Galaxy Resources: Bad News Will Be Punished In A Lithium Bear Market

Apr. 19, 2019 2:46 AM•GALXF Summary

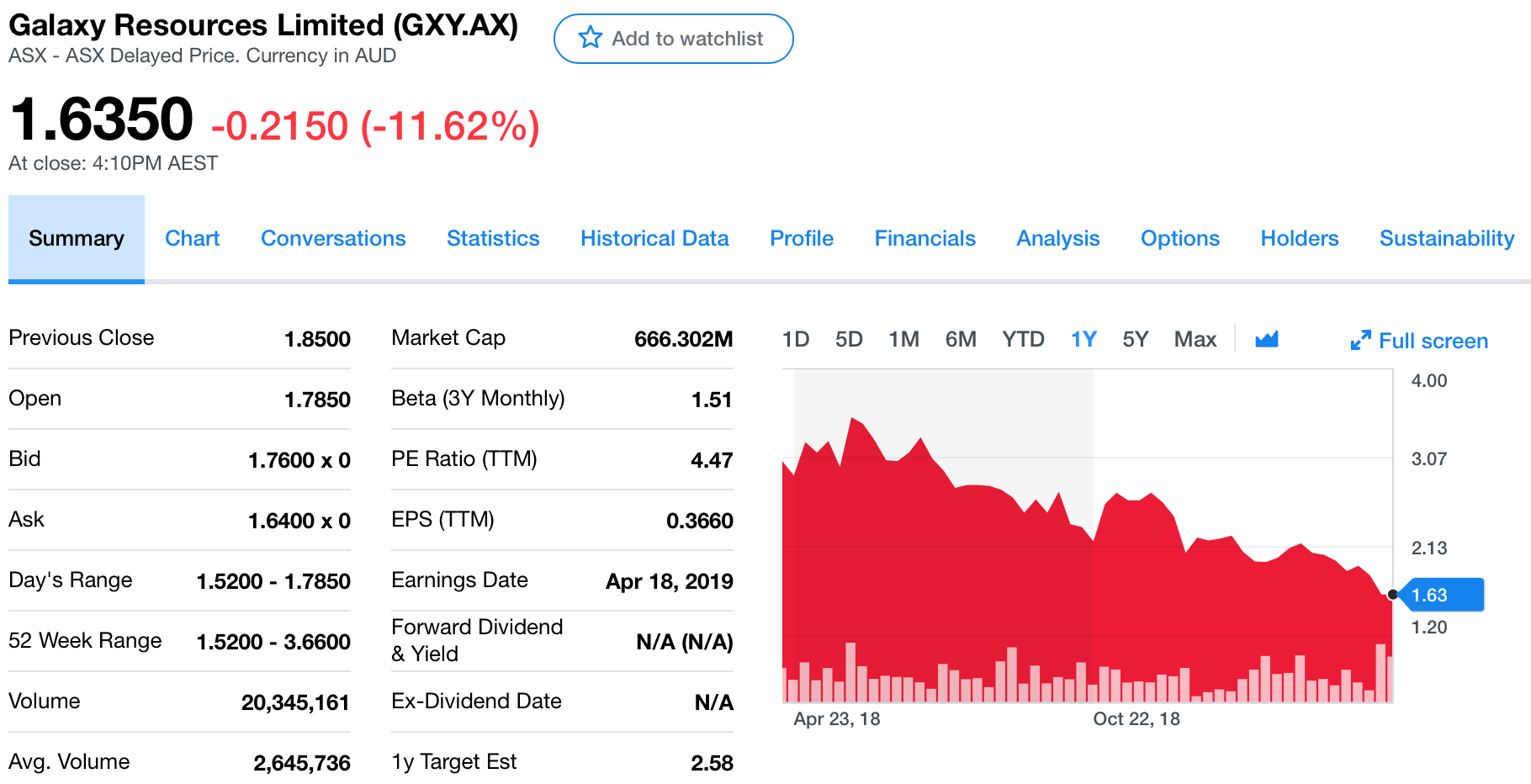

Shares of Galaxy Resources were smashed down Thursday, falling -11.62% after a series of bad news events hit the wire.

