FWIW IGO was flagging costs at Cosmos were likely to skyrocket within six months of the purchase …

And the environment has not become any easier with regards supply chain and labour shortages.

Also RUC Cementation one of the contractors on the project as of November 2021;

https://www.felix.net/project-news/...tracts-awarded-for-wa-cosmos-nickel-operation

https://www.ruc.com.au/projects/western-areas-cosmos-nickel-mine/

….. is currently in administration … (with Cosmos still on the go?).

cheers

https://thewest.com.au/news/kalgoor...e-than-double-the-original-estimate-c-8722190

IGO’s Cosmos nickel project to cost up to $825 million, almost three times the original estimate

Neil WatkinsonKalgoorlie Miner

Thu, 3 November 2022 2:00AM

IGO says developing the Cosmos project, which includes the Odysseus nickel mine near Leinster, will cost up to $825 million. Credit: Western Areas/Supplied

IGO says its just-acquired Cosmos nickel project near Leinster will cost up to $825 million to complete — almost triple the original estimate — partly because the company is increasing the nickel concentrator capacity.

IGO took control of Cosmos, where the Odysseus underground mine is being developed, when it picked up Western Areas in a $1.26 billion deal in June.

In its September quarterly report released to the ASX this week, IGO said total project costs to June 30 were $302m, and the company estimated another $493m to $523m would be needed to complete it.

“This includes all project development activities up until commercial production, plus the forecast costs to complete the shaft and shaft infrastructure that are expected to be completed around the end of CY23,” the company said.

“Accordingly, IGO estimates the total cost of the project, including the period prior to IGO ownership, to be between $795m and $825m.”

The company noted a KPMG independent expert report published in April estimated Cosmos would cost $425m.

IGO said this report had been issued to assess the reasonableness of IGO’s proposed takeover of Western Areas.

However, Cosmos’ price tag was $300m when Western Areas announced the project in 2018.

In explaining the extra cost, IGO said $150m was because of its optimisation plan involving scope changes to the project — which includes the expansion of the processing plant’s nameplate capacity to 1.1 million tonnes per annum from 750,000 tonnes per annum.

Another $140m was because of “timing” — which the company said was “items that were previously not classified in the project capital estimate such as sustaining capital or operating costs that are now included”.

Then there were “rectifications, omissions and escalation” of $95m “that were not included in the independent expert report that IGO has deemed necessary in order to deliver a safe, efficient and reliable operation”.

“It is estimated that between $400m and $425m will be spent in FY23,” the company said.

GR Engineering Solutions, which worked with IGO on the development of the Nova nickel-copper mine in the Fraser Range, this week told the ASX it had been awarded a contract variation to carry out the processing plant work at Cosmos, with the value of the engineering, procurement and construction contract now worth $76m.

IGO said it expected the plant to be completed during the third quarter of next year, with first concentrate to be produced from ore stockpiles at this time.

The company said shaft and associated infrastructure was expected to be finished by the end of next year, after which the hoisting of ore from the Odysseus shaft would start.

“IGO considers commercial production for the Cosmos project will be achieved when the process plant is capable of operating within acceptable limits of its intended operating capacity during the first quarter of FY24,” the company said.

https://www.afr. com/street-talk/murray-and-roberts-ruc-buyback-drags-on-macquarie-takes-a-peek-20230711-p5dnae

Murray & Roberts’ RUC deal drags on; Macquarie takes a peek

Sarah Thompson, Kanika Sood and Emma Rapaport

Jul 12, 2023 – 7.47pm

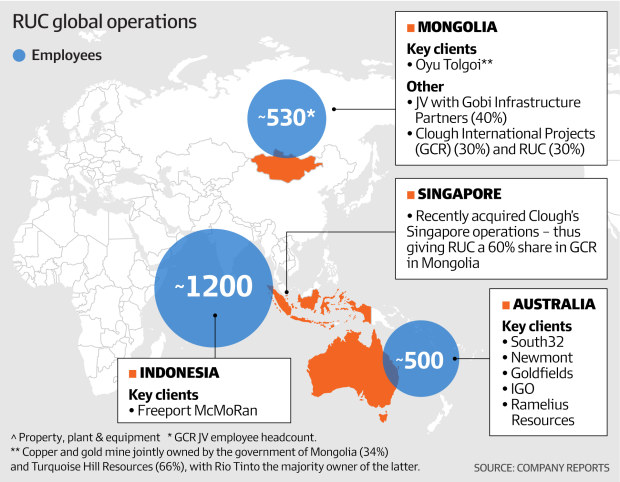

It’s one step forward, two steps back for Johannesburg-listed Murray &Roberts’ attempts to buy back Perth-based RUC Cementation Mining Contractors out of administration.

It is understood Macquarie held talks to come in as a lender to help Murray & Roberts mop up the deal. The bank weighed investing about $50 million via an asset-backed loan, which would have helped Murray & Roberts pay back creditors, regain control of RUC and end the saga of its Australian administration – which has already seen Clough sold to Italy’s WeBuild.

RUC is an underground mining specialist. Tamara Voninski

However, the talks between the two camps did not firm up into a deal. Macquarie is no longer on the scene, sources told Street Talk.

What it all boils down to is that Murray & Roberts is still trying to regain control of Perth mining specialist. RUC recorded $348 million in revenuesand $37 million in earnings in the 12 months to the end of June last year.

A spokesperson for Murray & Roberts declined to comment.

Deloitte, the company’s administrators, terminated Murray & Roberts’ deed of company arrangement on July 3, saying certain conditions precedent couldn’t be met. The termination came after the deal timeline was extended from June 30 to August 30, in line with an earlier report in Street Talk.

Harder than breaking rocks

The delay in getting a deal done – binding terms were agreed on March 24 – has already had bankers and advisers sharpening their pencils in case RUC boomerangs back to the auction block. However, there were no signs of Deloitte inviting competing bidders into the tent as of Wednesday.

Sources said RUC was shopped around with a $100 million price tag, and attracted interest from ASX-listed peers Perenti Group and Macmahon Holdings before its estranged parent won out. Its clients include South32, Newmont, Goldfields and IGO, while the service suite spans design, engineering, excavation, construction and commissioning services.

Those questioning Murray & Roberts’ ability to fund the deal have pointed to auditor PwC’s half-year review which said there was “material uncertainty related to going concern”.

The report added the business would have breached covenants at December 31, if its South African lenders hadn’t made some concessions. Asking its shareholders to fund the deal would be almost certainly out of question, given the share price is down 67 per cent year-to-date and 91 per cent over the 12 months.

Murray & Roberts would have its fingers crossed for a knight in shining armour to help it bankroll the re-acquisition. But if there is one, it’s well hidden.

Ann: Impairment of Western Areas Assets, page-21

Add IGO (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

$5.09 |

Change

-0.130(2.49%) |

Mkt cap ! $3.854B | |||

| Open | High | Low | Value | Volume |

| $5.16 | $5.17 | $5.04 | $16.90M | 3.322M |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 2 | 700 | $5.06 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $5.09 | 13400 | 2 |

View Market Depth

| Last trade - 16.10pm 08/08/2024 (20 minute delay) ? |

| IGO (ASX) Chart |