Been loading up every time AMC goes below $14, I see more value in AMC at $14 than buying CBA at $184 with a dividend yield of 2.8% compared with AMC above 5+%, better than money in term deposits and potential for a good capital gain over the next few years.

Amcor is a global packaging leader trading below pre-pandemic levels, offering a strong dividend and attractive risk-reward after acquiring Berry Global.

The Berry Global acquisition brings significant synergy potential, expected to drive 12% EPS accretion by FY26 and 35%+ by FY28, doubling cash flow.

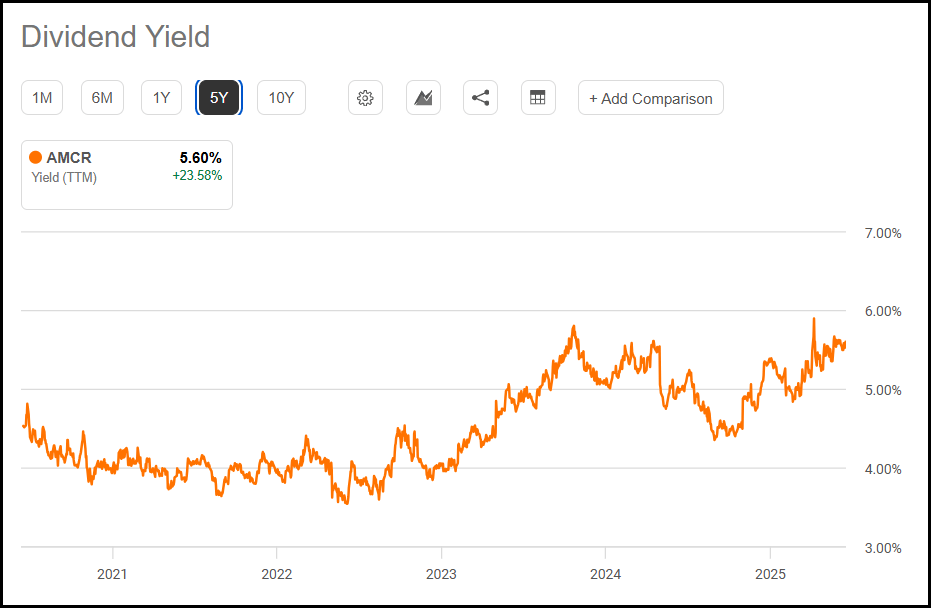

As a Dividend Aristocrat, Amcor's dividend yield is historically high at 5.6%, and the Berry deal should support its sustainability while allowing for future buybacks and balance sheet improvement.

Valuation suggests Amcor is fairly priced for low-rate, low-growth scenarios, but offers compelling upside if merger synergies are realized -potentially making it a Buy now.

Amcor (NYSE:AMCR)(OTCPK:AMCCF) has been struggling with the environment after the pandemic boom, but is now potentially getting a second chance to shine following the Berry Global acquisition. With the stock now trading even below the pre-pandemic levels, a solid dividend and a lot of synergies expected, I rate Amcor a Buy now, with an attractive risk-reward overall. As an essential company in many global FMCG (fast-moving consumer goods) industries paying very strong dividends, this is now getting to the level I've been waiting for to consider buying. Introduction & Financials

Amcor is a leader in consumer and healthcare packaging with a broad global footprint, providing cartons, closures, flexible films and other types of packaging for several global brands such as Coca-Cola (KO), Colgate‑Palmolive (CL), PepsiCo (PEP), Nestlé (OTCPK:NSRGY), Mars, L'Oréal (OTCPK:LRLCF), McDonald’s (MCD) and many others. They provide packaging solutions for a very wide range of industries, from food, beverages and pet food to home care and personal care, being one of the backbones of our modern society and key for many brands around us.

