Pgiam

Early-stage, growth-driven independent natural gas exploration and production (E&P) company, Tamboran Resources Corporation (NYSE:TBN), has combined an attractive location, unique unconventional natural resource assets, and its US style drilling techniques, to create an investment proposition that is compelling. However, that proposition remainslargely speculative. I recommend not investing in the firm as of yet, but putting it on a watchlist.

The Business Model

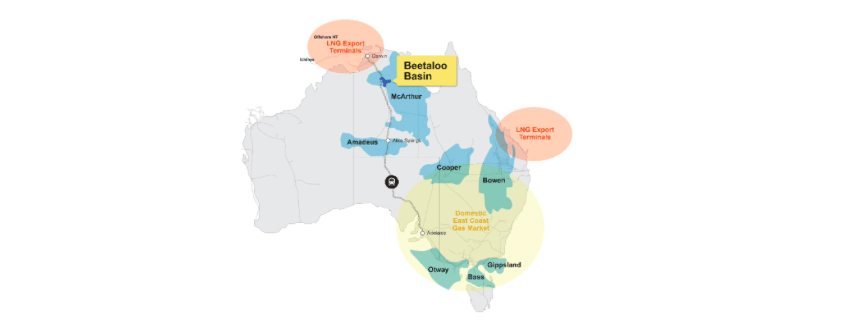

Tamboran employs an integrated approach to developing its unconventional natural gas resources in the Beetaloo, in Northern Territory, Australia. The Beetaloo covers some seven million acres (10,800 square miles) -around the size of Belgium-, and contains large amounts of unconventional natural gas resources. It is a part of the Greater McArthur Basin in the Northern Territory and is found some 300 miles southeast of Darwin, Northern Territory.

Source: Tamboran’s 2024 10-K

Source:Tamboran’s 2024 10-K

Evidence suggests that the natural gas found in the area has lower carbon dioxide than that produced elsewhere in Northern Australia and other fields that supply the East Coast gas market. Tamboran’s bet is that its use of U.S. drilling and completion technology will give it an edge in terms of achieving natural gas production that complies withAustralia’s greenhouse gas (GHG) regulations. The government aims to attain net zero carbon emissions for the whole economy by 2050. Shale gas production in the Beetaloo post-commercialization should be done through Scope 1 net zero emission basis. According to the 2024 10-K, Tamboran wants to reach net zero equity Scope 1 and 2 GHG emissions once it has begun commercial production.

The company and its working interest partners have exploration permits (EPs) for around 4.7 million contiguous gross acres in Beetaloo. As an early-stage company, Tamboran is pre-revenue. The company’s portfolio consists of assets such as 25% non-operated working interest in EP 161; 38.75% operating working interest in EPs 76, 98, and 117; and 100% operating working interest in EPs 136, 143, and EP(A) 197. The Sydney, Australia headquartered company was formed in 2009, and has been listed on the Australian Stock Exchange (ASX) since July 2021 and, inJuly 2024, went public on the New York Stock Exchange (NYSE).

There are three steps to the company’s development of its assets. In the first phase, the company will transition from exploration to commercialization; secondly, build its drilling program for production for the Australian East Coast and Northern Territory markets; and finally; after commercialization, drilling more wells to export liquified natural gas (LNG) plants in the Middle Arm Sustainable Development (MASD) precinct Darwin and the company’s proposed 6.6 Mtpa Northern Territory LNG export facility (NTLNG) for the South and East Asian markets.

Pre-Revenue, Therefore, Loss-Making

Tamboran has not yet begun natural gas production, so is pre-revenue and does not earn any other income. It is not surprising then that the company is at present unprofitable. The company’s net operating profit after tax (NOPAT) has remained within a tight range since 2023, from -$22.9 million in 2023 to -$22.6 million in the trailing twelve months (TTM), as the table below shows.

