I apologise I wasn't aware the link was collecting emails or that you could post whole blog posts here:Elders: A High Quality Agricultural Cyclical Underearning and Undervalued

Key Purchase Reason:

Not only can Elders now be bought with profits at a cyclical low, but can also be bought with a low valuation based on those lower profits.

Thanks for reading Christopher’s Investment Journal! Subscribe for free to receive new posts and support my work.

Elders sells goods and services to farmers across Australia such as agricultural chemicals, seeds, livestock broking and insurance. Its profits are also cyclical, not quite as cyclical as an individual farm, but Returns On Capital (ROC) tend to rise and fall from year to year based on a variety of factors. Based on last year's results, Elders profits are down due to a variety of temporary cyclical factors and its ROC is among the lowest in the last decade. In addition due to falls in the share price, its valuation based on those cyclically low profits is also quite low relative to past years.

What Elders Does

Elder’s is an Australian agribusiness that provides goods and services to farmers and other agricultural businesses. It divides itself into four key segments:

Branch Network: Is Australia’s second largest supplier of farm inputs such as seeds, fertilisers and agricultural chemicals. As of November 2023 it operates a network of 242 retail stores, provides product advice from 256 agronomists and has a wholesale business that provides independently owned stores.

Livestock Agency: provides a range of marketing and advisory services for livestock, wool and grain.

Real Estate Services: Is involved in the marketing and property management of farms, stations and lifestyle estates through company owned and franchised offices. Other services include water broking and commercial real estate.

Financial Services: Elders distributes a range of financial products including banking, finance, insurance and warranties.

Feed and Processing Services: Elders operates Killara feedlot, which incorporates grain-fed beef distribution, grass fattening operations, cow manure processing and irrigated corn production in Quirindi, New South Wales Australia.

In the 2023 financial year gross profit was $619 million which can be broken down into each of the above segments as follows:

Moat

Elder’s first significant competitive advantage is its brand in rural Australia. The Elder’s business has been around in Australian rural communities for 185 years and according to the Roy Morgan trust score it continues to be the most trusted brand in regional Australia.

The next competitive advantage Elders has is its scale. Elder’s businesses spread across much of rural Australia providing lots of goods and services to Australia’s farmers. This allows it to invest significant sums in optimising its supply chain efficiently moving goods from its many suppliers to its many stores and customers. In addition to its efficient supply chain it is also able to purchase goods for its stores at scale discounts and even produce its own branded goods through its backwardation strategy. All this allows it to get lower prices for its customers and take more of the margin on each good and service sold. Furthermore in its agency business scale advantages are also very important as businesses based on auctions generally move to the largest auctioneers. As it allows the sellers to get their livestock and crops in front of more customers and the customers to see more livestock and crops.

Finally another important advantage Elder’s has relative to its competitors are its relationships with its customers. Elders are invested in their customer’s success with each branch having managers who build relationships in local communities and with Elder’s many agronomists advising farmers on how to get the most out of their land and deal with the many challenges their businesses face. For example in the Northern Territory the year round hot conditions can lead to heat stressed cows developing leaky gut, where the majority of their immune system resides. This can lead to a decline in the health of the animals and productivity of the herd. Elder’s staff after researching supplementation systems developed an innovative new lick block containing chromium called KEMTRACE, that can help remove the impact of the heat stress.