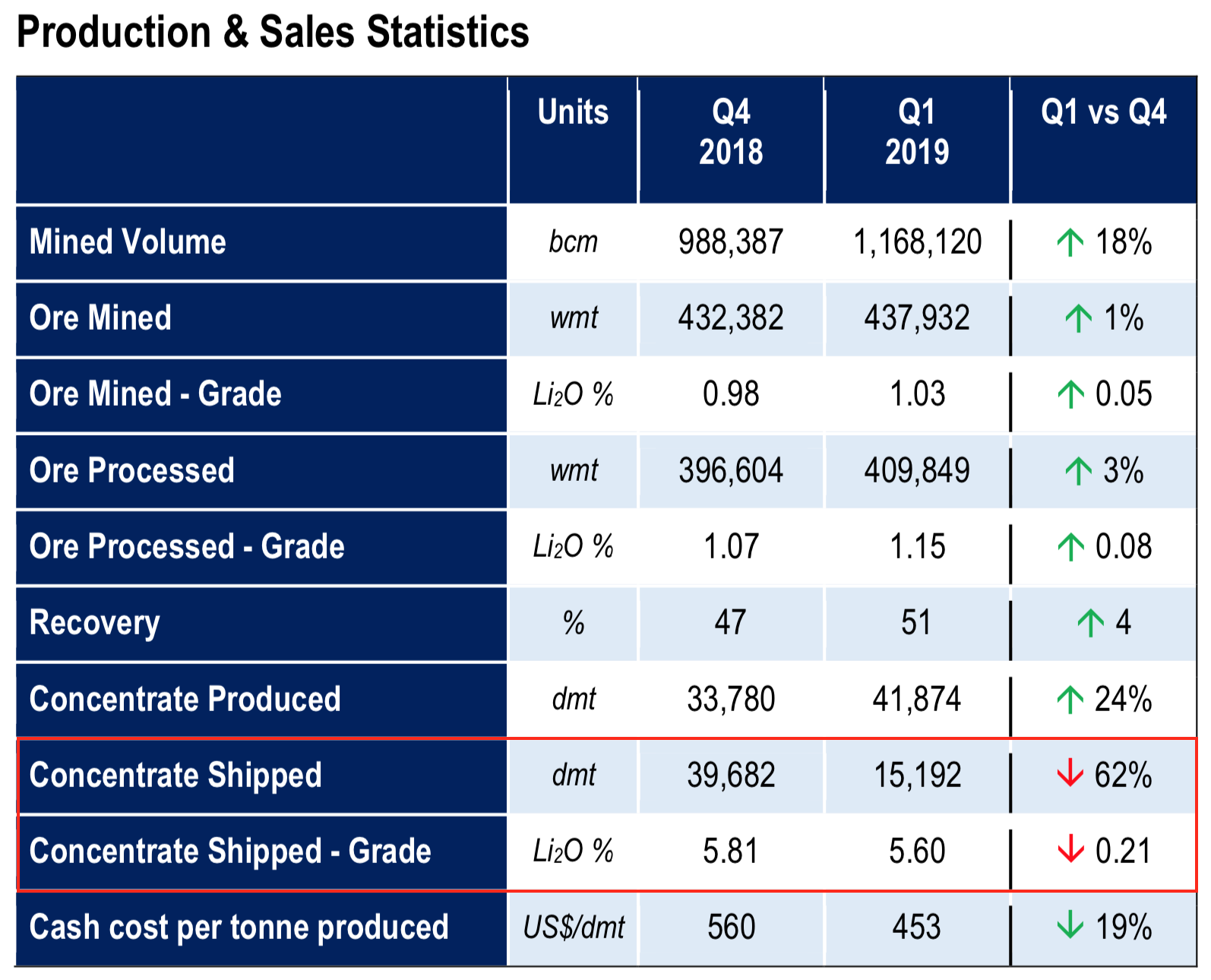

At Mt Cattlin, Q1 production numbers showed that recoveries only improved incrementally, despite the YOP being implemented, and more troubling, concentrate shipments fell by -62% while grade fell to 5.6%.