Yahoo Finance

Macrotrends

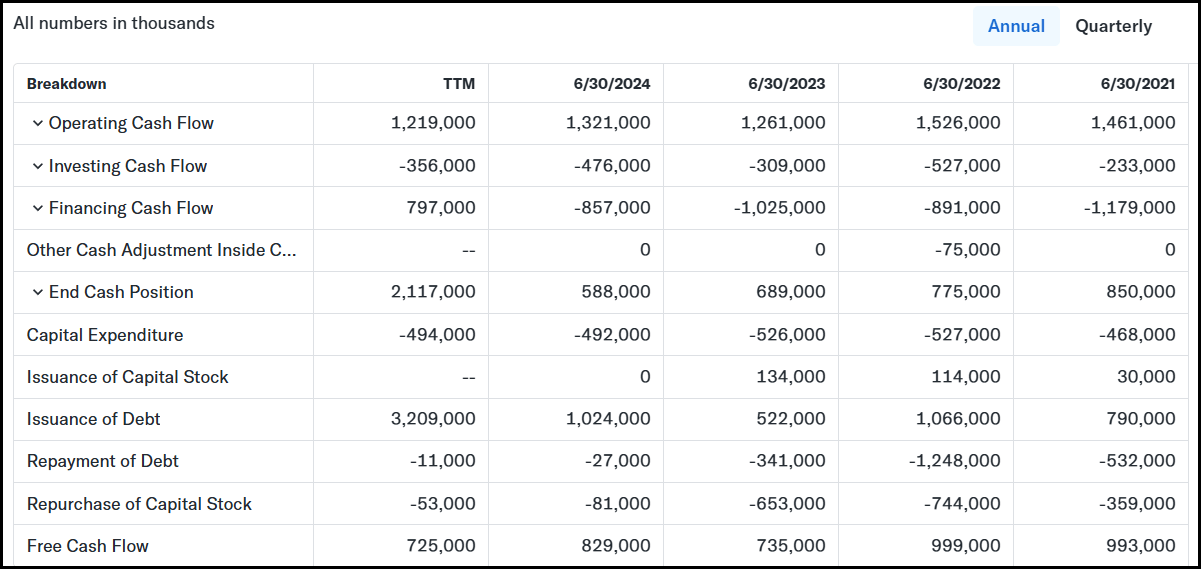

They can make around $800 million in cash flow now and expect $900 million to $1 billion in adjusted free cash flow in this fiscal year, normalizing around a solid level after a significant boom in demand. The company saw a rise in household consumption (and thus demand for packaging) during the pandemic thanks to stay-at-home trends, but that is now falling due to what they call increasingly uncertain consumer environment, particularly in the US, although it’s still significantly above pre-pandemic levels thanks to an acquisition I’ll mention below.