Earnings and General History

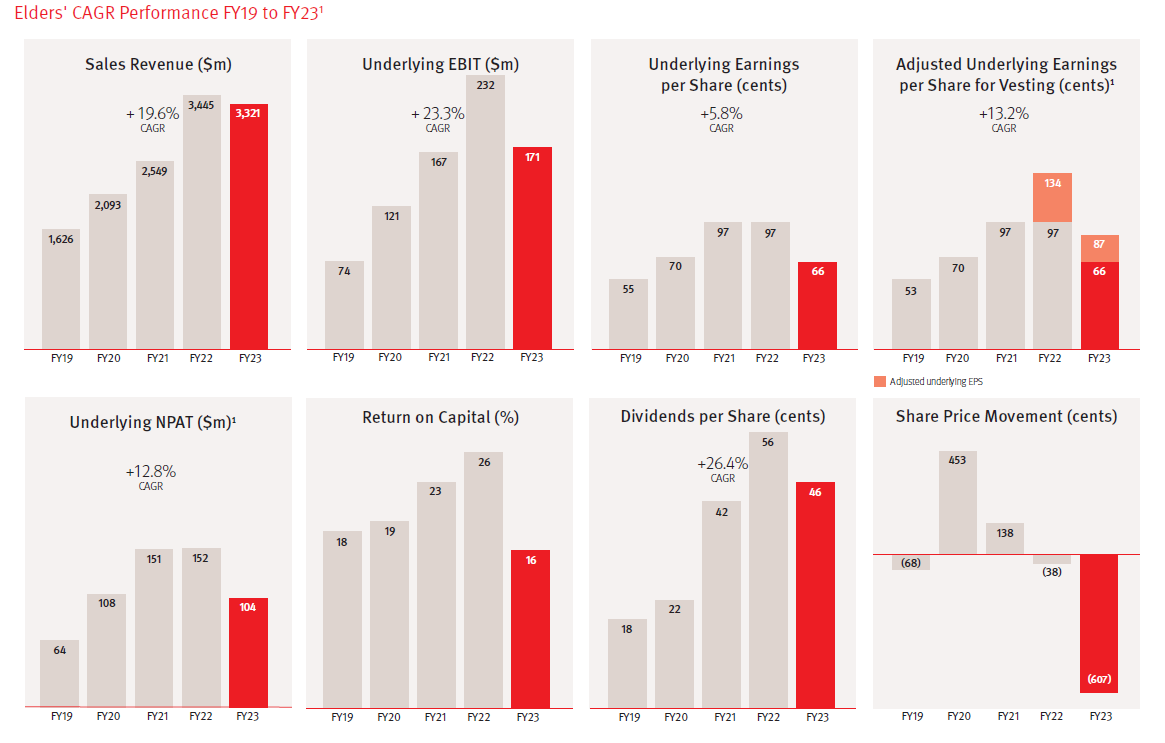

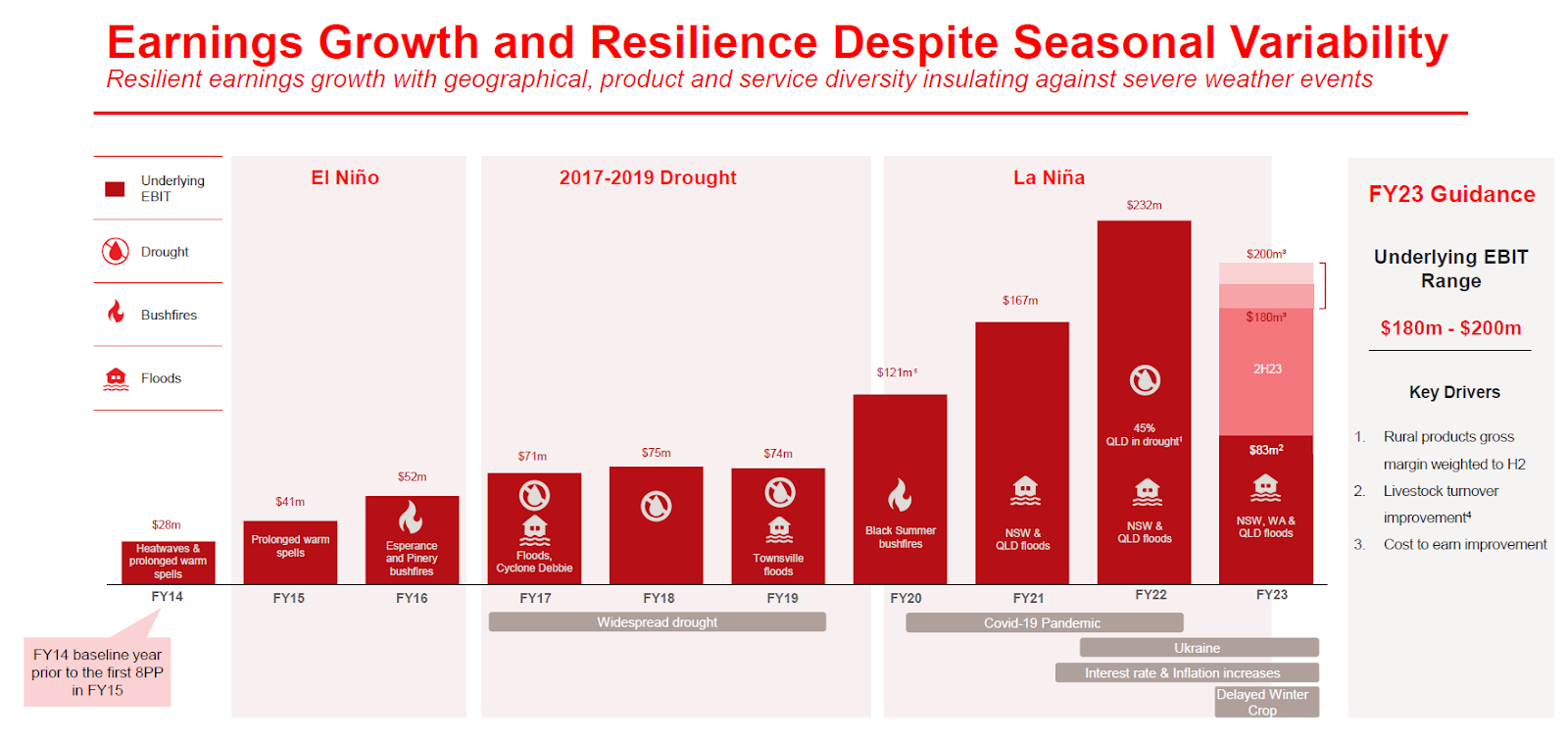

As can be seen from the chart above Elder’s revenue, earnings and ROC have more or less been in an upward direction since the financial year 2019. Financial year 2023 is the outlier with all the aforementioned figures down for the year. Given Elder’s size and coverage over all of Australia (The land of droughts and flooding rains) there is always one or more one off problems somewhere in rural Australia impacting farmers and their ability to buy goods and services from Elders. However in the financial year 2023 a number of factors have influenced Elder’s earnings. These include a delayed winter crop, interest rate and inflation, but mostly customers drawing down on their stockpiles bought from 2022 when there were fears of shortages due to supply chain problems causing farmers to overbuy and so reduced buying in 2023. Thus as stated at the beginning Elder’s is a cyclical business and usually the cyclicality is dealt with by its scale and diversification across Australia, but sometimes the size and number of the short term factors lead to lower profits and return in a given year.

The above graphic starting at 2014 makes Elder’s look like a compounder type business with earnings growing by low double digits each year and the occasional down year. However over the last 10 years Elders has gone through a transformation after a very poor performance following the financial crisis which its share price is still recovering from.

Prior to the financial crisis Elders was more of a conglomerate trading under the name of Futuris. Over the period after the financial crisis Elders divested businesses unrelated to agriculture, such as its automotive parts business and later on businesses that did not meet its ROC hurdle. It used the money from these divestments as well as considerable capital raisings to get its debt under control. The current CEO and Elder’s current strategy began in 2013 and as a result although the above graphic shows rapid growth this is taking place from a business being rebuilt and so is likely to at least slow in the future. In addition, despite Elder's competitive advantages, anyone owning shares should keep vigilant of Elder’s debt levels, ROC and that the business stays in its circle of competence, so there isn’t a repeat of 2009-2013.

Industry

Elder's success is tied to the success of its customers and the agricultural businesses across Australia which it serves. Based on the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) outlook from 2012 the demand for food is expected to be approximately 77% higher in 2050 than in 2007 at an average annual growth rate of 1.3%. Most of this increase is expected to come from Asia due to rising incomes where Australia has an advantage due to proximity.