After ~1 year of negotiations, a joint venture deal could not be reached with third parties to help bring the company's flagship project, Sal de Vida, into production.

The company's balance sheet remains robust with $285.3 million in cash and zero debt.

For Galaxy shareholders, it's all about the long game now.

Shares of Galaxy Resources (GXY.AX/OTCPK:GALXF) closed Thursday's session down -11.62% on the heels of the company releasing a string of bad news. The already beaten-up and battered stock is now down a staggering -43% over the last year, with shares of GXY currently trading at A$1.635/share.

Because the broader lithium sector as a whole is operating in a bear market, there is little slack for mistakes right now and the prevailing mentality from traders at this time is to sell first and then ask questions later. In other words, patience is in short supply and the market really doesn't have any appetite to wait around for a turnaround story.

Mt Cattlin Q1 Production Numbers

First off, Galaxy Resources announced its Q1 production numbers from its sole operating lithium mine, Mt Cattlin, located in Western Australia, for the three months ending on March 31, 2019.

Although the amount of spodumene concentrate produced and ore grades increased from the previous quarter, not to mention cash cost per tonne produced declined by 19% (which are all improvements from the previous quarter), there were three items that stood out more than the rest:

Recovery was only 51%, up 4% from previous quarter.

Concentrate shipped was only 15,192 dry metric tonnes (dmt), falling -62% from the previous quarter.

Concentrate shipped - Grade was only 5.60%, falling -0.21% from the previous quarter.

Addressing each bullet point one by one, in regards to recoveries, even though Galaxy reported slight improvements at its Mt Cattlin operations, it's probably safe to say that the market was expecting larger strides to have been made by now, since the Q1 quarter was supposed to represent the one in which the Yield Optimization Project (YOP) was ready to start bearing fruit. As a refresher, the company invested capital into the YOP to primarily focus on three key upgrades, with the end goal being to profoundly increase recoveries (which at ~50% and below are arguably subpar to industry standards for hard rock lithium processing):

Ultra-fine dense medium separation (DMS) circuit.

Secondary floats re-liberation circuit.

Final product optical sorting

With the YOP, the primary issues that arose impacting performance in Q1 are as described by the company:

YOP average utilization of all circuits was below the forecasted 70% due to the bottlenecking of material through the re-liberation circuit and a sub-optimal distribution of the feed between the DMS and ultra-fine DMS circuits. Minor mechanical enhancements, including a larger pump on both the re-liberation circuit and ultra-fine DMS has rectified these issues with total utilization of the ultra-fines DMS circuit of 80% during the final three weeks of March.

The YOP was completed in Q4 2018 and the company previously reported that commissioning was 85% complete, prior to the start of Q1 2019. Targeted recoveries are 70%, which the market will now have to wait until the end of Q2 to see if Galaxy can achieve. So far, not so good, as the YOP has gotten off to a rather rocky start, experiencing hurdles that will need to be overcome.

Next, turning to concentrate shipped, the decline of -62% (down to just 15,192 dmt in Q1 vs. 39,682 dmt in Q4 2018) has to come as somewhat a surprise because it is not only significantly less than the amount of material shipped in the previous quarter, but also since it occurred during the same quarter in which the company actually managed to produce more concentrate (41,874 dmt in Q1 vs. 33,780 dmt in Q4 2018, up 24%).

This "outlier" in the amount of concentrate shipped, was also addressed by the company in the latest press release, with the following explanation being given:

The differential between production and sales volumes for the quarter was due to timing differences between Mt Cattlin production and the agreed delivery schedule between Galaxy and its customers during Q1 2019. This was a result of large volume shipments made to customers at the end of Q4 2018 to take advantage of higher sales prices resulting in our contracted customers having adequate inventory at the start of 2019. Galaxy’s customers have mainly weighted their required shipment volumes to the second half of 2019. Shipments are now being finalized for the June quarter and a more normalized shipping schedule is expected for the remainder of 2019.