Capital IQ & Capstone Partners

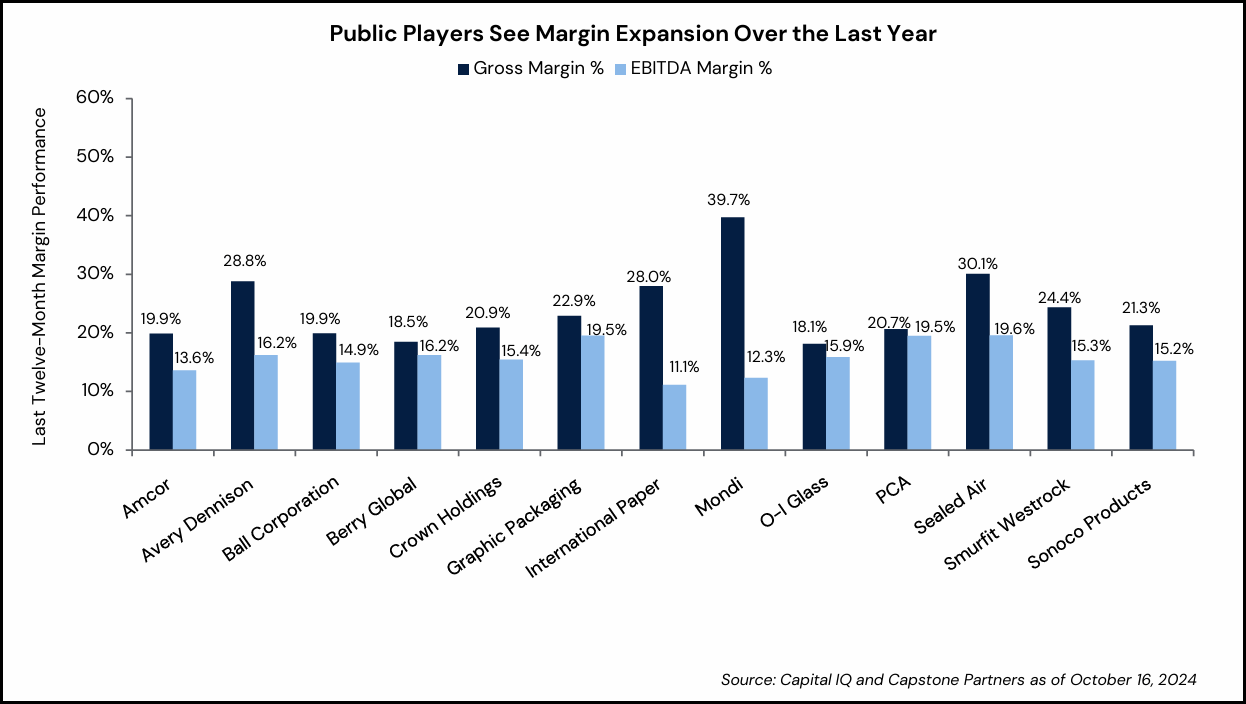

On the margin side, Amcor is below the industry’s average EBITDA margin of ~15.9% last year, according to research from Capstone Partners. Still, given their size as the industry leader, this is not terrible on such a revenue, and we actually see improvements in the past 12 months, although it’s still slightly below their 5Y average of 14.36% due to ongoing issues in the environment.