Elders largest business within Australia is its branch network which is the second largest in Australia behind Nutrien. Together Nutrien and Elders account for about 2⁄3 's of Australian agricultural retail and the rest of the market is served by much smaller independence.

Australia, as the poem goes, is “the land of droughts and flooding rains” and so relative to other countries has a less stable climate, adding difficulty for farmers. Elder’s management team claims that now their coverage of Australia is broad enough that this is less of a problem due to the varied climatic zones in the regions covered by their store network. There is always a drought or flood or bushfire or other problem impacting farmers somewhere in their covered regions making this cyclicality less of an issue. However as can be seen this year there are a large number of factors that can impact farmers and their demand for inputs and so this business does endure cyclical lows such as the current one.

Future Prospects

As discussed above the demand for agricultural products is expected to increase until 2050 at a rate of 1.3%. This will require more inputs to make current farmed land more productive and to make more marginal land productive enough to farm. In addition to this, Elders has a number of other avenues to expand their business beyond increases in agriculture.

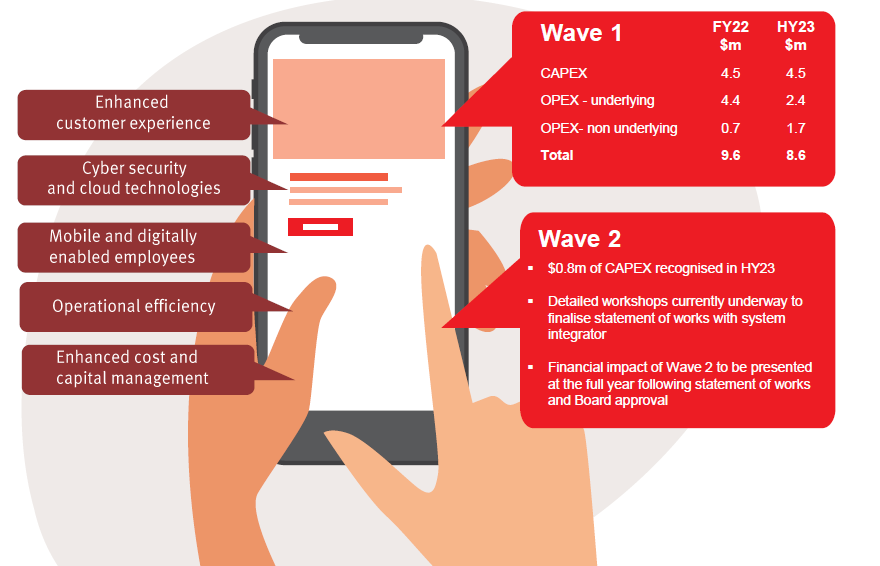

In 2022 and 2023 Elders completed a number of capex programs to improve the efficiency of its supply chain and store network that will lead to lower costs and enhance customer experience.

One of Elder’s main potential avenues of external growth and growth since 2013 is buying independent agricultural retailers. As discussed above Nutrien and Elders account for about ⅓ of agricultural retailers in Australia the remaining third are much smaller independents. These independents can be bought for much lower profit multiples than Elder’s currently trades and then Elder’s can increase profits and margins of the retailer by introducing its own products and making it a part of its more efficient supply chain. Then by controlling a larger section of the market for agricultural inputs it can lower its costs through greater scale, a type of distributive flywheel like effect. In addition to this there is also the possibility of international expansion with Elder’s with Elders increasing its stake in PGG Wrightson a New Zealand company in the same business.

