Ardea Resources: A Leveraged Nickel And Cobalt Optionality Story Worth Tracking

Aug. 13, 2019 1:05 PM ETArdea Resources Limited (ARRRF) Summary

The price of nickel has been surging of late and is now up over $7/lb.

Fears over an Indonesian export ban are likely contributing to the short-term price spike, but the outlook for nickel remains bullish longer-term due to an expected surge in battery demand.

Ardea Resources controls a large nickel laterite resource, the Goongarrie Nickel-Cobalt Project, which is currently an "optionality play", but it may soon become viable if nickel keeps on soaring.

The company is focused on landing a strategic partner to help with financing, and with peer Australian Mines recently announcing an off-take deal, interest from third parties could be picking up in the nickel space.

Shares of ARRRF also provide additional leverage to the cobalt price, and with Glencore recently announcing plans to stop operations at the world's largest cobalt mine by year's end, a perfect macro storm of rising prices for both nickel and cobalt could be setting up, which if it happens, would greatly benefit a company like Ardea Resources.

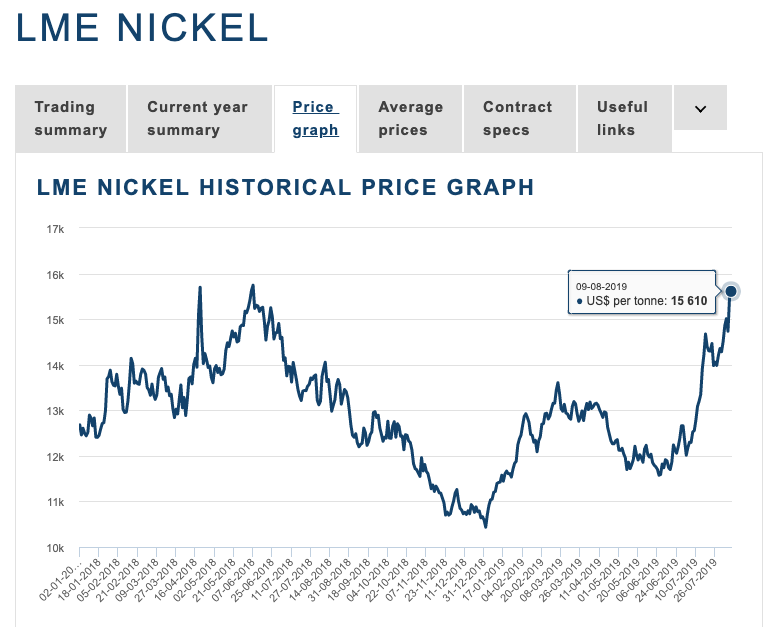

While many base metals have been struggling over the last few months or so (e.g., copper, zinc, tin, etc.), there is one outlier that has been bucking the trend, and that's nickel.

As the following chart shows, the price of nickel has been experiencing a resurgence of late (since the start of January 1, 2018), and the LME nickel price is currently trading at $15,610/t.

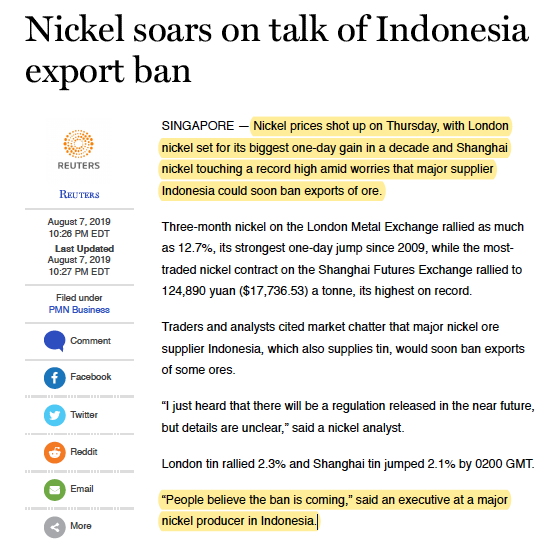

Granted, much (or perhaps all) of the recent spike up in the nickel price likely has to do with growing concerns that Indonesia might take action to ban nickel ore exports earlier than originally anticipated (moving up the date from 2022), which is noteworthy because the country has been the world's largest producer of the metal.

With that said, looking slightly further out into the future, the above price action seen in nickel so far in 2019 might just be indicative of an ongoing developing bullish trend.

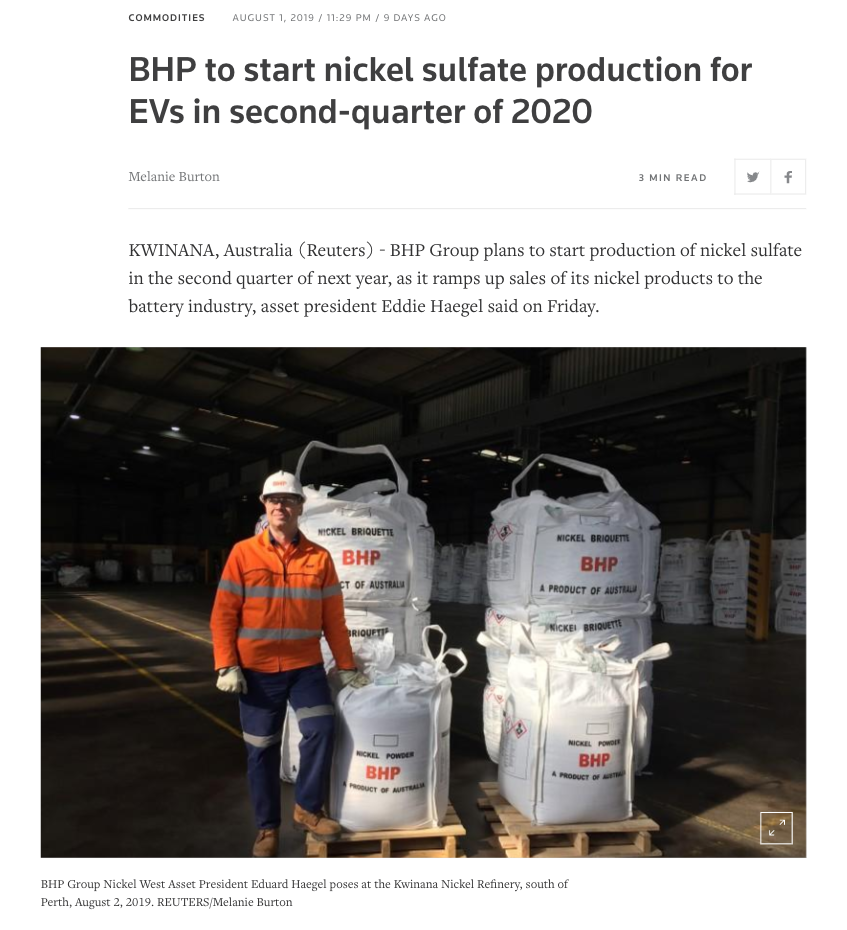

Over the next few years/decade, "battery supply shortages may be linked to rising demand for nickel" due to the expected arrival of the electric vehicle revolution.

