.1mt & 100.7mt of LNG was sanctioned! There were 4 quiet years between 2006 - 2010 where projects that reached FID totalled the following numbers; 4.5mt, 8.8mt, 4.7mt, 17.4mt, 8.6mt (starting in 2006 in ascending order). We are currently in the 3rd year of the next bust cycle, the reality is its a short term, spot trading world at the moment with simply no pressure for buyers to sign long term contracts. Change is on the doorstep though as buyers must look towards the future where a shortage will be inevitable unless action is taken before the end of 2019. From years of research, future demand numbers could look like the following;

85 terminal proposals that have received decent press (52 Asia, 15 Europe/Baltics, 9 Africa, 2 Middle East, 2 Australia) + expansion projects from already online terminals/ proposals 19 (15 from China, 1 Fos Cavaou France, 1 Mugardos Spain, 1 Zeebruge Belgium 1 Swinoujscie Poland).

Total 206.92mt. There are a further 8 Chinese proposals from NOCs - CNOOC, CNPC, Sinopec + 25 proposals from 2nd Tier players namely - Huadian, Hanas, GCL, Yudean, Guangzhou Gas, Sino Gas & Energy, Pacific Oil & Gas, Hubei... that are flying under the radar.

For new entrants looking to enter the LNG market like Bangladesh, Hong Kong, Sri Lanka etc where their terminal utilisation rates will not be known, i gave a worst case utilisation rate of 35% to determine what volumes they might be looking to acquire in the future. Global utilisation rates in 2014 were 48.5% excluding Netherlands, Canada who are tiny LNG importers (otherwise including 44.2%) 2015 42.6% (otherwise 39.6%) 2016 45% (41%).

Although there is no purported glut, approximately 61.6mt of excess supply (from 12 LNG exporting terminals) is currently not contracted and will be available for sale once Australia's Wheatstone, Prelude, Ichthys & USA's Corpus Christi, Freeport, Cameron, Dominion Cove terminals come online and reach full production. Supply that went unsold from trading houses Shell, BP, Engie, Total, Iberdrola, Natural Gas Fenosa = 8.8mt. In the meantime and in both cases, the volumes of excess supply is being sold on the spot market or via pipeline.

Updated, proposed terminals that are front runners to reach FID are:

Fortuna 2.2mt (Has BTA with Gunvor 2.2mt)

Woodfibre 2.1mt

Mauritania 2.5mt (Backed by BP)

Corpus Christi Train 3 4.5mt (FID reached)

Venture Global 10mt (BTAs for 6mt - will majority of this volume be bankable?)

Tellurian 27mt (Initial capacity 11mt, Charif Souki, Meg Gentile)

Delfin 13mt (Initial capacity 9mt)

Mozambique 12mt (BTAs with PTT 2.6mt, EDF 1.2mt)

Sabine Pass Train 6 4.5mt

Sengkang, Indonesia 2mt (BP, under construction)

PNG expansion 8mt (Backed by Exxon, Total)

Golden Pass 15.6mt (backed by Qatar, Exxon)

Qatar Expansion 23mt (North Field)

LNG Canada 26mt (Inital capacity 13mt - Shell 50%, CNPC 20%, Kogas 15%, Mitsubishi 15%

MAGNOLIA 8mt (BTA with Meridian 2mt)

Total 119mt

* This total takes in-to account contracts already signed and initial capacities.

The chasing pack;

Arctic, Russia 16.5mt

Far East, Russia 5.4mt

Baltic, Russia 10mt

Lake Charles 15mt (Shell)

Cameron Trains 4 & 5 10mt

Rio Grande 27mt (Initial capacity 9mt)

Goldboro, Canada 10mt (SPA with Eon for 5mt)

Nigeria Train 7 & 8 8mt (Shell, Total, Agip)

Congo 1.2mt

Total 80.1mt

Overall big picture;

Demand - 206.92mt up until 2025

Supply - 61.6mt not currently contracted from 12 exporting countries.

Supply - 8.8mt not currently contracted with major trading houses

Supply - 119mt from probable, worldwide proposed export terminals

Total 189.4mt

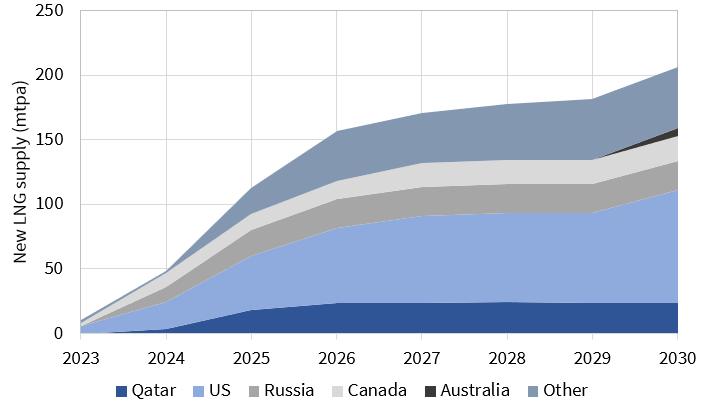

So I'm going to say that in coming up with these numbers, the world is going to need roughly 120 - 130mt of new supply to meet demand by 2025. Remember, 81.4mt of LNG was sold on the spot market in 2017! I just happened to find a graph that backs up my prediction;

Next LNG Supply Wave: the 5 Major Players

June 20, 2018

Will leave you with a parting thought from a twitter statement from respected LNG analyst Susan Sakmar on 30th June 2018. " LNG supply has been growing faster than demand, but the market will tighten by 2023 unless new projects take FID soon. My prediction is FIDs are coming soon! The mood was upbeat @WGC2018 with many projects moving forward. Expect announcements 4Q2018 1Q2019. "

The wave is upon us!

There's been a lot of banter around the US targeting the Chinese...

-

- There are more pages in this discussion • 9 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Add LNG (ASX) to my watchlist

Currently unlisted public company.

The Watchlist

RCE

RECCE PHARMACEUTICALS LTD

James Graham, CEO

James Graham

CEO

Previous Video

Next Video

SPONSORED BY The Market Online