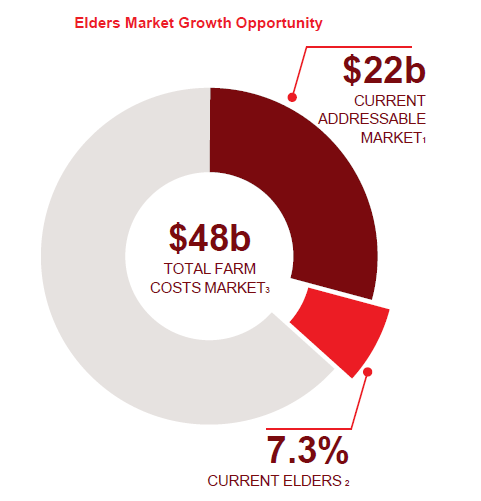

Another Elder’s strategy for growth is its backwardation strategy of buying suppliers of key goods, where potential returns meet their hurdle requirements. ABARES estimates that the current market of agricultural costs in Australia to be 48 billion with Elders estimates their potential addressable market in that of 22 billion and currently Elder’s revenue represents 7.3% of this market.

Balance Sheet

Elder’s debt currently stands at 463.3 million. This represents a debt to EBITDA of 2.14 times. In addition 206.3 million of this balance is made up of lease liabilities. They have interest coverage of over 11 times so should the rates of their debts go up as they have in recent years all the debt can be covered.

Most of the liabilities in Elder’s balance sheet is for running the business and not taken out as longer term debt and is manageable given its current levels. Given Elder’s past and cyclicality it is important to keep an eye on it, but very manageable at the moment.

Management Team

Mark Allison is the current CEO of Elders. He was appointed as a non-executive director in 2009 and then CEO in 2014 and presided over Elder’s turnaround. Mark has a 43 year career in agricultural businesses spanning technical, supply, manufacturing and distribution roles. He has worked at a number of companies including Wesfarmers, GrainGrowers Limited and Incitec.

Paul Rossiter is the CFO of Elders. He has worked for the business since 2009 and was appointed CFO in July 2023. His previous employers include Credit Suisse and Morgan Stanley.

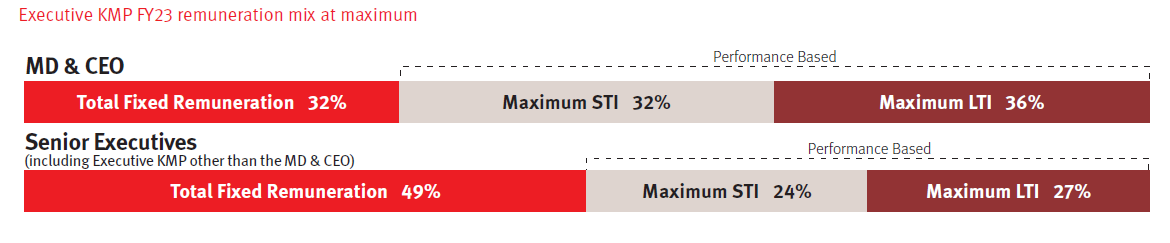

Elder’s compensation for senior executives is a mix of fixed base pay as well as short and long term incentives. The percentage breakdown of each of these varies based on the seniority of the employee with the percentage that is fixed pay declining with seniority and the percentage that is long term incentives increasing. As below:

The 2023 financial year was a volatile year for Elders stock price with the price reaching multi year lows. Coinciding with this there have been a number of insider purchases of Elders stock both as part of remuneration program and general market purchases.

One significant issue that has led to Elders stocks volatility in 2022 and 2023 are actions by management that have been interpreted negatively by the market. In November 2022 Mark Alison the CEO announced his retirement but this wasn’t greeted positively by the market with Elder’s shares diving over 20% in reaction to the announcement.

Then in early 2023 Elder’s stock fell another 7% on one particular day on no significant company announcements. When the ASX asked Elders for an explanation it was discovered there was a private investor briefing on that day, in which management claimed there was nothing new announced. This wasn’t taken well by investors either leading to further falls in the stock price.

Finally in June 2023 it was announced that due to the difficulty of finding a new CEO Mark Allison had been convinced to remain as CEO in exchange for a $410,000 pay boost and two year bonus of $1,000,000. Although this led to some limited share price recovery it has indicated to shareholders that the board and executive team had neglected one of their important responsibilities of succession planning.