Compared to other battery metals, BHP Group's asset president Eddie Haegel had these thought to share with the market, most recently:

We anticipate that there will be no sustainable premium in the lithium sector, whereas we think that is not the case for nickel," Haegel told a media briefing at the plant.

We think that in the medium to longer term there will be a margin that will be sticky for nickel, and so we consider it an attractive commodity."

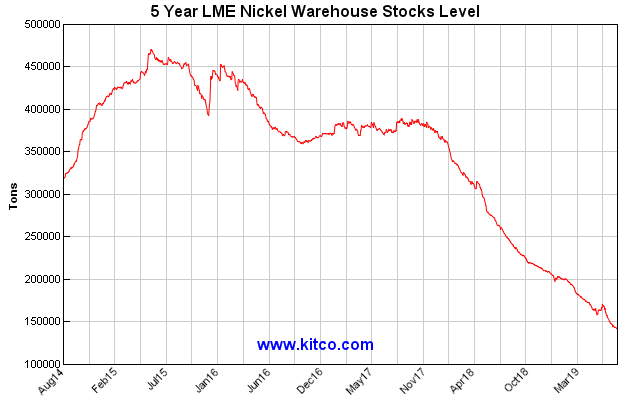

Further, dwindling LME nickel warehouse inventory over the past 5 years certainly doesn't hurt the case for a bullish longer-term narrative towards nickel.

Source: *****

So, while all the hype over 2017-2018 was centered primarily around the battery metals lithium and cobalt, it's starting to look increasingly likely that nickel will be next in line to have its turn in the spotlight.

As such, due to the sheer size and scale that some of the larger laterite deposits out there have to offer up (particularly those found in the "safe and stable" jurisdiction of Australia), these "optionality plays" (in general, nickel laterite projects offer lower-grades and require much more initial CAPEX to get off the ground than many of their nickel sulphide peers) will be worth tracking most closely, sort of as a barometer, to gauge just how much speculator interest is developing for nickel.

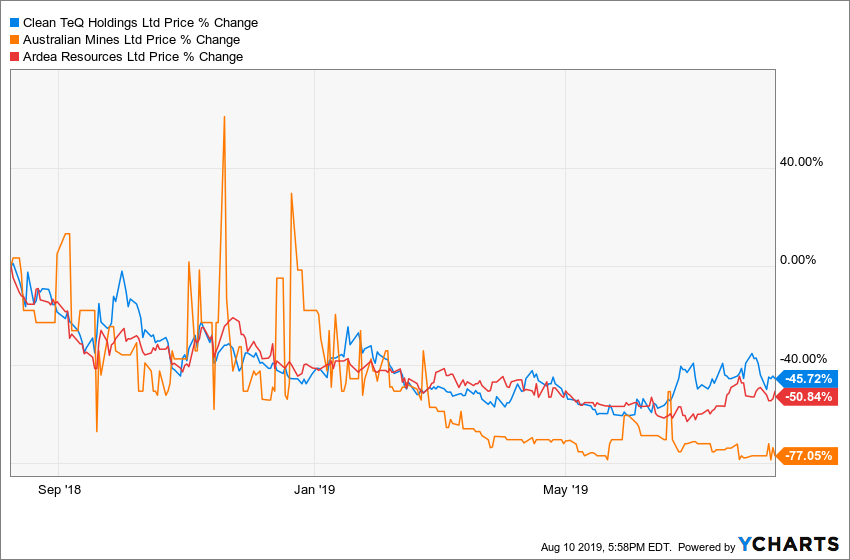

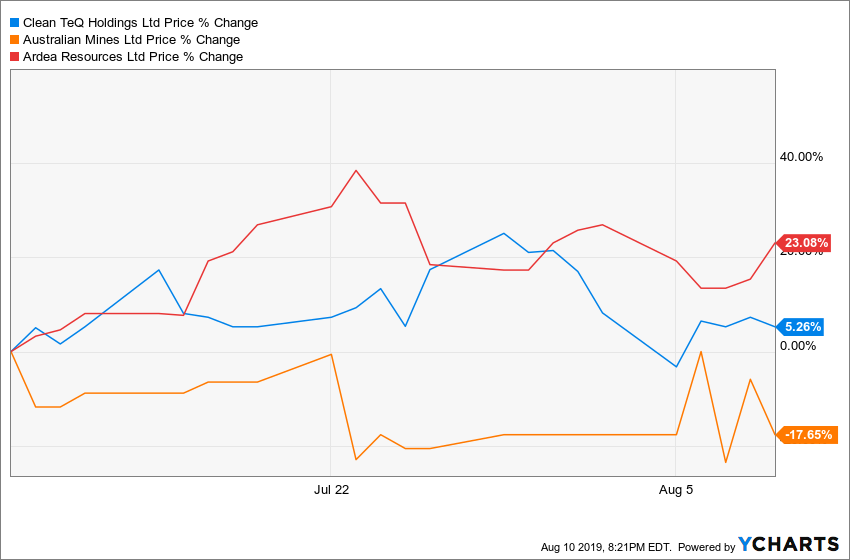

However, a turnaround story may now be starting to unfold, particularly for Ardea Resources, which has so far been distancing itself from the pack, over the last month.

CTEQF is up 5.26%.

AMSLF is down -17.65%.

ARRRF is up 23.08%.

Shares of ARL.AX (the native ticker symbol of ARRRF) are now trading at A$0.50/share.

Let us now take a closer look and examine what the Ardea Resources story is all about.