Amcor IR

Amcor IR

Amcor IR

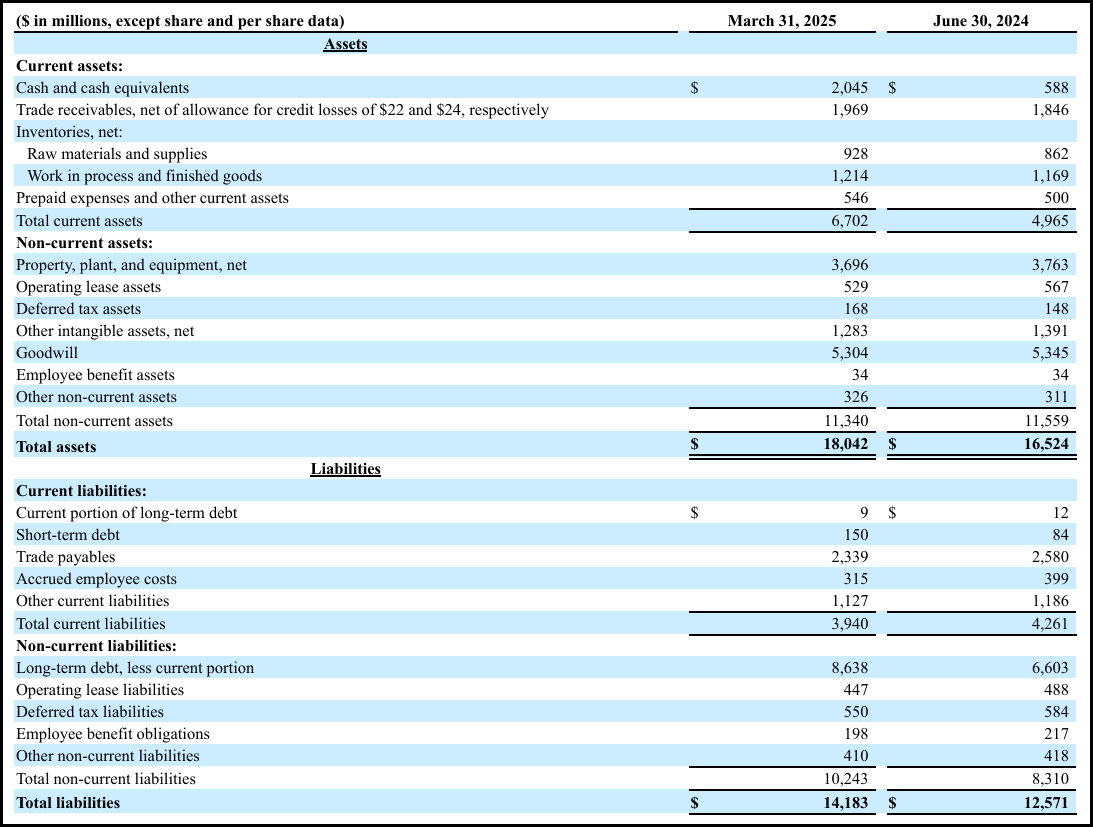

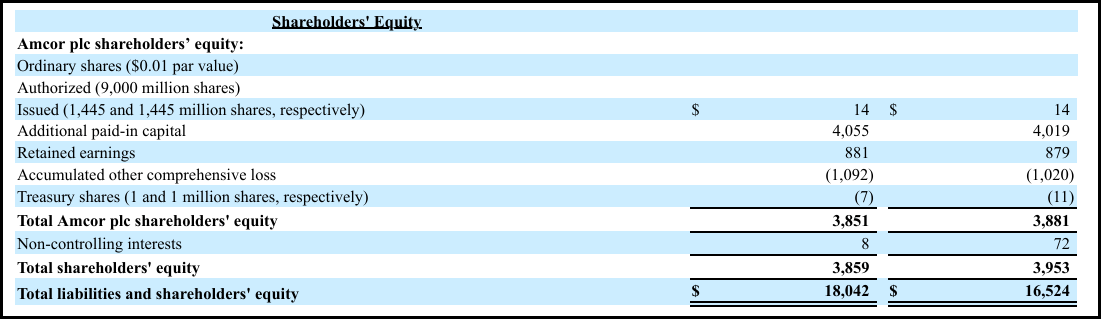

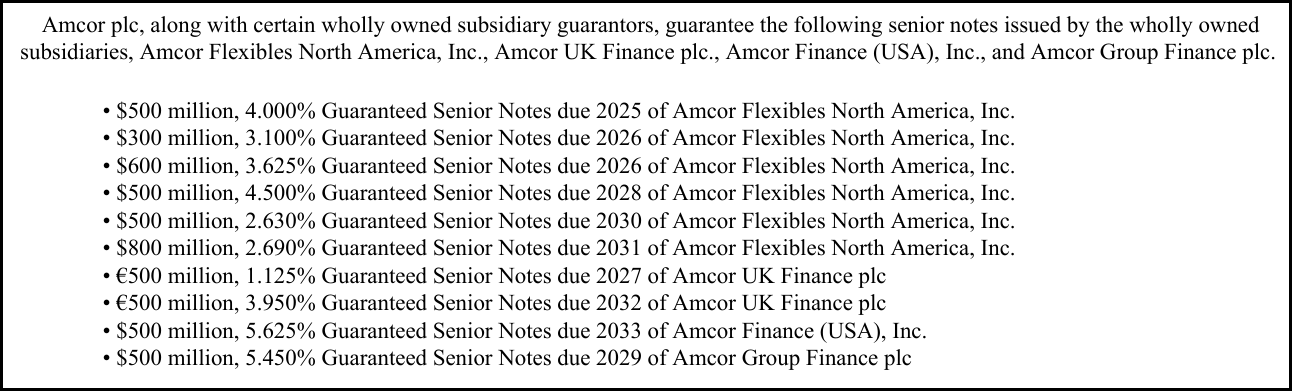

Financially, since Amcor recently bought Berry Global, one of their key competitors, we’ll have to look into both of their balance sheets since they have yet to release a combined one. On Amcor’s side, we see an overall good position, with current assets above their current liabilities, but also a significant amount of debt after recently issuing $2.2 billion to finance the merger with Berry that I’ll mention below. Their debt comes at relatively low interest rates of 1.125 - 5.625%, with all of them being spread well over the next 8 years and no significant maturity in any. So, not a bad balance sheet overall, although there isn’t much equity, especially if we deduct the goodwill.

Berry Global IR

From Berry, we see a similar position, with relatively high debt offset by their assets, although also a significant amount of goodwill. Still, they should be okay from a financial point of view, as no debt came with significant maturities that they couldn’t refinance. If anything, Amcor’s size could help them refinance this at better than Berry’s recent weighted average interest of ~ 5.37%, so that’s maybe another $50-100 million in interest saved. Risks & Opportunities