Economic Category (Values in millions) | 2023 | 2024 | TTM | |

GAAP Net Income | $ (32.03) | $ (21.92) | $ (24.62) | |

Total Hidden Non-Operating Expense, Net | $ - | $ - | $ - | |

Reported Non-Operating Expense, Net | $ 13.02 | $ 3.36 | $ 2.85 | |

Change in Total Reserves | $ - | $ - | $ - | |

Interest for PV of Capitalised Operating, and Variable Leases | $ - | $ - | $ - | |

Non-Operating Tax Adjustment | $ (3.91) | $ (1.01) | $ (0.85) | |

Reported After-Tax Non-Operating Expense/(Income), Net | $ - | $ - | $ - | |

Net Operating Profit After Tax (NOPAT) | $ (22.92) | $ (19.57) | $ (22.63) |

Source: Author calculations and company filings

1) Non-operating expenses not recorded on the face of the income statements, compared to those reported on the face of the income statement.

In that period, returns on invested capital (ROIC) have increased from -13.8% to -6.4%.

Tamboran Will be a Winner in the Transition

Empire Energy managing director Alex Underwood, whose firm also operates in the region,said that, “This is a huge resource, I think the Beetaloo contains around enough gas to supply Australia for the next 400 years.” The company’s most obvious competitive advantage lies in the fact that it is the leading acreage holder and operator in the area. The company’s 2-D seismic data indicates that its assets contain large amounts of high-quality natural gas in what Tamboran believes is the core of the Velkerri shale gas play. The average shale thickness of the Middle Velkerri-B shale shows is 230 feet over around 610,400-acres (or 950 square miles). The company believes that the Middle Velkerri section is continuous over the area.

Secondly, competition in the Beetaloo is limited. The geography of the region, the contiguous nature of the firm’s acreage, and the absence of restrictive boundaries, means that the company can execute its strategy and deploy 10,000-foot laterals as well as U.S. style unconventional drilling techniques. The company’s scale also means that it can produce in large volumes, enjoying economies of scale and stimulating investments in in-basin frac sand and other services.

Finally, the Beetaloo’s closeness to the Australian East Coast and the Asian LNG markets means that it not only has access to attractive markets, but it will be able to negotiate for attractive prices compared to those in North America. The company cites figures from 2024, in which “spot prices for natural gas delivered from Henry Hub averaged $2.20 per MMBtu. Over that same period, the Japan Korea Marker (JKM) continuous futures price of LNG averaged $11.23 per MMBtu.” At present, production costs are higher in the Beetaloo compared to North America, but scale economies should push those down with time.

The Company is in a Strong Cash Position

In the TTM, the company has burned through $33.6 million in free cash flow (FCF) at a monthly burn rate of $2.8 million. The company has cash and cash equivalents of $74 million, giving it 26 months until it needs more capital. With interest coverage of 16.23, I feel that the company is in a strong cash position to continue to press for its goals.

Company | Ticker | Interest Coverage Ratio | Cash on Hand ($thousands) | TTM FCF Burn ($ thousands) | Runway in Months | |

Tamboran Resources Corporation | TBN | 16.23 | $ 74.04 | $ (33.62) | 26 |

Source: Author calculations and company filings

Valuation Reflects Early-Stage Opportunity

A company’s intrinsic value is its NOPAT capitalized by the cost of capital, added to any non-operating assets, net of non-operating liabilities, that the company has. As a pre-revenue company, Tamboran cannot help but trade at a negative intrinsic valuation. In the TTM, the firm’s NOPAT of -$22.6 million is capitalized by 9.9% cost of capital, to which we add the value of its assets held for sale, and deduct the value of its noncontrolling interests, to get -$272.7 million, compared to a market cap of $307 million. What this means is that the market believes that the present value of growth opportunities (PVGO) is $579.8 million. At present, there is no evidence to say that the company can ever grow NOPAT enough to match that. This does not mean it will not happen, just that there is no evidence for that as yet.

Conclusion

Tamboran is well-placed to take advantage of its key competitive advantages to become a leading and profitable supplier of unconventional natural gas. It has the potential to enjoy scale economies, is well positioned, and its resources are attractive. The company’s current lack of profitability is natural. A consequence of that is that its intrinsic value is negative. A lot of speculation is built into the price. I do not recommend investing in the business, but would put it on a watchlist.