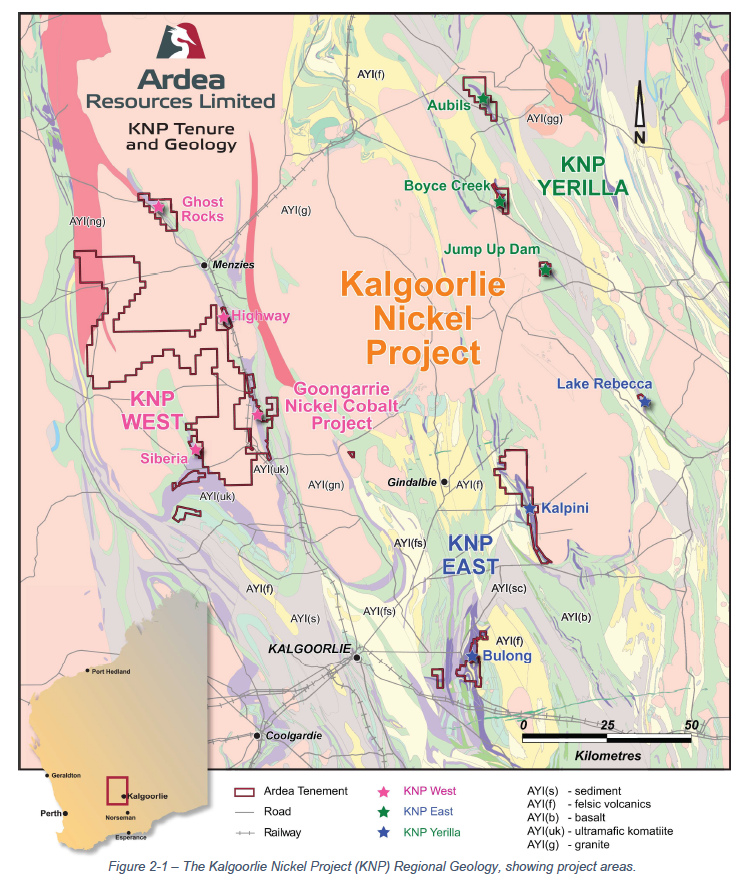

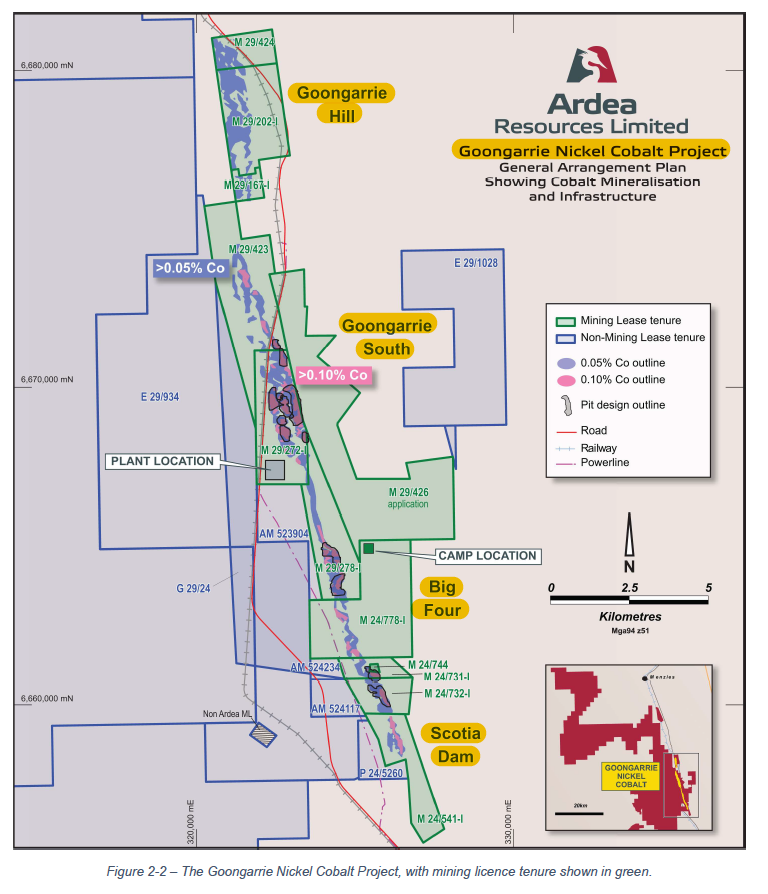

The Kalgoorlie Nickel Project/Goongarrie Nickel-Cobalt Project

Ardea Resources has a 100% ownership stake in their flagship Kalgoorlie Nickel Project (KNP), which is located in Western Australia.

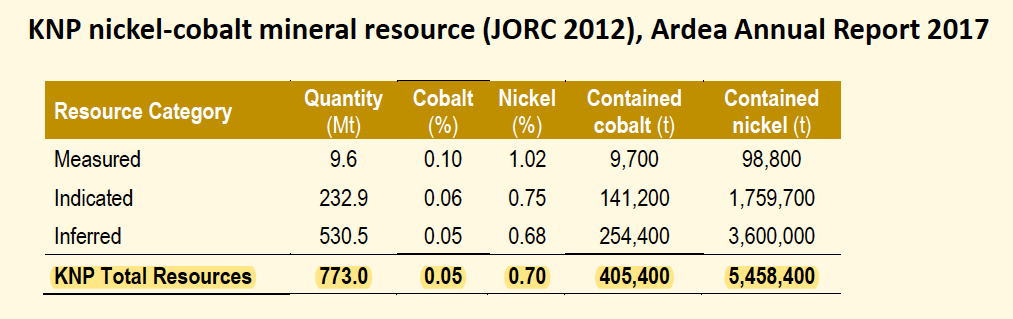

While vast and exceptionally large in overall size (total resource of KNP measures in at 773 Mt, which translates to an in-ground inventory containing 405,400 tonnes of cobalt and 5,458,400 tonnes of nickel), on the whole, the KNP is too low-grade (0.05% Co and 0.70% Ni) to be economical.

Therefore, in recent years, Ardea Resources has been keen on developing and re-scoping a smaller subset of the KNP, in hopes of isolating out the high-grade regions, which could support an economical mine plan.

In large part due to the surging cobalt price (and hype) in recent years, Ardea Resources was motivated to publish a pre-feasibility study (PFS) for the Goongarrie Nickel-Cobalt Project (GNCP), which is contained within the boundaries of the much larger KNP tenements.