Amcor IR

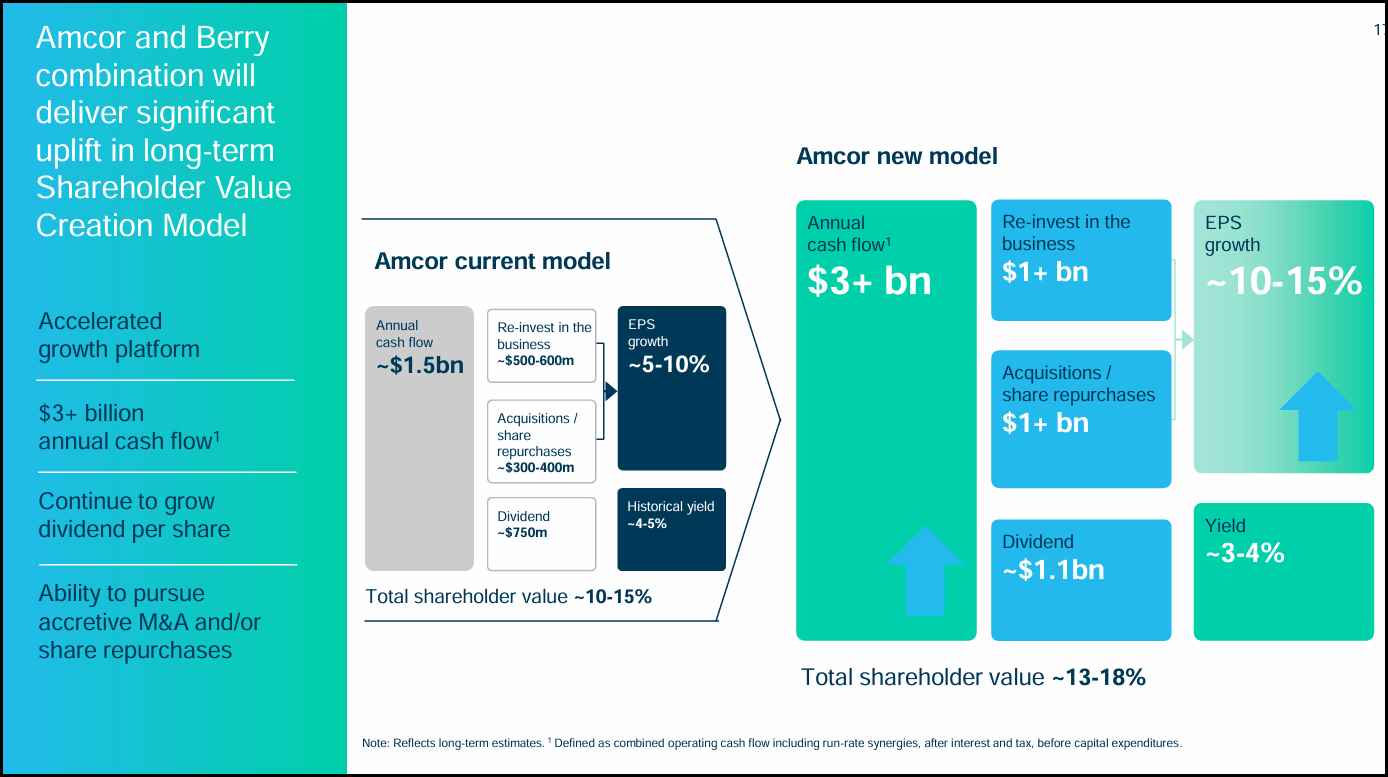

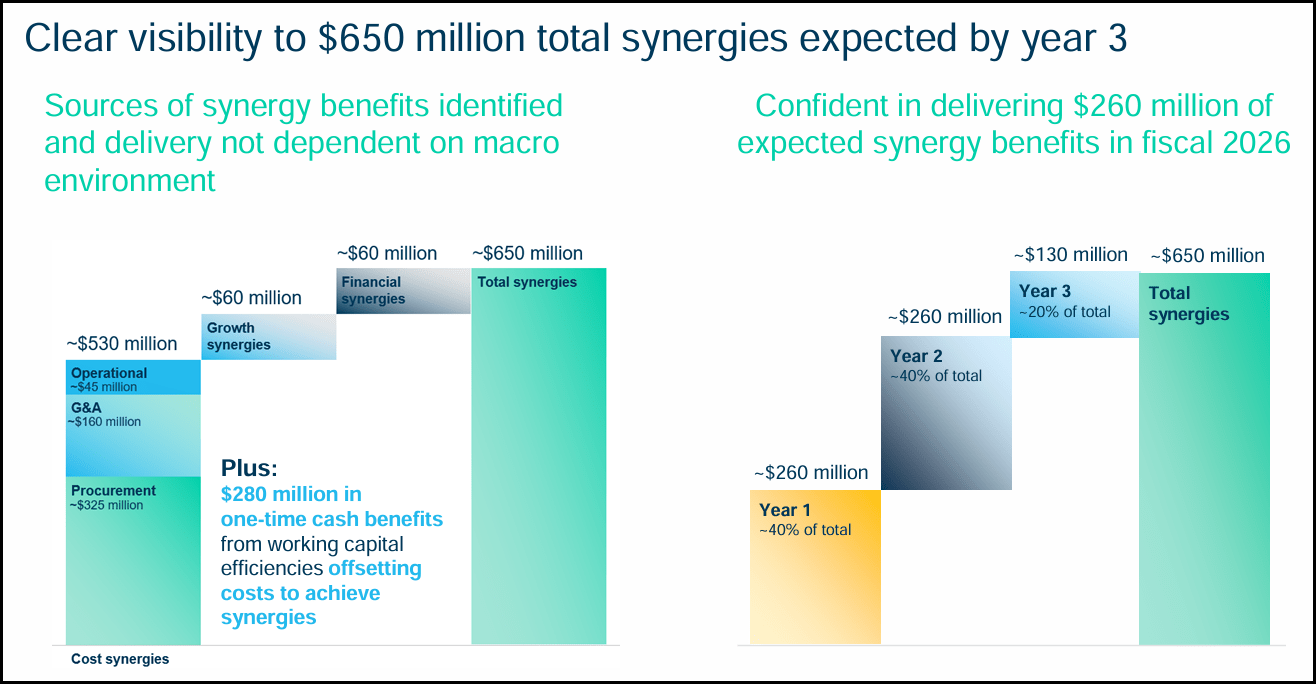

A reason behind the post-pandemic wave of growth, on top of the higher demand, is the acquisition of Bemis in 2019 for around $5.25 billion, combined with structural cost cuts and investments in higher-growth areas. However, we see this repeating itself at an even greater scale now, in what seems to be one of their best moves to date, with Amcor recently announcing another significant acquisition - purchasing Berry Global for ~$8.4 billion worth of stock. Following the acquisition, they expect 12% EPS accretion in FY26 through synergy benefits alone 35%+ EPS accretion by end of FY28 through $650 million total synergies (not annual).

Amcor IR

The acquisition is expected to significantly increase its debt load (as I mentioned above) but should also generate very significant cash flows. With Berry itself generating more than $600-800 million in cash flows in previous years, this should be very beneficial for Amcor. This would basically more than double Amcor’s TTM free cash flow. By FY28, they expect annual operating cash flows of over $3 billion, so a very significant level of growth. It’s no wonder that over 99% of Amcor shares present voted in favor of the deal.