Earlier, in February, Galaxy Resources did give a hint to the market to expect lower contract pricing in 2019 for its spodumene concentrate product being produced at Mt Cattlin:

Reduced margins in lithium chemical sales have resulted in a flowback reduction in the contracted price of spodumene for 1H 2019. Whilst contract prices are notably weaker than 2018, they have not reduced by the same percentage magnitude as the fall in Chinese lithium carbonate prices in 2018. Further, as a result of price volatility, Galaxy has adapted its price strategy for 2019 and has negotiated for a price reset during the course of 2019 rather than a 12 month fixed price.

So, although the explanation given by the company in its most recent Q1 Activities Report is consistent with the message relayed earlier in the year alerting the market to expect lower spodumene concentrate sales pricing in 2019 for its end products, the third bullet point (the fact that Galaxy was able to only produce/ship 5.60% grade spodumene concentrate in Q1) begs the retail speculator to play the role of devil's advocate and ask the (worst-case scenario) question:

Are customers rejecting Galaxy's concentrate because it's failing to meet the criteria for battery-grade spec?

Typically, when it comes to hard rock lithium mining and the processing of spodumene concentrate, the objective of companies looking to sell feedstock material for use in converter plants designed to produce battery grade lithium carbonate/hydroxide has been to aim for a grade of 6%. And although 6% isn't necessarily a binary cut-off point that must be met for finished material to be classified as "battery grade," there is no question that a higher grade spodumene concentrate will command a premium in sales price relative to that of a lower grade product.

Also, keep in mind, in recent years there has been an intense ramp-up in spodumene concentrate production, with so many new hard rock lithium mines coming online (with the majority of new mines emanating from Western Australia). Likely, there exists a plethora of high grade (6%) spodumene concentrate available out in the marketplace at this time, so there may currently be less of a willingness for customers to feel the need to have to "settle" for lower grade material (much less pay a premium for it) when 6% spodumene concentrate should be relatively easy to find (and cheaply too).

Let's not forget, in the backdrop of a bear market, lithium prices across the board (i.e. carbonate, hydroxide, spodumene concentrate) have been declining, and spodumene concentrate, in particular, has felt the pressure.

Spodumene producers “experienced more pressure as 2018 contracts expired, ushering in a difficult period of negotiation for suppliers, as Chinese converters sought to receive significant discounts due to increased supply” says Benchmark:

With negotiations still ongoing for the limited volumes available outside of offtake agreements, prices as low as $620/tonne have been reported in the market – however this has largely been for small quantities of off-spec material.

The majority of volumes are being traded at $700-750/tonne for 6% Li2O spodumene concentrate, although there could be some further decreases when Chinese buying activity resumes from mid-February onwards.

Further, although it's not an exact science (and can vary from customer to customer), there is unquestionably a certain threshold point that can't be breached before a batch of spodumene concentrate will be deemed "too low grade" to be suitable for use in the lithium-ion batteries market, and thus must be sold elsewhere (presumably for a lower price).

Now, is 5.60% still perfectly acceptable for Galaxy's end users?

That remains to be seen, but for Galaxy's sake (as well as shareholders), it would be best if the YOP can get on track quickly to help crank up the overall concentrate grades well north from current levels, so any lingering concerns about "too low grade for batteries" material being produced can be put to rest for good.

From the Q1 report, it appears that the company is at least heading in the right direction so far in the month of April:

With the Yield Optimization Circuits now operational, the final product grade has continued to improve in April, with an average grade of 5.9% achieved on production volumes assayed throughout the month-to-date.

Certainly, the "honeymoon phase" is now over for Galaxy Resources since the company is no longer one of the only hard rock lithium suppliers in town. As such, because Mt Cattlin shouldn't be confused with being a world-class tier 1 one hard rock lithium asset (it's not, and certainly not in the league of Talison's Greenbushes mine, by any stretch of the imagination), the realization must be that the days of this "mediocre" asset being able to generate ample amounts of free cash flow have likely closed for the foreseeable future.