Source: Ardea Resources March 2018 Pre-Feasibility Study

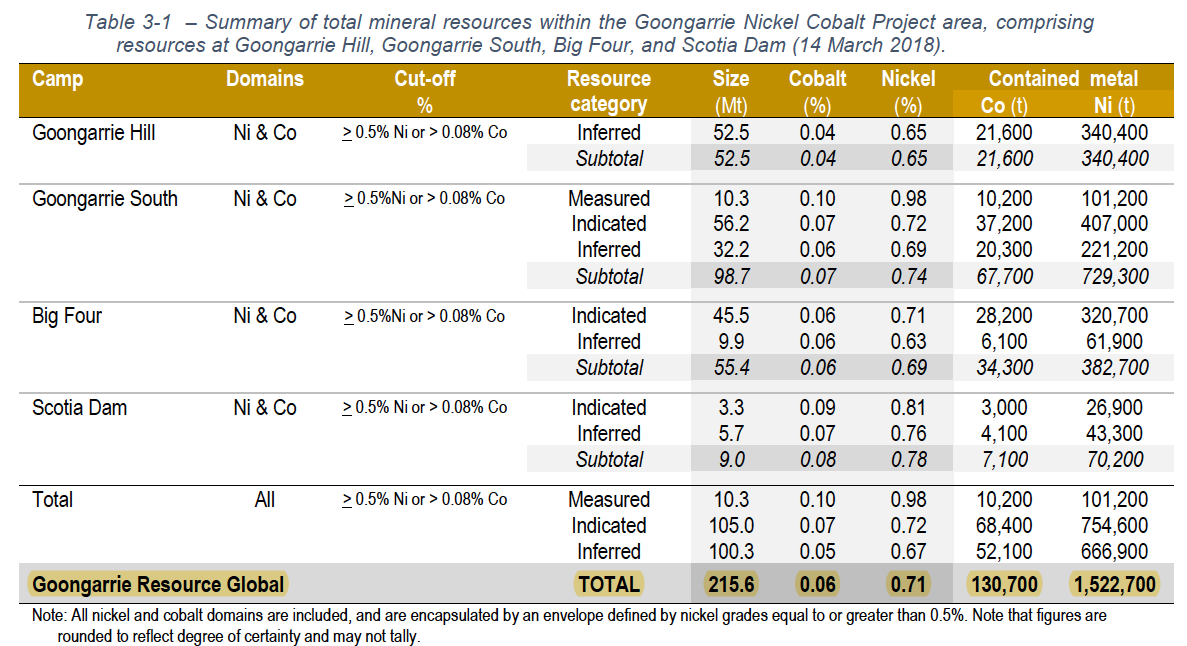

The following mineral resource estimate for the GNCP is shown below, which contains 215.6 Mt @ 0.06% Co and 0.71% Ni.

Source: Ardea Resources March 2018 Pre-Feasibility Study

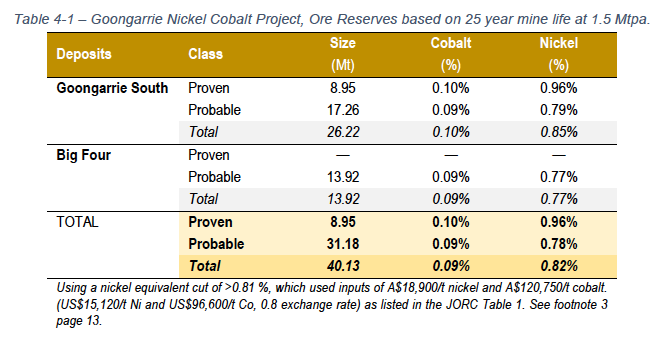

While optimization work has been ongoing, the results won't be known until after the in-progress definitive feasibility study (DFS) is later released to market.

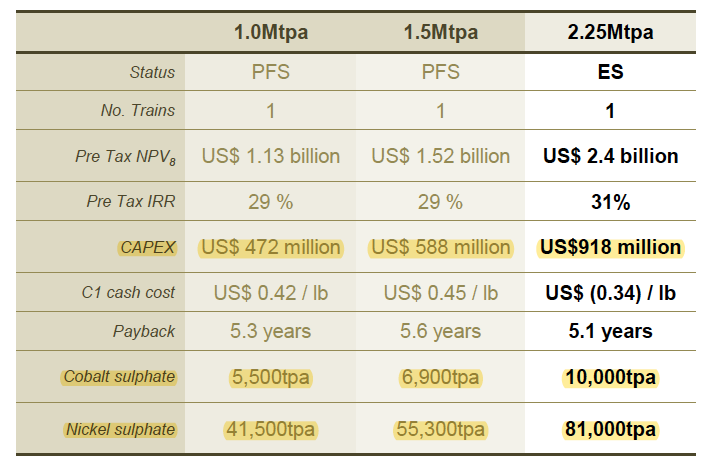

For now, Ardea Resources has 3 potential production scenarios outlined for the GNCP (the 1.0 and 1.5 Mtpa scenarios were defined in the PFS, while the 2.25 Mtpa scenario was published shortly after via an expansion study).

Source: Ardea Resources July 2019 Corporate Presentation

As shown in the table above, even though the GNCP was re-scoped in recent years to focus more on regions enriched with "high grade" cobalt, by and large, the bulk of any kind of production scenario would still be highly skewed in favor of nickel. Initial CAPEX is expected to range between $472 million and $918 million, utilizing a single autoclave processing train.

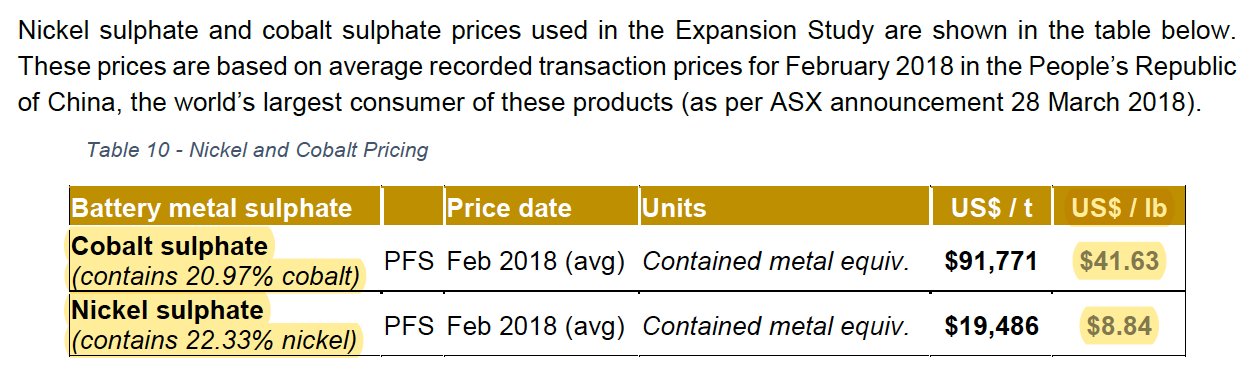

Also, it's worth noting that project economics for both the PFS (1.0 and 1.5 Mtpa scenarios) along with the expansion study (2.25 Mtpa) were produced using a base-case scenario that assumed a very high cobalt sulphate price of $41.63/lb and a more reasonable nickel sulphate price of $8.84lb.

