If anyone knew the answers candidly to this we'd all be billionaires. Well we wouldn't because it's a transfer of wealth from one to another.

Without overcomplicating it.

Share prices go up on announcements when it exceeds market expectations and goes down when it underwhelms. Evidently the market expected a better result than what was presented.

Personally think many saw the IRR and NPV and thought that's lower than what i've been reading. 'sell'. Then it's a case of herd mentality. It's down 5% must be bad 'sell'.

Additionally, a lot of people have done really well on IXR over the last 12-18months and many would have been hoping for a tidal wave of buying leading up and upon the SS to finally take some profits. When that sugar hit didn't come we saw price softening and subsequently people forced to offload at whatever the market was offering in fear that the subsequent days and weeks to follow the price offered will be even less.

IXR is no longer a sugar hit riding the wave of exploration. 2024 H1 is targeted as the production timeline and for some those timeframes just don't work. Even if the reward come production is significant. I reflected though on Chinalco's MOU and the fact they've done 12months of due diligence to even agree to an MOU. As far as I'm aware they don't own any large stake in IXR but the MOU's in principle was listed for offtake and potential equity so they're obviously interested even when we were 5c+. I think that the largest global rare earth company by MC would have done better DD in the last 12 months than the buyers and sellers who based their investment choices today by spending 10-30mins speed reading the 58 page document. Highly probable that mobs like this or big end of town are the ones buying the share between now and production.

If you're chasing huge returns in short timeframes then IXR probably isn't the stock for you. Chinalco's investment timeframe would be thinking min 3-5year timeframe and then the profitability over the life of the project. Typically, the big end of town has the patience to outstrip to urgency of a lot of retail and IMO over the next 12-24months we'll see much of the retail handing their shares over to the insto/sophs/brokers etc. Of the 250M shares exchanged today there will be a lot of retail selling to retail who probably will in turn sell this again in the next 2-6 months because no lambo. I've been pretty cautious with buying into IXR with any further capital massive funding as I have been expecting an inevitable selloff and major low somewhere in the development cycle of IXR. I'm waiting for full capitulation of patience as I'm pretty content to launch back in as we commence the grind to production.

There's a good suite of news between now and the BFS confident that as the project de-risks you can then apply a high proportion of value relating to economics. When you understand discounted FCF you'll realise it's highly depending on your revenue in the early years. If you assess project based on the NPV and IRR i agree doesn't look favourable. If you look at a true LOM EBITDA then it's outstanding.

LOM ebitda is 1.7bn AUD or Post tax 1bn. So essentially, close to 100M AUD profit per annum. Obviously the stage production profile means it's lower initially and then higher at 12.5mtpa throughput. Irrespectively, it's on average close the the market cap in post tax revenue.

For context. If the company paid all that annual revenue as a dividends then if you held 1M shares = worth 38k at todays value you'd receive a 28.5k dividend.

What i'm more interested in is the 12.5mtpa ebitda. Which as suggested is 3800tpa which a rough margin of $50 (even at the lower end of the forecast come that period) we're still talking 190M USD = $244m AUD. Again, if that was all profit and you held 1M shares (todays value) = 38k then dividend is 70k.

So appreciating that production is a ways off but if you look at those profits in terms of EPS or a dividend payment to me it starts to show the significant upside but with some patience. It's probably worth factoring in some further dilution for debt/equity arrangement so you can probably reduce those by 20-25% and we're at ~30k dividend for first 11year whereby Y9 onwards would be around 52k.

If a company had no growth and gave all profit as dividend i was would expect a 10-15% yield. i.e. the dividend is worth 10-15% of the stock. So if we accept that it could be between 30-52k in it's production state then this would need to formulate roughly 12.5% of what the total stock would be worth. Takin the middle point of both then 328k holding yields a dividend of 41k (midpoint). If you consider a company value in this manner then you arrive at roughly 10 times upside from one's holding today. Reminding that theres companies like GRR for example who pay a similar yield and recently their share price tripled on IO price so i think there is upside to that in growth.

Irrespectively, I can see how the market dislike the announcement and short to mid termer it was time to cash in as we now enter the grind phase which is probably much less appealing but fairly well de-risked.