Another potentially positive catalyst are rate cuts boosting the economy, but due to Trump’s tariffs, we now saw the Fed deciding not to cut in June due to expecting elevated inflation and weaker economic growth. Still, 2 rate cuts are expected this year, so it’s a step forward to this catalyst. I consider this a catalyst because rates are one of the tools that central banks have in fighting inflation. By increasing the rates, the Fed increases the cost of borrowing, which limits discretionary budgets, thus lowering spending and demand and fighting inflation. When they are cut, the opposite happens, basically boosting consumer demand and discretionary budgets, which is beneficial for Amcor and their clients.

Another fundamental tailwind to keep in mind is the growing population. Amcor’s products are key for many FMCG globally, and a higher population attracts by default higher consumption of food/beverages/personal care/etc. products, which means sustained demand for companies like Amcor and Berry. Dividends & Buybacks

Seeking Alpha

Amcor is a Dividend Aristocrat with over 40 years of consecutive dividend hikes, currently trading at around their highest yields ever - ~5.6% - representing around $730 million, which is on the brink of not being sustainable. However, thanks to the Berry Global acquisition, this should save the company for several more years. This acquisition literally saved Amcor from potentially cutting the dividend soon and seeing its stock price crash. As a result of the Berry merger, there will be ~2.37 billion shares of the new Amcor based on their SEC filing, so the total dividend should cost them around $1.1 billion from now on, plus other future increases.