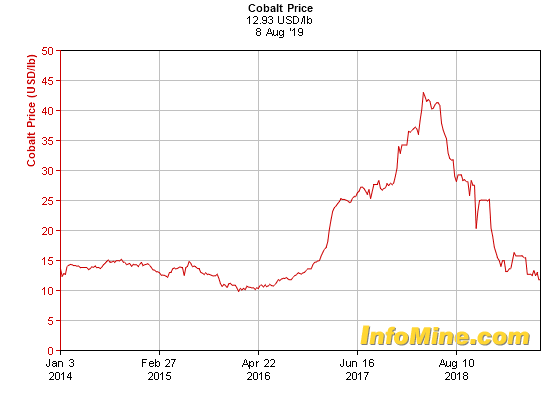

However, as the following chart will show, the cobalt price has been in free fall over the last year and is now trading at ~$13/lb, nowhere close to $40/lb.

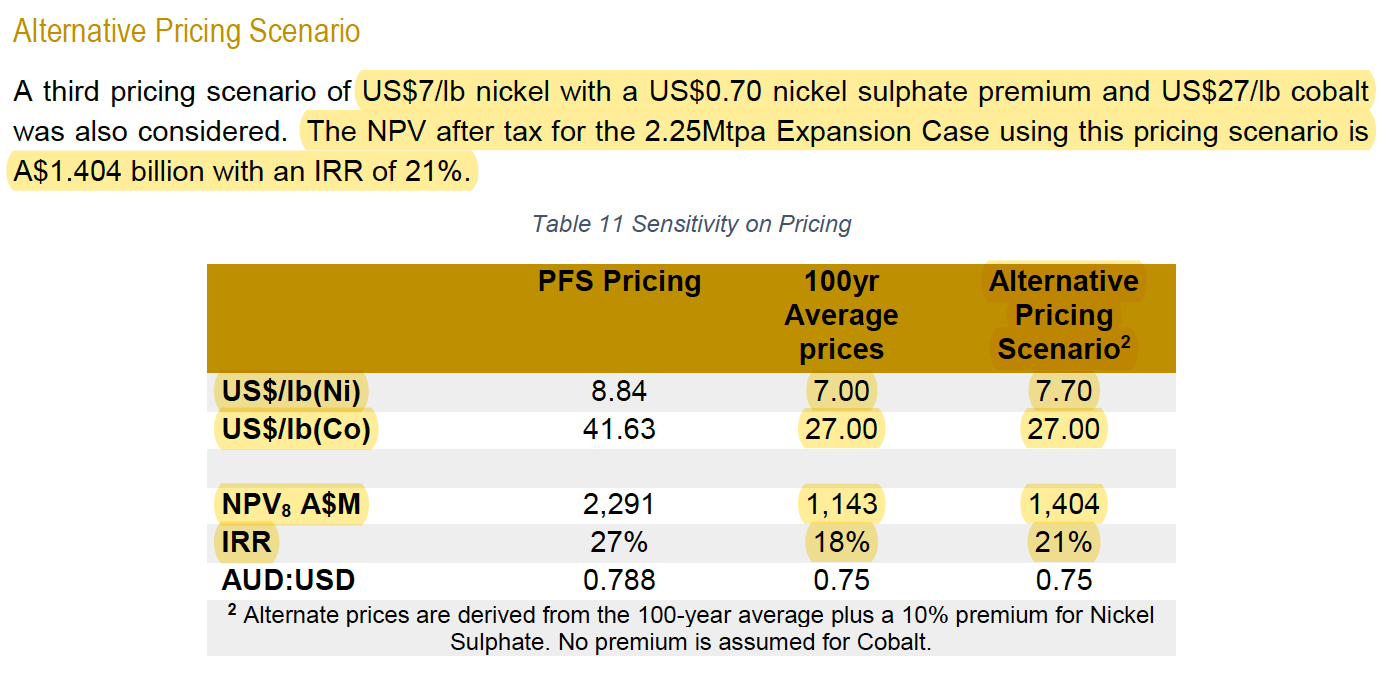

Fortunately, in the expansion study published for the 2.25 Mtpa production scenario, Ardea Resources did manage to include a section for both a 100-year average prices scenario, along with an additional alternative pricing scenario, both cases factoring in for the possibility of a much lower cobalt price (which would be more applicable to apply today since this is exactly the type of market environment we now find ourselves operating in).

Source: Ardea Resources July 2018 Expansion Study

In the 100 years average prices scenario, a nickel sulphate price of $7.00/lb is used, along with a cobalt price of $27/lb, which would produce an after-tax NPV (8% discount rate) of A$1.143 billion and an after-tax IRR of 18% for the GNCP.

Taking the same input prices above but adjusting for a nickel sulphate premium of $0.70/lb ($7/lb nickel + $0.70/lb sulphate premium) gives us the alternative pricing scenario, which would produce a slightly higher after-tax NPV (8% discount rate) of A$1.404 billion and an after-tax IRR of 21% for the GNCP.

Without question, the above-highlighted project economics for both "lower-priced" 2.25 Mtpa production scenarios clearly show that the GNCP is presently an "optionality play" at today's metal prices (~$7/lb nickel and ~$13/lb cobalt), but again, given the context of a fast-rising nickel price environment that could very well be getting underway now, it's conceivable that it may not take long before this project becomes a lot more viable.

The Search for a Strategic Partner

Further, if we look past the rather "mediocre" project economics (which would look even more dismal if a 10% discount rate was used) and focus more on the issue of security of supply, given the dearth of undeveloped high quality + large nickel sulphide deposits that exist worldwide, for certain end users, a project like GNCP may very well already be "good enough" to entice someone to lock in a Binding Offtake Agreement (BOA) and/or joint venture partnership, sooner rather than later.

Certainly, where things stand at the moment, the next major milestone that Ardea Resources will need to achieve in order to continue advancing the GNCP towards production is to secure BOAs/partnerships.

In June 2018, Ardea Resources appointed KPMG as its lead advisor tasked with trying to find a strategic partner to help finance the GNCP.

The following progress report was released back in April.

Further, the June Quarterly Activities Report provided an additional update on how the strategic partner search has been going so far, hinting that the recent move up in the nickel price has not gone unnoticed by third parties.

