Interesting info translated from Chinese, Chinese smelters are obviously struggling. Profit margins between 100 to 300 yuan/tonne (US$13 to US$40/t).

At the lowest power price of 0.43 yuan/kWh ( US$0.06/kWh) this is still US$250/t more than OM Sarawak. The Chinese export price cost would be US$1,350 to US$1,375 /t FOB. Cost of OM Sarawak should be under US$900/t FOB. CIF Japan is currently US$1,430 so OMH should still be making US$300 to US$400/t profit CIF Japan.

Ferroalloys continue to find the bottom in the medium term

2023-06-21 00:12

Terminal demand has not improved

On the one hand, the low profits of steel mills suppressed the purchase price of raw materials, and the bidding price of ferroalloys in steel mills continued to decline in June; on the other hand, with the recovery of corporate profits, some ferrosilicon manufacturers began to resume production, and the output of ferrosilicon will increase later. Therefore, ferroalloys still maintain a weak operating point of view in the medium term.

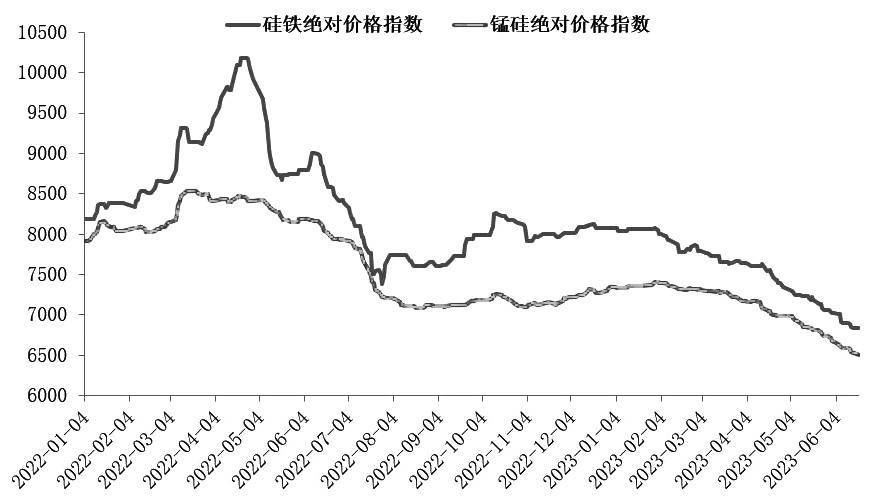

The picture shows the absolute price index trend of ferrosilicon and manganese silicon (unit: yuan/ton)

Since the beginning of the year, the price of ferroalloy has been on a downward trend. The reason is that, on the one hand, the downstream demand has weakened, and at the same time, the production capacity has been oversupplied; Looking forward to the market outlook, we believe that the oversupply of ferroalloys has not improved, the profits of steel mills are low, and the purchase price of raw materials has been lowered. The immediate production profit of the enterprise rebounded

Since the beginning of the year, the output of manganese and silicon has remained at a high level, and the operating rate of manganese and silicon manufacturers has remained at around 60%. The total output of manganese and silicon in the first five months has increased by 4.29% year-on-year, and the output of manganese and silicon in May continued to grow month-on-month. The high production of manganese and silicon is mainly contributed by the two production areas of Inner Mongolia and Ningxia. The above two production areas have obvious advantages in electricity prices, and the production profit is about 100-300 yuan/ton. Among them, the production of manganese and silicon in the Inner Mongolia production area accounts for a large proportion and the profit is better Driven by profits, the operating rate of this production area remains high, and production in other areas continues to suffer losses. However, with the reduction of electricity prices, manufacturers in the south have plans to resume production. It is expected that the supply of manganese and silicon will continue to rise slightly month-on-month.

Low profits have led to a continuous decline in ferrosilicon production since the beginning of the year. In the first five months, ferrosilicon production fell by 13.64% year-on-year. In May, ferrosilicon production fell by 24.46% year-on-year. The average operating rate of ferrosilicon manufacturers remained at around 38%. In the early stage, the profit of ferrosilicon production was low, and only the production areas in Inner Mongolia and Qinghai kept the profit below 100 yuan/ton. Recently, with the drop in the price of semi-coke small materials, the profit of spot production of ferrosilicon has rebounded, and the profits of Inner Mongolia, Qinghai and Ningxia production areas have risen to more than 300 yuan/ton. With the recovery of profits, some ferrosilicon manufacturers have begun to resume production. Ferrosilicon production will increase later. It is more difficult to increase the price of manganese ore

Since the beginning of the year, the price of manganese ore has continued to weaken, and the inventory of manganese ore ports has been in a state of accumulation. In mid-May, with the decline in the number of manganese ore arriving at the port, the port inventory of manganese ore began to decline. At present, the port inventory of manganese ore is about 6.2 million tons, which is still a year-on-year increase. It is at the highest level in the same period of the previous year. In June and July, overseas manganese ore quotations to China continued to fall, and manganese ore cost support was weak. There is a global surplus of manganese elements, and the superimposed demand has weakened, making it difficult to raise the price of manganese ore.

Coke supply and demand are mismatched, and the price of coke has dropped by about 350 yuan/ton since May. Coal prices have fallen sharply, and semicoke cost support has weakened. Although semicoke industry associations in many places proposed to limit production and protect prices in April, semicoke prices have stabilized in the short term, but demand has fallen sharply. The price of semicoke small materials has fallen by 430 yuan since the end of May. / ton, the price may weaken further in the later period.

There is a large difference in the cost of electricity for ferroalloys in the north and the south, and the northern production area has an obvious advantage in electricity costs. The cost of electricity in the main production areas of Inner Mongolia is the lowest, currently around 0.43 yuan/kWh. Recently, electricity tariffs in Ningxia and Yunnan production areas have been lowered. According to feedback from individual enterprises, electricity tariffs in Yunnan will drop to the same level as those in Inner Mongolia production areas in June and July. Changes in electricity prices in major production areas have narrowed the gap in the production cost of ferroalloys between the north and the south, but the electricity prices in the north still have an advantage. Overall, the prices of manganese ore, coal and electricity, which account for a large proportion of the cost of ferroalloys, have all declined, and the cost of ferroalloys has further decreased.

Since the second quarter, the steel industry’s demand for ferroalloys has continued to decline. The demand for downstream infrastructure and real estate for steel is unlikely to improve significantly. The demand for manufacturing is also weak. Downstream demand is about to shift from the peak season to the off-season. It is unlikely that the end demand for steel will rebound significantly. . Steel mills are less willing to take the initiative to restock ferroalloys, and maintain low inventories of raw materials. Compared with the same period last year, the steel intake of mainstream major manufacturers is at a historically low level. The low profits of steel mills suppressed the purchase price of raw materials, and the bidding price of ferroalloys in steel mills continued to decline in June.

Overall, ferroalloys are still in the stage of oversupply. With the reduction of electricity prices and semi-coke small material prices, the production costs of manganese, silicon and ferrosilicon will drop. Driven by profits, the output of the two will rebound slightly, but the downstream demand has not improved. The demand for real estate, infrastructure and manufacturing has not seen a significant improvement, the demand for steel products is weak, and the profits of steel mills are low, which will continue to depress the purchase price of raw materials. The price of ferroalloy has not yet bottomed out, and the medium-term view is still weak.

(20min delay)

(20min delay)