It's hard to compare PLS and CXO, but i'll add my 2 cents worth as I've been a holder of both companies and i'm confident of CXO hitting a market cap of > $300m (approx 50c).

Everyone keeps getting held up over the resource size. Yes, PLS has a giant resource, but they are only producing 314,000 tpa (as per the DFS). CXO is looking to produce 225,000 tpa. So while the resource is considerably larger, you can't sell it all at once, and this is the big thing people are forgetting - you can only sell to the customers you have, and they can only consume so much per year. So the big resource isn't the only thing to consider.

Most companies have a valuation using a PE of between 10 to 15, that means that CXO needs to get to a 10Mt resource to see a PE of even close to 10 (assuming no increase to the 1Mtpa DMS processing plant). Looking at the drill results recently, I have penciled in between 10Mt and 13Mt, and I think it's fair to assume there is plenty more to be found (IMO - we will easily go > 20Mt)

So if both PLS and CXO are selling the amounts stated above (considering a 10 year period) the market cap should be reflective of that and not just the total resource size, otherwise companies would trade at PE's of the LOM.

The next thing that would push the higher CXO market cap case is the projected pricing and operating costs (obviously there is a lot of subjectivity here).

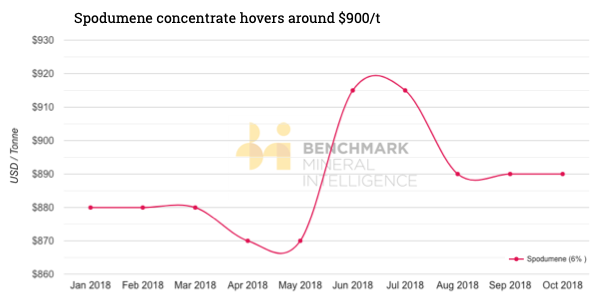

Based on the PFS the CXO NPV numbers are using US$649 as the price, which we know to be low based on other Lithium miners and the below (Note: 6% spod - the CXO PFS uses 5% spod, but I expect this is likely to be updated in the DFS).

CXO have also suggested a very low operating cost of A$371 (US$278) (see below)

PLS is significantly higher (see below)

It's to the point where CXO's profitability p.a. could very well be similar to PLS despite the smaller plant, if they can achieve the same/similar sales price.

The obvious big thing going for PLS over CXO is the ability to significantly expand the plant and have the spod to feed it, plus the bonus Tantalite sales. If they do this then the market cap will grow based on the next 10 to 15 years increase in expected revenue/profitability.

So I guess what I am saying is that it isn't so simple to compare the two, particularly when CXO keeps finding more tonnage. If the CXO cost assumptions are correct (Note: I remain somewhat skeptical as things almost always cost more than anticipated), then this thing will be highly profitable and IMO go above a $300m market cap. If they can hit between $100m to $140m EBIT p.a. then it stands to reason that at least a 5x (if not 10x) market cap on those earnings is possible (with supporting LOM).

Note: I expect the DFS will be delayed to include the recent drilling, but particularly the Lees/Booths link so they can push the LOM to > 10 years. It looks way better to release a DFS that says NPV of $700-$800m, than it does saying NPV of $350-400m, particularly for a $35m company. I'm happy to wait, the fundamentals are only going one way.

Have a good weekend all.

Ann: Maiden Sandras Mineral Resource Grows Finniss to 6.3Mt, page-68

Add CXO (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

10.3¢ |

Change

0.006(5.67%) |

Mkt cap ! $213.6M | |||

| Open | High | Low | Value | Volume |

| 10.0¢ | 10.5¢ | 9.8¢ | $995.7K | 9.951M |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 25 | 1074598 | 10.0¢ |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| 10.5¢ | 3651528 | 53 |

View Market Depth

| Last trade - 11.04am 11/07/2024 (20 minute delay) ? |

| CXO (ASX) Chart |