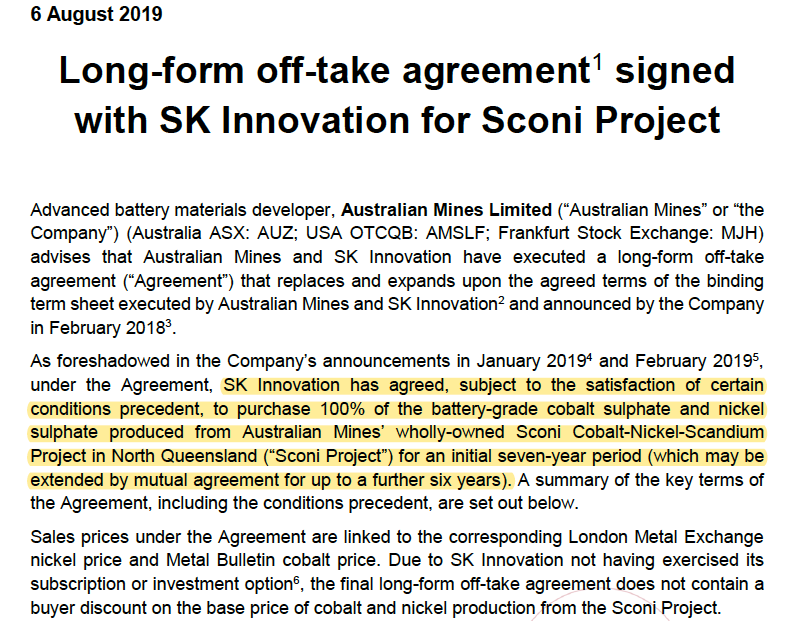

In the context of the broader market, it does appear that Australian Mines was just recently able to secure a long-form off-take agreement with SK Innovation.

Perhaps more deals will be around the bend in light of a recovering market for nickel?

For Ardea Resources, being able to reel in a legitimate strategic partner in the near future could do much to lift the share price of ARRRF out of the doldrums, which it has been residing over the past year or so.

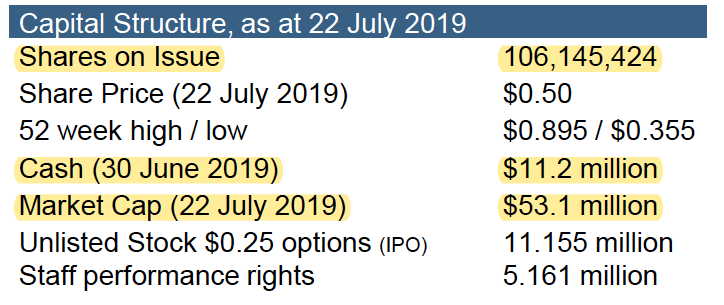

Share Structure and Cash Balance

Ardea Resources currently has ~106 million shares on issue, which for a later-stage development company is arguably a rather tight registry.

Further, the company currently has A$11.2 million of cash in the bank and zero debt.

Source: Ardea Resources July 2019 Corporate Presentation

Presumably, the company has enough working capital on hand to get through perhaps a few more quarters, but eventually, the company will need to raise a lot more capital, since again, the initial CAPEX estimate to put the GNCP into production is estimated to range between $472 million and $918 million. Looking back with the benefit of hindsight, management missed a wonderful opportunity to shore up the treasury when its script was a lot stronger, during the last bull market that took shares of ARL.AX up to ~A$2.00/share.

The End of the Cobalt Bear Market?

While Ardea Resources has always been more of a nickel "optionality play", the main culprit behind the rapid ascent experienced by shares of ARRRF in 2017-2018 was, in fact, likely due to cobalt, which again will be a byproduct produced by the GNCP.

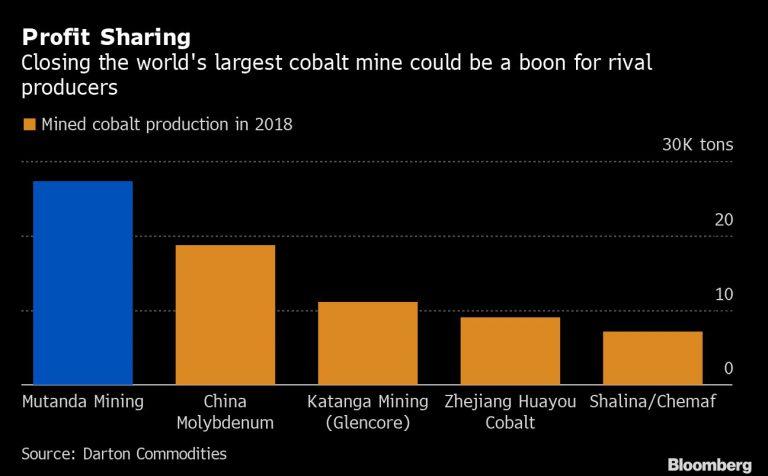

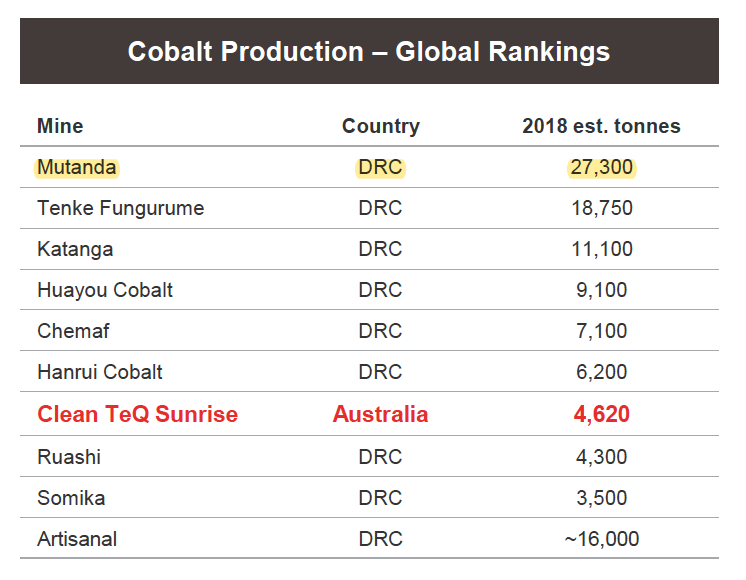

As mentioned earlier, although the price of cobalt has cratered over the last year and is now trading at just ~$13/lb, most recently, major producer Glencore (OTCPK:GLCNF) sent shockwaves across the industry when it announced plans to suspend production at its Mutanda Project, located in the Democratic Republic of Congo, by the end of the year.