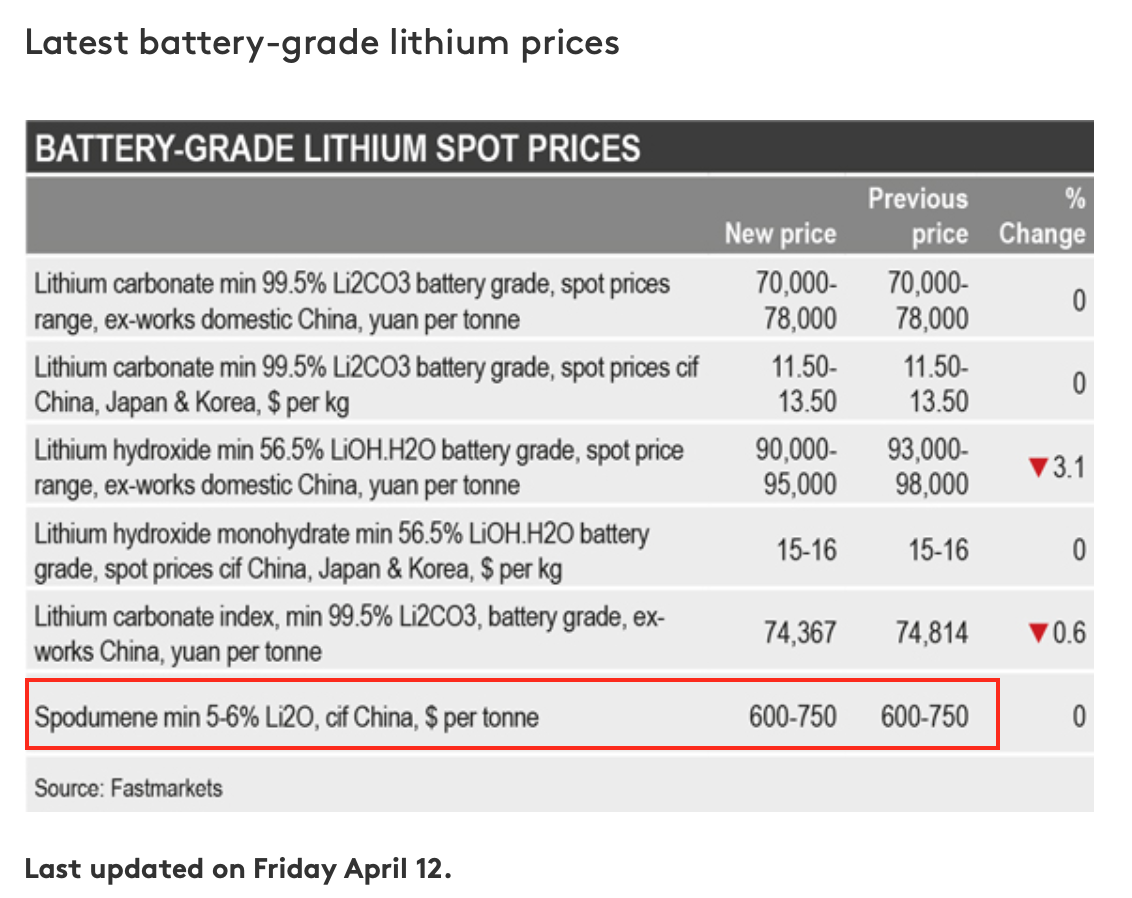

As quoted above and shown in the pricing slide below, current pricing for spodumene concentrate (ranging from 5-6% grades) is in the range of $600-750/t.

To my knowledge, Galaxy hasn't disclosed its contract pricing for 2019 publicly, but one can infer based on the above datapoints that profit margins have no doubt collapsed (relative to 2017-2018 peak pricing), and at this stage of the game, with cash costs for Q1 registering $453/t (which is still not low, despite improving from $560/t reported in Q4 2018) and the company unable to (yet) produce 6% grade spodumene concentrate, the market is likely looking further ahead down the road and anticipating Mt Cattlin being unable to generate much (if any) free cash flow moving forward from here. Therefore, it's feasible to assume that some of today's price decline in the share price of GXY.AX can be attributed to the market revising and lowering its future expectations for Mt Cattlin.

