5 – KORE POTASH – Current price 0.775p

Our 2021 recommendations had to include Kore Potash, where almost all the pieces are now in place to allow the company to commence a dramatic growth trajectory. It remains to be seen whether the majors of the potash world will be prepared to concede market share to them or buy them up. Perhaps in the coming twelve months we will get an answer.

Almost every company seems to claim that its operations are in the lowest cost quartile. However, Kore is able to go one stage better as its project has all the makings of being the lowest cost potash supplier to the giant Brazilian market from its globally significant deposits in the Republic of the Congo (RoC). If that wasn’t enough, Kore has the shortest shipping route to the Brazilian market, along with the fast-growing African market.

District scale development potential

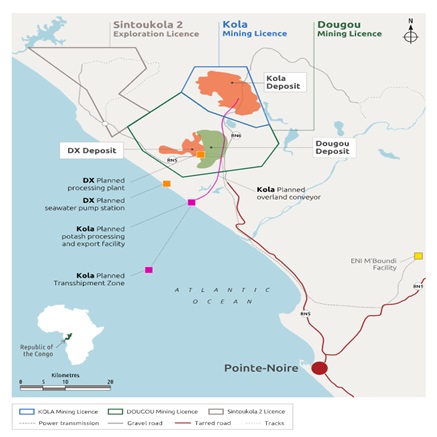

Kore has been developing its vast Sintoukola potash basin in the Republic of the Congo since 2010. The company is certainly well-blessed as it has district scale development with 6 billion tonnes of potash which is just 12km from the coast. There is no shortage of technical data and existing feasibility studies as something like US$150 million has already been spent here to date.

Kore is developing its global significant potash deposits in the RoC. Source: Company

Such is the enormous scale of this potash basin that eventually a big project will be required to really do this globally significant potash resource justice. It will also need a big budget. Its flagship 2.2Mtpa Kola project came through DFS with flying colours but, with an estimated US$2.1 billion capex. Great, but this sort of financing just isn’t available for a lowly capped junior miner for a new project in the RoC.

Small starter DX project

New blood in the boardroom led to a really sensible move to devise the smaller starter DX project, one which would mark the initial stage in the district wide development of the Sintoukola potash basin. The 400,000tpa DX project is rapidly going through feasibility studies and there is no reason that this shouldn’t be in production by Q4 2023. The PFS was announced in May 2020 and allowed the team to commence work on the DFS in September 2020.

Progress on various elements for the DFS allowed an Updated PFS to be announced in mid-November 2020, materially enhancing the results of the PFS. Basically, the Ore Reserve estimate for the DX remained unchanged. However, an improved understanding allowed the production schedule for this Updated PFS to include 2.43Mt of Muriate of Potash (MoP) from Indicated Mineral Resources and 2.31Mt MoP from Inferred Mineral Resources. The end result is a far longer mine life and higher NPV.

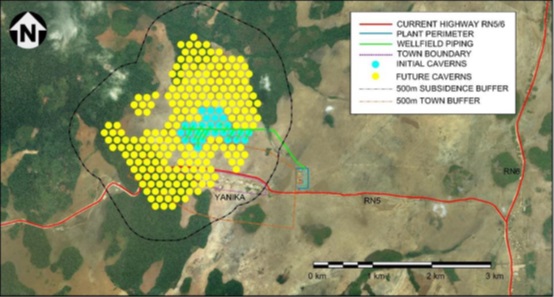

Wellfield and process plant location planned for DX. Source: Company

As it stands, the Updated Production Target gives a 30-year project life at 400,000 ktpa MOP. The Updated PFS determined an attributed NPV 10 of US$412 million and 23.4% IRR on a real post tax basis at life of project average granular MoP price of US$422/t (which is the Argus Media’s price forecast CFR for DX Project’s target markets), with a post-tax payback period of just over four years.

All the signs are that DX can rapidly come on stream with capex under US$300 million, making it financially possible for a greenfield operation in the Republic of the Congo. DX is a scalable solution mine which is low risk as there are many such successful potash projects around the world. Getting DX into production is a game changer as it will make the financing of Kola possible and begin to unlock the tremendous value here.

All this is being played out against a background of rising potash demand as the world will need to grow 50% more food by 2050. Arable land per person is sharply declining and farmers are increasingly using more fertiliser to feed an anticipated population of 9 billion people by this time. Kore will produce MOP which is the cheapest and most important source of potassium for agriculture, so there is no risk of substitution.

Our view is that Kore will either be allowed to grow or be acquired. DX and Kola put Kore on a real journey with its 6 billion tonnes of potash. Not only are the company’s production costs very cheap but also Kore has the shortest shipping route to the African markets and Brazil. Moving ahead, the development of the Sintoukola Potash District will basically be serving to replace potash from the Northern Hemisphere.

There looks to be substantial potential value to be created at Kore for the benefit of all shareholders over the coming years. We initiated coverage on Kore Potash with a Conviction Buy stance in June 2020 when the price was sitting at 0.85p with a target price of 6.51p. Now with the shares trading at 0.80p, we are more than content to reiterate our stance.

Add to My Watchlist

What is My Watchlist?