So over the past year and a bit there have been a number of red flags by Elder’s management team. This management team prior to these recent events have however had a good long term track record creating a large amount of value for shareholders, so this should be further monitored. It would be good to see a more formal CEO succession plan at some point, especially given it has cost so much to retain Mark Allison and it’s only another two years before they face similar problems. The stock price has fallen enough that it more than accounts for these issues if taken in isolation and assuming they are not part of a larger trend.

Valuation

Over the past two years Elders stock price has fallen from a high of 14.39 to a low of 5.46 a fall of 62%. It is currently at 8.82 recovering significantly from its lows (and significantly since I started writing this at the beginning of January). It is currently trading at 13 times earnings and 8 times free cash flow which is on the lower side of its historic earnings multiples. However relative to past years this business's earnings are around cyclical lows (I won’t call cyclical lows as something unexpected and low probability to always happen next year to create greater lows) with per share earnings falling the most they have in 10 years from 97 cents per share to 66 cents. Thus there is a high probability of an earnings recovery, if it were to recover to close to 2022 earnings it would be trading at close to 9 times earnings, which is close to the lowest valuation it has traded at.

In addition Elder’s current historic valuation is relatively low in my view for a business that has managed to grow earnings at high rates and achieve high returns on capital over the past 10 years. In my view given its above average future potential growth, high returns on capital and dividend I believe it should trade in line with at least market averages of 15-16 times earnings. Maybe this is due to its past, it being grouped with relatively low quality agricultural businesses or a mix of the two.

Thus Elder’s at the moment presents a company trading at low earnings valuations, under earning, returning copious dividends to shareholders, growing the business and all for a low price.

Risks

General Agricultural risks

As with any other agricultural business Elders is affected by a large number of potential risks. These risks include commodity price risk, climatic risk, biosecurity infections of a large number of animals and geopolitical tensions affecting agricultural export markets or input markets. A number of these risks have been seen over the past few years with commodity prices and agricultural input prices particularly volatile in 2022 when Russia invaded Ukraine or climatic risks in various regions of Australia at any time. One way of reducing these risks relative to other agricultural businesses is Elders scale across Australia’s many climates as well as servicing farmers across many types of agricultural products diversifying away some of these risks. But despite that diversification some of these risks can still impact Elders top and bottom lines as can be seen this year.

Succession Planning

As discussed earlier in 2022 Mark Allison attempted to retire and had to be convinced to stay with additional money. This perhaps indicates a lack of succession planning on the part of Elders for key executive positions. It would be good to see some type of plan around this presented to shareholders so that there is not a repeat in the future where the company can’t do without a key executive.

Employee Injuries

The agricultural sector is in many parts more physically demanding than other sectors of developed economies such as Australia. As a result injuries to employees could give Elders a bad reputation as an employer not allowing it to pick the best employees to service its clients and be costly to Elders, taking care of injured employees. This is a key metric of executive remuneration and Elder’s over the years has continued to improve it. Financial year 2023 saw an average of 4.7 injuries per month across the entire business.

Summary

Elder’s is a high quality agricultural business operating in Australia with a good growth runway ahead of itself. Over the past two years it has had a combination of cyclical factors affecting its business and management issues which have left it underearning and at a cheap valuation. I expect a high probability of recovery in the next year or two to its former valuation and at least mid single digit growth.

I apologise I wasn't aware the link was collecting emails or...

Add ELD (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

$8.44 |

Change

0.080(0.96%) |

Mkt cap ! $1.328B | |||

| Open | High | Low | Value | Volume |

| $8.38 | $8.49 | $8.34 | $3.308M | 392.4K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 1 | 601 | $8.42 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $8.44 | 548 | 1 |

View Market Depth

| Last trade - 16.10pm 07/06/2024 (20 minute delay) ? |

|

|||||

|

Last

$8.43 |

Change

0.080 ( 0.91 %) |

||||

| Open | High | Low | Volume | ||

| $8.38 | $8.48 | $8.34 | 87124 | ||

| Last updated 15.59pm 07/06/2024 ? | |||||

| ELD (ASX) Chart |