We're not being OPEC. We've got an operation that wasn't making money at these levels," Glasenberg said. "You're not going to run an operation that's not making money."

For the broader cobalt sector, though, taking Mutanda offline could have huge ramifications, as the mine produced ~27,000 tonnes of cobalt in 2018, which is most significant when put into context that the total market supply is "only" ~135,000 tonnes.

Again, as mentioned earlier, the Expansion Study for the GNCP considered an alternative pricing scenario utilizing a "still too high" cobalt price of $27/lb (which is more than 2x the current price), so any type of catalyst that could put an end to the bear market in cobalt and start a trend reversal would be a huge win for helping to improve project economics.

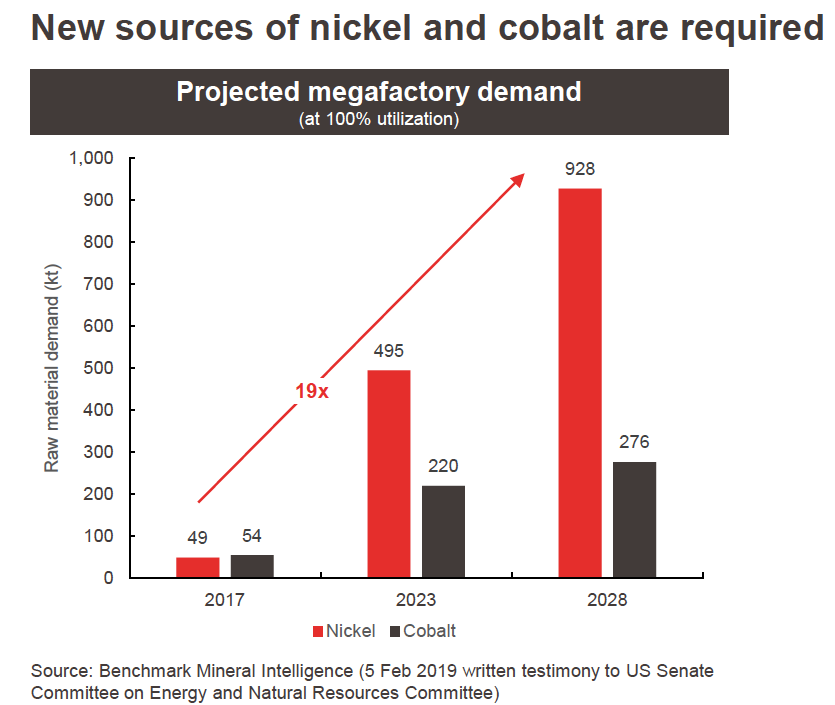

For Ardea Resources, an ideal perfect storm would be the combination of a full-fledged bull market taking place concurrently in both nickel and cobalt, which from the chart below, looks like it could happen at some point down the line (assuming the electric vehicle paradigm shift that many market analysts are predicting to happen does in fact).

Source: Clean TeQ June 2019 Corporate Presentation

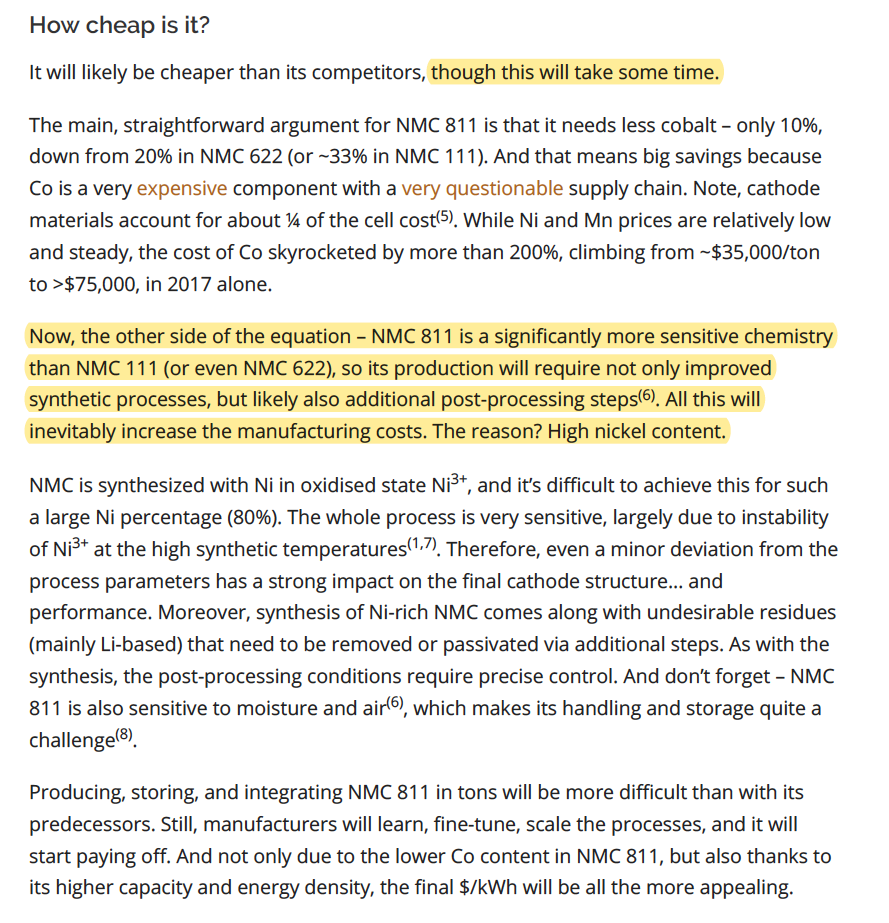

Yes, while there's also been a lot of talk in the battery industry in recent years about potentially reducing/eliminating cobalt content (due to its scarcity and volatility in pricing, which can at times make it a very expensive component), by transitioning to high-nickel cathode chemistries (e.g., NCA, NMC 622, NMC 811, etc.), in many cases, it's easier said than done in actuality.

