Steel mills began to replenish inventory in August, ferroalloy prices fluctuated strongly

2023-08-10 08:34:00 Li Wenjing

Since bottoming out in early July 2023, ferroalloy prices have recovered slightly. As of the close on August 7, 2023, the main contract price of ferrosilicon rose by 0.46% to 6914 yuan/ton, and the main contract price of manganese and silicon rose by 4.29% to 6752 yuan/ton. There are two main reasons for the rise in ferroalloy prices in July: one is that energy commodities have stabilized and stabilized, forming cost support; the other is that steel mills have slightly replenished their warehouses on the demand side. Looking forward to August, the author believes that we still need to pay attention to the influence of these two factors.

From the perspective of supply, the output of ferrosilicon is at a low level and that of manganese and silicon is at a high level, but both are affected by cost support.

The production cost of ferrosilicon is mainly electricity, semi-coke, steel shavings, electrode paste, and pellets. Among them, electricity accounts for the highest proportion of the cost, and semi-coke accounts for about 15% of the cost. In July, the high temperature weather in the south drove up the daily energy consumption, and the power plants began to destock. The available days of coal fell from the high level. According to statistics, Qinghai, Ningxia, and Inner Mongolia Pingdian are still profitable, but the ferrosilicon production losses in Shanxi and Gansu range from 230 yuan/ton to 270 yuan/ton, resulting in low ferrosilicon production. According to statistics, in July, the comprehensive capacity utilization rate of 136 production enterprises in ferrosilicon production areas across the country was 52.34%, an increase of 4.29% from the previous month; the output of ferrosilicon was 434,438 tons, an increase of 8.92% from the previous month, and a decrease of 5.82% from the same period last year. From January to July, the national ferrosilicon output was 3.14 million tons, a year-on-year decrease of 14.3%.

The production costs of manganese silicon are mainly manganese ore, electricity, coke, electrode paste, and silica, among which manganese ore, electricity, and coke account for the highest proportion of the cost. Since the price of manganese ore fell in April, the import profit has remained in a state of loss, which has led to a decline in the enthusiasm for manganese ore imports. According to data from the General Administration of Customs, my country imported 2.51 million tons of manganese ore in June. It is estimated that the import volume of manganese ore in July and August will still be around 2.5 million tons, so there will be a monthly demand gap of 200,000 to 400,000 tons of manganese ore. Although the manganese and silicon production enterprises in the south are losing money, the northern manganese and silicon production enterprises are making profits, resulting in a rise in manganese and silicon production month after month. According to statistics, in July, the comprehensive operating rate of 121 production enterprises (accounting for 94%) in silicomanganese production areas across the country was 62.74%, an increase of 0.71% from the previous month; the output of silicomanganese was 994,350 tons, an increase of 4.16% from the previous month, and a year-on-year increase of 54.2%. From January to July, the national output of manganese and silicon was 6.5 million tons, a year-on-year increase of 11.2%.

From the perspective of demand, the actual demand has not changed much, but steel mills have begun to replenish their warehouses, and the bidding data of steel mills has turned slightly warmer.

The demand for ferrosilicon is mainly for steel smelting, followed by export and metal magnesium. In terms of steel demand, according to data from the National Bureau of Statistics, in June 2023, China's average daily crude steel output was 3.037 million tons, a month-on-month increase of 4.5%; the average daily pig iron output was 2.566 million tons, a month-on-month increase of 3.3%; It was 4.0027 million tons, an increase of 4.7% from the previous month. In June, China's crude steel output was 91.11 million tons, up 0.4% year-on-year; pig iron output was 76.98 million tons, flat year-on-year; steel output was 120.08 million tons, up 5.4% year-on-year. From January to June, China's crude steel output was 535.64 million tons, a year-on-year increase of 1.3%; pig iron output was 451.56 million tons, a year-on-year increase of 2.7%; steel output was 676.55 million tons, a year-on-year increase of 4.4%. Steel production in July is expected to be flat month-on-month and to rise year-on-year, so the demand for steel for ferrosilicon remains stable and slightly increases.