They also did significant buybacks back in 2022 and 2023, but reduced them a lot after the environment worsened in recent years. This extra demand also contributed to the ups and downs we saw in the stock price during that time, and there is potential to see them spend the extra capital on that again after the Berry deal, although I’d prefer seeing them focus on repaying the debt and improving the balance sheet first. From the looks of it, they expect the yield to fall to 3-4% from the historic 4-5% as they’ll ramp up the buybacks after the acquisition is complete. Valuation

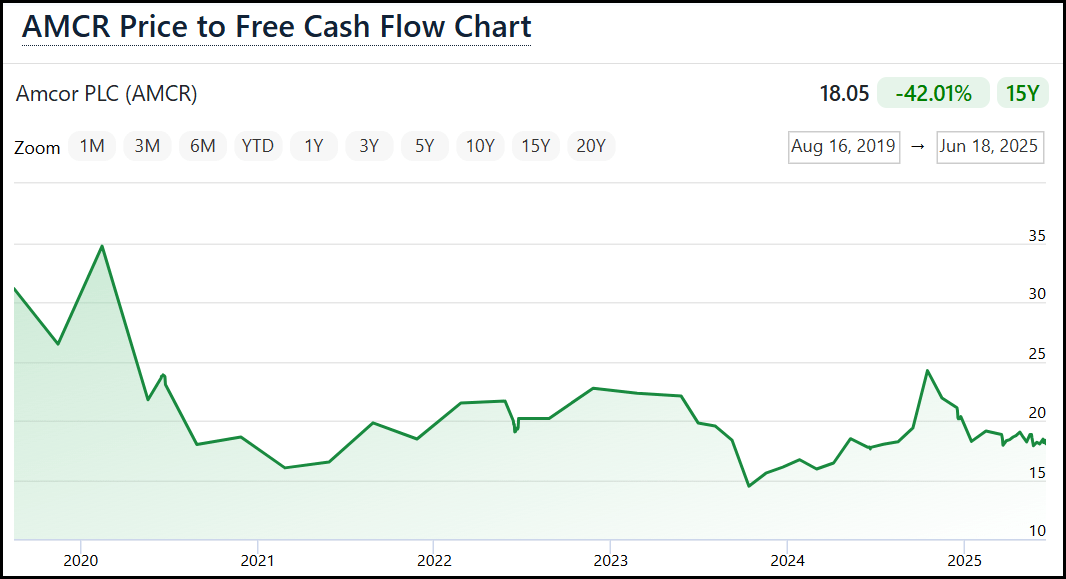

Based on a DCF valuation where Amcor’s cost of capital falls to 6% thanks to rate cuts, and using a starting free cash flow of $1.4 billion (roughly equal to their combined TTM), growing at 5% annually for five years and 3% for the following five (well below Amcor’s 5Y average of 6.3%), with a 1.5% terminal growth rate, we get to an enterprise value of ~$39.0 billion. After subtracting roughly $17.6 billion in net debt following the Berry acquisition, the implied equity value is ~$21.4 billion. With ~2.37 billion shares outstanding now, this results in an intrinsic value of roughly $9.04 per share, which is literally 1 cent below the price this is trading at when writing this. However, let’s also see some sensitivity scenarios to get a better idea about the merger’s potential.

Financecharts

Scenario 1

In a bad environment with basically no synergies and a slow CAGR of 2.5%, the combined companies should make around $1.5 billion in 3 years. If the market is disappointed by this, we can even assume a worse ratio than we’ve seen in recent years - let’s say 12, which would be ~20% below the packaging industry’s median of ~15. That’s a market cap of $18 billion, meaning a price of $7.88, so about 20% below the current stock price.

In this case, their ~$1.1 billion dividend would still be sustainable, and there is enough room to improve the business by repaying debt on top. In this scenario, the yield would be around 6.1%, so that by itself, combined with very small hikes, could be enough to offset the loss. Still, that’s not a good enough return for 3 years, but this scenario assumes significant overstatements about the merger from the company. Scenario 2

If they reach their $3 billion OpCF target, and we subtract roughly $1 billion in CAPEX (their combined levels from recent years), that’s $2 billion in FCF by 2028, implying a solid CAGR of ~10% for 3 years, which is not impossible to see thanks to their synergies and potential debt repayments/lower interest rates. If the market gets more optimistic about it and trades at 22.5x that amount - similar to 2023 levels - that’s a $45 billion market cap, meaning a price of $19.70, so a very nice ~110% profit from the current level, plus significant dividends that they can even hike to 7-8% sustainably. Conclusions

So, based on the current levels, Amcor seems like it’s fairly valued for a low-rate environment and low growth expectations. However, for a solid 5.6% dividend yield and upside potential from the acquisition in case they beat the market’s current expectations, I believe Amcor could be a Buy at the current levels - although I’d prefer to see a focus on debt repayments for a while.

AMC Price at posting:

$14.07 Sentiment: Buy Disclosure: Held

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.

(20min delay)

(20min delay)