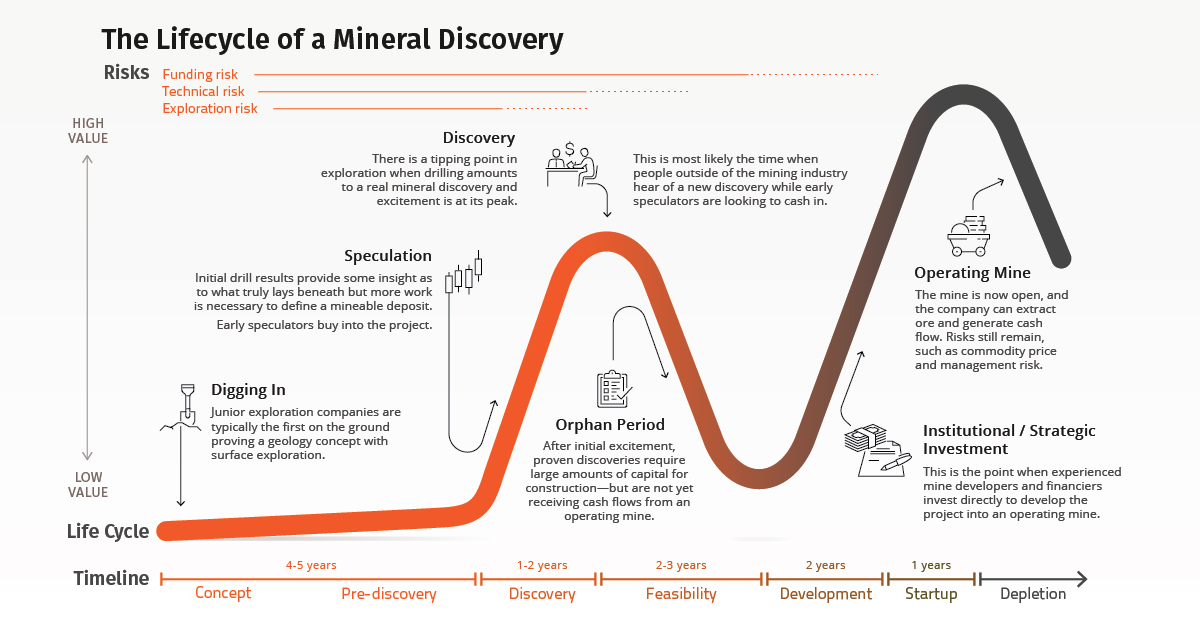

We are in feasibility noting the timeline they have has 5/6 years from feasibility to start up. We are looking a 3Y. with 1Y of that construction. These graphs above are not to scale and not all stocks fit this perfectly but to some extent even if the price heads sideways the above graph is a pretty good indication of sentiment and movement.

Noting construction is end of 2023. We've got 18-20months before we're half way up the second ramp. So at some point between the exploration hype we've all just experienced and end of 2023 there will be a bottom of some form. Now would again say that this isn't a catch all graph. There's quite a few stocks that simple head sideways whilst going through the PFS/DFS stages etc. I would also suggest that the "large amount of capital" is muted for us as we are fully funded through to BFS. Additionally the period to BFS completion (which construction scheduled to start slightly afterwards) is 16months from today. So it's not a massive timeframe, no massive capital requirements to get to that phase so i would garner that at some point market will reach it's capitulation of patience at some point in the next 18months and for me i'm quite comfortable with that and look forward to taking that opportunity to increase exposure.

*Disclosure buys for me is 3.7c as i see short term support between 3.6c-3.8c. Think we still might see the pro's pressure the retail hands here and second lot of buys is down at 2.8c which is the next major logical test of supply. That's a MC of around 90-100m which would place it inline with biolantanidos. Ironically, we've only just been allowed to present almost exactly the same tonnage as them despite there being evidence of another 230mT and exploration upside of another 300mT IMHO. But anyways some people here might absolutely panic at that thought and think i'm speaking unrealistic but if i've learnt anything in my time investing is to expect the unexpected. I'm not selling at these levels as to be frank i've never been astutely good at predicting exact top's and bottoms, which is evidenced by the fact 24 months ago where some sat on 70/60/50% loss. For some the notion of 2.8c or even today's value of 3.8c can be very painful and hence my comments that it's sometime good to be conservative and in the spec end always good to take some profits when they present. I'm one of the fortunate ones with a .4c average but if i was entering this stock i think 3.6c-3.8c would be a decent initial entry (hence i have buys there) and i think 2.8c would be the hail mary hope of entry and tbh i'd be pretty shocked if it went lower as that would be lower than biolantanidos which only has 80mT at half the grade and was a T/O 2 years ago i'd hazard that company would sell for twice or 3 times as much today and so on that you can make a case for undervaluation today.

In the end market chooses valuation and as investors you're trying to outwit as inevitably every time you buy a share it's from someone that thinks this is overvalued now. Everytime you sell it's to someone who see's it as undervalued. Not everyone can get it right.

I usually liquidate heavily in development but truthfully am staying the course here as the production timeline isn't that far off. It's a world class asset, in a severely high demand sector. Those without the 2-3y vision are the ones selling which is fine but it's probably to like minded individuals whom are position themselves over the next year to capitalise on the next 30.

Philosophical food for thought.

SF2TH

(20min delay)

(20min delay)