However, the export volume of ferrosilicon has dropped. According to customs data, the export volume of ferrosilicon in June was 31,918.3 tons, a month-on-month decrease of 11,409.8 tons, or 26.33% month-on-month; a year-on-year decrease of 27,930.4 tons, or a year-on-year drop of 46.67%.

Magnesium metal is the second largest demand point for ferrosilicon. In the first half of 2023, the output of magnesium metal will drop sharply year-on-year, and the price will also drop sharply. Research data from relevant institutions shows that China's magnesium ingot output in June 2023 will be 53,000 tons, a month-on-month decrease of 9% and a year-on-year decrease of 35.3%. From January to June, the cumulative output of magnesium ingots in China was 380,000 tons, a year-on-year decrease of 24.6%. It is expected that the domestic output of magnesium ingots in July will continue to decline compared with that in June, about 51,000 tons.

The demand for manganese and silicon is poor, mainly due to the reduction in rebar production and poor overseas prices, but the market is more looking forward to purchasing and storage. Manganese and silicon are widely used in iron and steel metallurgy and foundry industries, and the amount of manganese and silicon used in rebar is significantly greater than that of other steel types. However, under the influence of the downturn in the real estate industry, the demand for rebar is deviated, and the production and sales volume is lower than that of plate, resulting in poor overall production of manganese and silicon. According to the latest data from the National Bureau of Statistics, in June, China's steel bar output was 20.618 million tons, a year-on-year increase of 3%; the output of medium-thick and wide steel strips was 17.711 million tons, a year-on-year increase of 12.9%. From January to June, the cumulative output of steel bars was 117.558 million tons, a year-on-year increase of 0.4%; the cumulative output of medium-thick and wide steel strips was 100.790 million tons, a year-on-year increase of 9%.

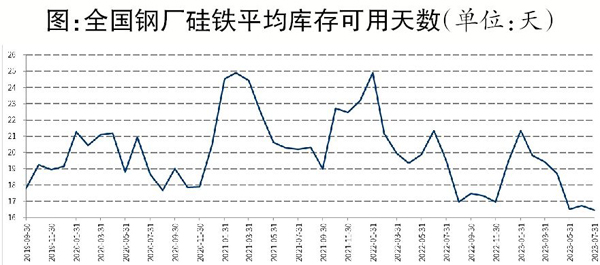

Ferroalloys are raw materials for steel smelting, and steel mills will adopt a low inventory strategy for ferroalloys before the end of July. According to statistics, in July, the ferroalloy inventory of domestic steel mills continued to decrease month-on-month, and the average number of days available for steel mill inventory was 16 days, which was at the lowest point in nearly three years. However, at the end of July, the willingness of steel mills to replenish inventory has picked up. On August 2, the bidding work of the iconic steel mills in the north started, and the bidding volume increased. The willingness of steel mills to replenish raw material inventory has increased.

Looking forward to August, from a fundamental point of view, it is expected that the ferroalloy market will continue to fluctuate at the bottom. However, there are still uncertainties in terms of policies, including the purchase and storage of manganese, whether the production of ferroalloys, crude steel or pig iron will be limited, and downstream demand stimulation policies. For ferrosilicon, the current output is not high, and the market supply is not oversupplied. However, the overseas ferrosilicon price is low and export profits are poor. Exports still drag down the demand for ferrosilicon. The state of "upper top, lower bottom". The biggest variable for manganese and silicon is purchase and storage. According to the current output, the monthly surplus of manganese and silicon is 100,000 to 200,000 tons. If there is no round of purchase and storage, the current high production of manganese and silicon will bring Due to inventory pressure, we still need to pay attention to possible supply bottlenecks at the manganese ore end. It is expected that the price trend of ferroalloys in August will still be dominated by strong shocks.

"China Metallurgical News" (version 3, version 03, August 10, 2023)

OMH Price at posting:

53.5¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)