Sal de Vida Disappointment

With all that said, the biggest disappointment in Galaxy's string of news releases today has to be that after ~1 year of negotiations with various different parties, the company was unable to agree to terms on a joint venture deal to co-develop its flagship lithium (brine) project, Sal de Vida, located in Argentina.

As stated in the Q1 Activities Report:

Throughout the second half of 2018 and early 2019, Galaxy and JP Morgan conducted a comprehensive evaluation of strategic joint venture opportunities for Sal de Vida (“Sal de Vida process”.

To date, Galaxy has not been able to agree a transaction structure which provides what it believes is an appropriate valuation basis that properly reflects the world class nature of the Sal de Vida asset, particularly in the context of the successful POSCO transaction. Negotiations are ongoing with a shortlist of interested parties, however the Company has now resolved to formally close the Sal de Vida process.

In hindsight, Galaxy likely missed out on a "golden window of opportunity" to capitalize on a deal for Sal de Vida last year, and because the current landscape for lithium isn't the most conducive right now for sellers (in a low price environment, there's really no pressure on larger companies to have to overpay for assets), it's difficult to imagine how any terms being ironed out today could be more favorable than what might have been achieved when lithium prices (and mining stocks) were trading at record high territories.

As such, it is my own belief that the single largest contributor to the share price of GXY.AX falling by -11.62% today was due to Galaxy announcing to market that "the Company has now resolved to formally close the Sal de Vida process."

Likely, short-term traders/speculators holding onto shares of Galaxy awaiting for a Sal de Vida joint venture deal to be announced used Thursday's news to exit and close out their positions (no doubt, adding to the selling pressure).

For shareholders with a longer-term time horizon for holding shares of GXY.AX/GALXF, though, this could very well be a case of "short term pain for long term gain." Galaxy Resources is playing hardball, in a sense, holding out for a better deal to unlock shareholder value, and although the immediate consequence is perhaps a slower development path for putting Sal de Vida into production (since financing still needs to be raised to fully fund Stage 1 initial CAPEX and the company has to continue relying on its own in-house technical expertise in order to continue progressing the project along), the company gets to retain 100% ownership in a world-class tier 1 asset that should still have immense potential, capable of generating ample free cash flow once in production.

Therefore, if the path moving forward is to fly solo, the tricky part for Galaxy Resources will be in figuring out how to take Sal de Vida to the finish line without making catastrophic mistakes (the lithium chemicals business is notoriously challenging, which is probably the main reason why junior companies elect to bring in larger companies as joint venture partners in the first place).

The Bright Side

Nevertheless, on the bright side of things for Galaxy Resources, the company remains flush with cash (as I mentioned in my previous article), ending Q1 with $285.3 million (before accounting for the $67.3 million in taxes Galaxy may be responsible for paying, due in May 2019, as a consequence of the POSCO transaction) on the balance sheet, with zero debt.

So, although it's unfortunate that a most favorable deal involving Sal de Vida couldn't be reached at this time, Galaxy should still be commended for being able to execute a most favorable deal for itself with POSCO last May, selling non-core tenements for a handsome sum of $280 million (before taxes).

As such, Galaxy presumably has enough cash in the bank to fund a large portion, if not most of the initial CAPEX required to complete construction and bring Sal de Vida online, which is a most enviable position for any mining company aspiring to put a flagship project into production to find itself in.

In other words, unlike many of its lithium peers who are no doubt desperate at this time to secure whatever financing they can get to bring in the capital needed to advance their projects forward, Galaxy is not desperate for cash, so the company should still be well-positioned to make significant progress towards progressing Sal de Vida closer to production, while at the same time remaining patient, waiting for sentiment to return to favorable in the lithium space before committing to any deals with third parties for a joint venture.

Minimizing dilutive financings as much as possible is infinitely easier to do when you have lots of cash on the balance sheet and zero debt, which is the case for Galaxy Resources at this time.