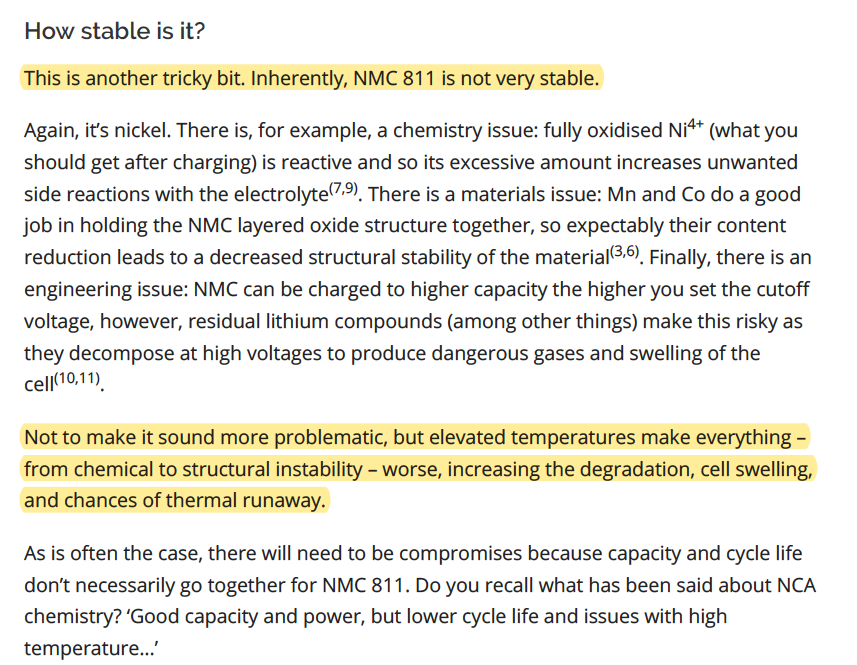

Then, there's also the matter of stability, which can become more of a safety hazard as increasingly more nickel is added (and less cobalt).

Source: Research Interfaces

In regards to any potential thermal runaway issues that could arise due to elevated temperatures when using high-nickel cathode formulas, mitigating against that very risk has historically been the calling card for even using cobalt in the first place.

More likely, the shift towards high-nickel content will still happen (technology will keep on advancing/improving), but it will progress gradually over the years as opposed to the "all or nothing" binary viewpoints shared by some market observers (who somehow believe it will be an overnight-type of sensation).

From Eric Norris, Albemarle's (ALB) President, Lithium, speaking in regards to 811 configuration, on the company's Q2 earnings call:

But I'll reiterate what I said three months ago, we never expected 811 to be a big player in EVs in the next couple of years. There are technology and processing challenges yet for that technology to be safely used in a large-scale format in a battery for an EV. It is being used experimentally in some - in China in some consumer goods products. It is being blended with a six to two to sort of, if you will, supplement the energy within that battery at a small level. But it is not - there are today, really no - we don't see any 811 full EV batteries for some time yet.

However, as Livent (LTHM) President and CEO Paul Graves shared during the company's most recent Q2 earnings call, there are data points to suggest that the shift to high-nickel content cathodes is, in fact, starting to pick up traction in the market.

We believe -- and again, data is not that easy to get ahold of, and so, we do our best with what's out there and with some of our own conversations with customers, but it feels to us that high-nickel chemistry in the first quarter and second quarter of 2019 -- and by that, I mean purely 811 and NCA -- in China, production perspective was about 10% of total production. Now, that's important to understand because total production of those cathodes was up 25% Q1 to Q2, so we're seeing the shift -- from relatively low percentages, we're seeing a shift in production of high-nickel cathode materials.

We're seeing those cathode materials first and foremost finding their way into non-EV applications, where maybe the safety environment feels a little different. We are seeing what I believe to be the dying growth story in LFP or NNC 111 and maybe even 532 chemistries. While they will continue to have large applications, whether it's in stationary storage or in certain non-passenger EV applications, it feels like the technology roadmap for passenger EVs is moving more quickly and more rapidly toward high-nickel chemistries. We're seeing 622 for sure grow more quickly than anything -- about 45% Q1 to Q2 based on the data we have. That's a meaningful shift.

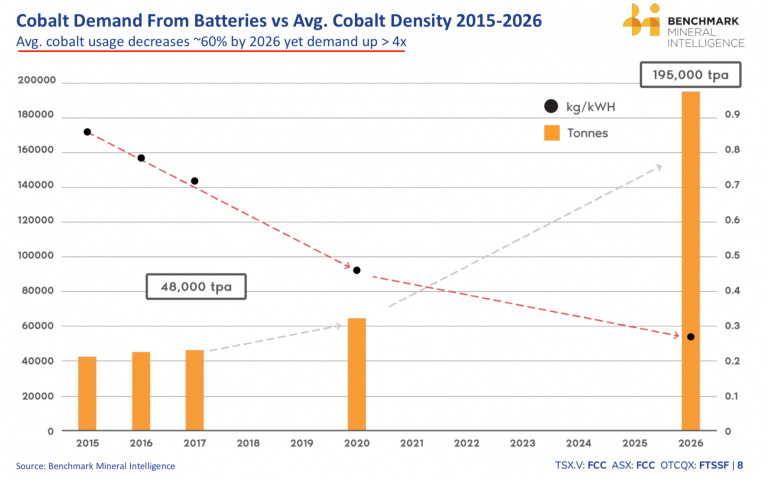

Even so, as the following chart illustrates, global demand for cobalt should still be robust over the foreseeable future.

Since a company like Ardea Resources has an asset like the GNCP that has massive inventories of both "critical" battery metals, nickel, and cobalt, it's hedged in either direction, irregardless of whether or not the shift to high-nickel cathode chemistries happens gradually (or otherwise).

Conclusion

It's been a brutal bear market for many nickel + cobalt laterite mining stocks over the past year and shares of ARRRF are down -50.84%. However, growing concerns that an Indonesian nickel export ban originally slated to commence in 2022 could be moved up has ignited a ferocious rally in the nickel price over the past few months.

Looking even further down the road, it also seems probable that demand for nickel will only accelerate from here (as electric vehicle adoption starts to pick up pace worldwide), which could be a strong catalyst for higher prices.

So, while the last year has no doubt been difficult for Ardea Resources to work through, brighter days could lie ahead, especially if the company can bring in a strategic partner to help finance the GNCP into production.

Furthermore, Glencore's decision to shut down operations at their Mutanda mine by year's end could be just the remedy needed to put an end to the brutal bear market in cobalt, which would be another boon for Ardea Resources.

Currently, shares of ARRRF represent an "optionality play" on two critical battery metals, nickel and cobalt, who could both be on the cusp of a turnaround story. As such, Ardea Resources' flagship GNCP might be able to offer speculators some massive leverage, due to the size + scale potential of this project.

Moving forward from here, for anyone interested in battery metals, Ardea Resources will be a company most worth following.

Disclosure: I am/we are long ALB. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

ARL Price at posting:

57.5¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)