Put your own puzzle together, based on your own analysis after considering as much information/opinions/data/etc that you can get your hands on, imo.

…but if you somehow think that some investment bank or similar big dog has any interest whatsoever in “helping” retail to “better understand” the market, then you are delusional imo.

Just look at the latest “fearmongering” below wrt forecast oversupply.

Now is that oversupply “forecast” disingenuous or what??

(The below from a post I made over the road the other day)

——

Looking forward to looking back at this over the coming years, btw.

“

Morgan Stanley, who thinks lithium markets will remain in surplus until “beyond 2030”. “

Exhibit 8: Lithium oversupply may take some time to rebalance. Source: Wood Mackenzie, Morgan Stanley Research. (From: “Lithium views from Las Vegas Conference”, Morgan Stanley Research, 1 July 2024)

Exhibit 8: Lithium oversupply may take some time to rebalance. Source: Wood Mackenzie, Morgan Stanley Research. (From: “Lithium views from Las Vegas Conference”, Morgan Stanley Research, 1 July 2024)

“The above Exhibit from Morgan Stanley shows lithium carbonate equivalent (LCE) deficits/surpluses since 2018, and the broker’s forecasts until 2030.”“

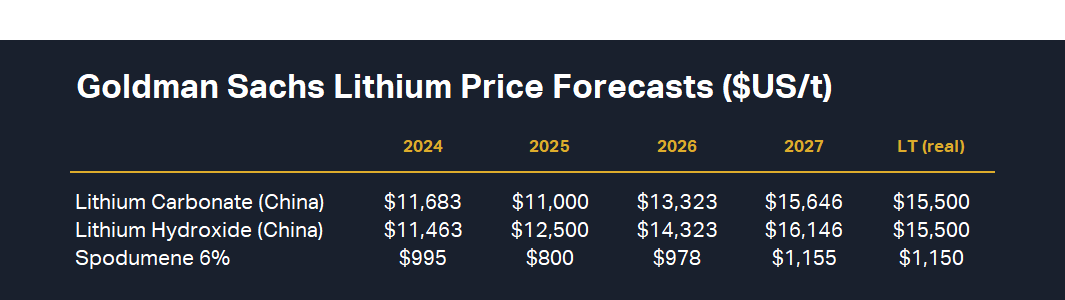

Given its concern about the supply side, Goldman Sachs concludes “we continue to factor in near-term pricing weakness over 2H CY24 and CY25”. See below the broker’s lithium price forecasts out to 2030.”

Table: Goldman Sachs lithium price forecasts. Source: Goldman Sachs Research

Table: Goldman Sachs lithium price forecasts. Source: Goldman Sachs Research“

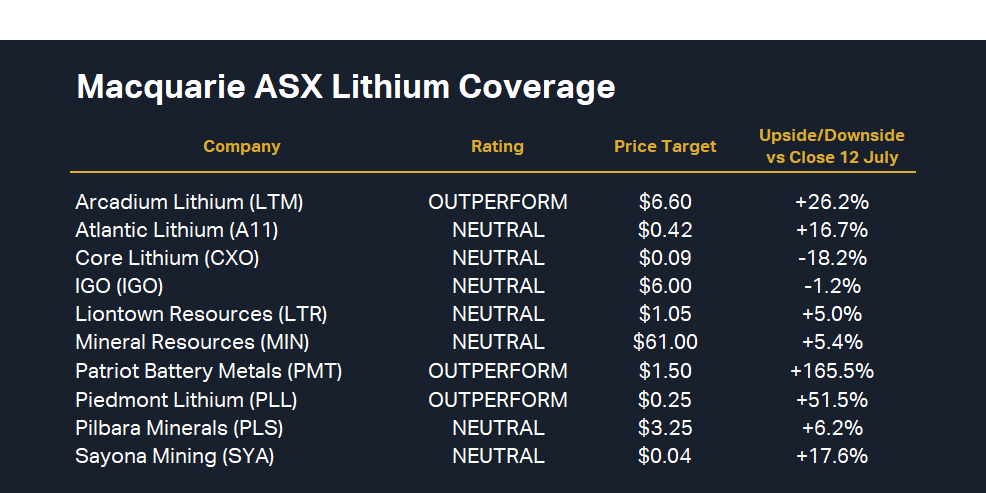

Macquarie predicts elevated upstream supply could continue to “weigh on lithium prices in the near term”.”

Macquarie ASX lithium coverage. Source: Macquarie Research

Macquarie ASX lithium coverage. Source: Macquarie Research——

DYOR on the stocks that these punters actually hold.

With these sorts of outlooks, one would think they’d own ZERO and be short selling up to their eyeballs….

Time will tell.

—-

For those with poor eyesight, you may have missed that in their “exhibit 8”, Morgan Stanley present the oversupply “forecast”….. but it seems that in this “forecast”, they have included supply from what they call:

OperatingPlus

Committed projectsPlus

Non-committed projectsPlus

Projects at 100% basis (theorteically available).Wow. Ponder that.

In 2026, just 2 years from now, it appears they are pointing to an oversupply of almost 600kt LCE.

In that same period, they indicate demand increasing by around 500ktpa, so they appear to be suggesting that supply will

increase by around 1 million tonnes over the next 2 years.

Even if that oversupply is cumulative, their “exhibit 7” indicates an increase in demand of circa 250kt in 2025, and another circa 250kt in 2026, so including their 193kt oversupply in 2024, and considering their 2026 oversupply figure of 556kt, they seem to be suggesting a total

increase in supply (over 2 years) of:

(250kt+250kt)+(556kt-193kt)

= 863kt LCE

Read that again.

Are they actually forecasting an increase in supply, over the next 2 years, of 863kt LCE…???

…but hang on, that includes, it would appear, supply from every possible new project and expansion….? Is that realistic?

Is that anywhere even close to realistic?

Where is their “oversupply” chart that incorporates a more realistic view of the

likely new supply, the “

highly-probable” new supply; one that

excludes projects that are borderline or non-viable under their pricing forecast?

Detail matters.

Very very interesting.

DYOR

——

(20min delay)

(20min delay)