Hyper-Growth In Lithium Demand Still Forecasted

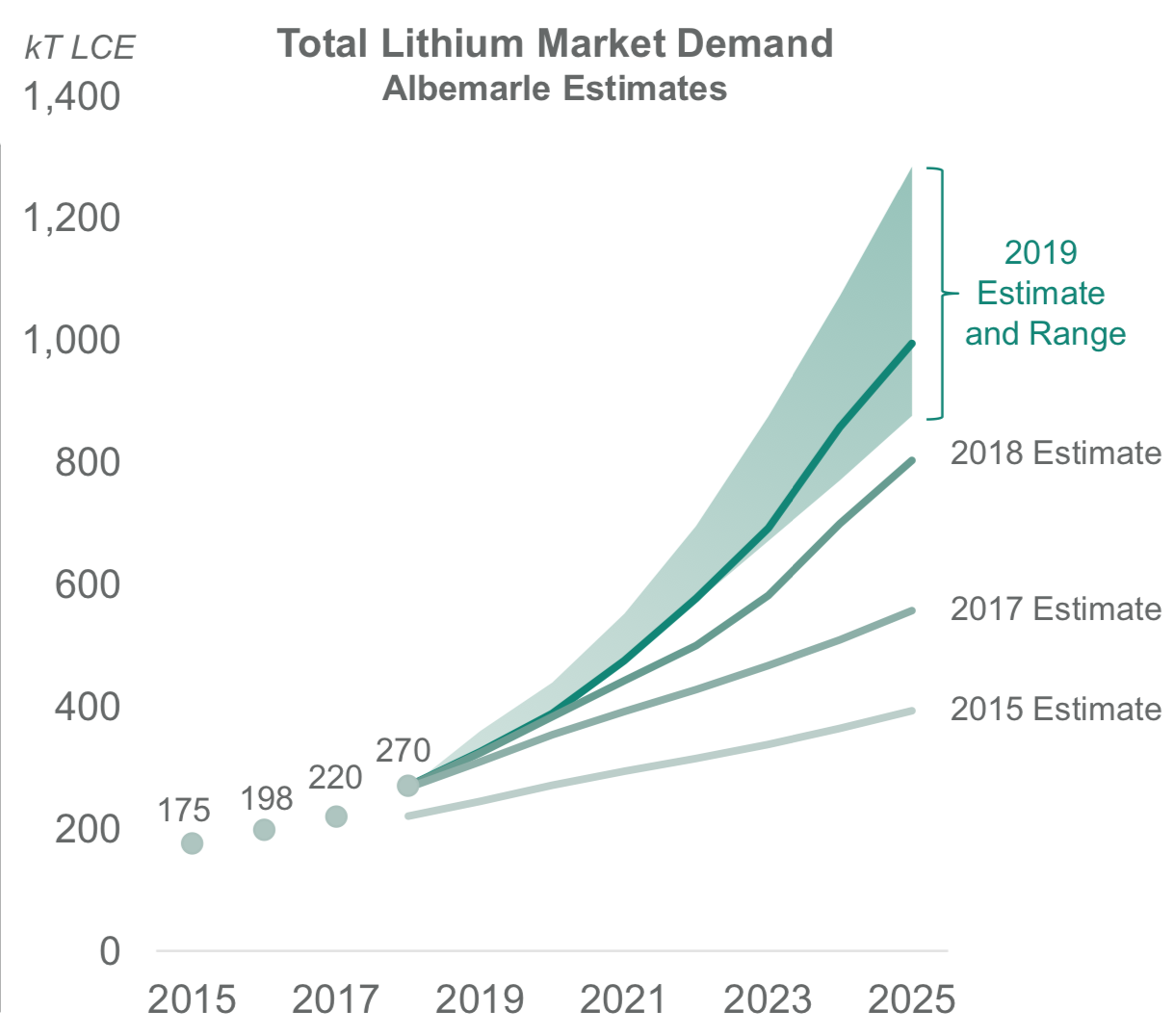

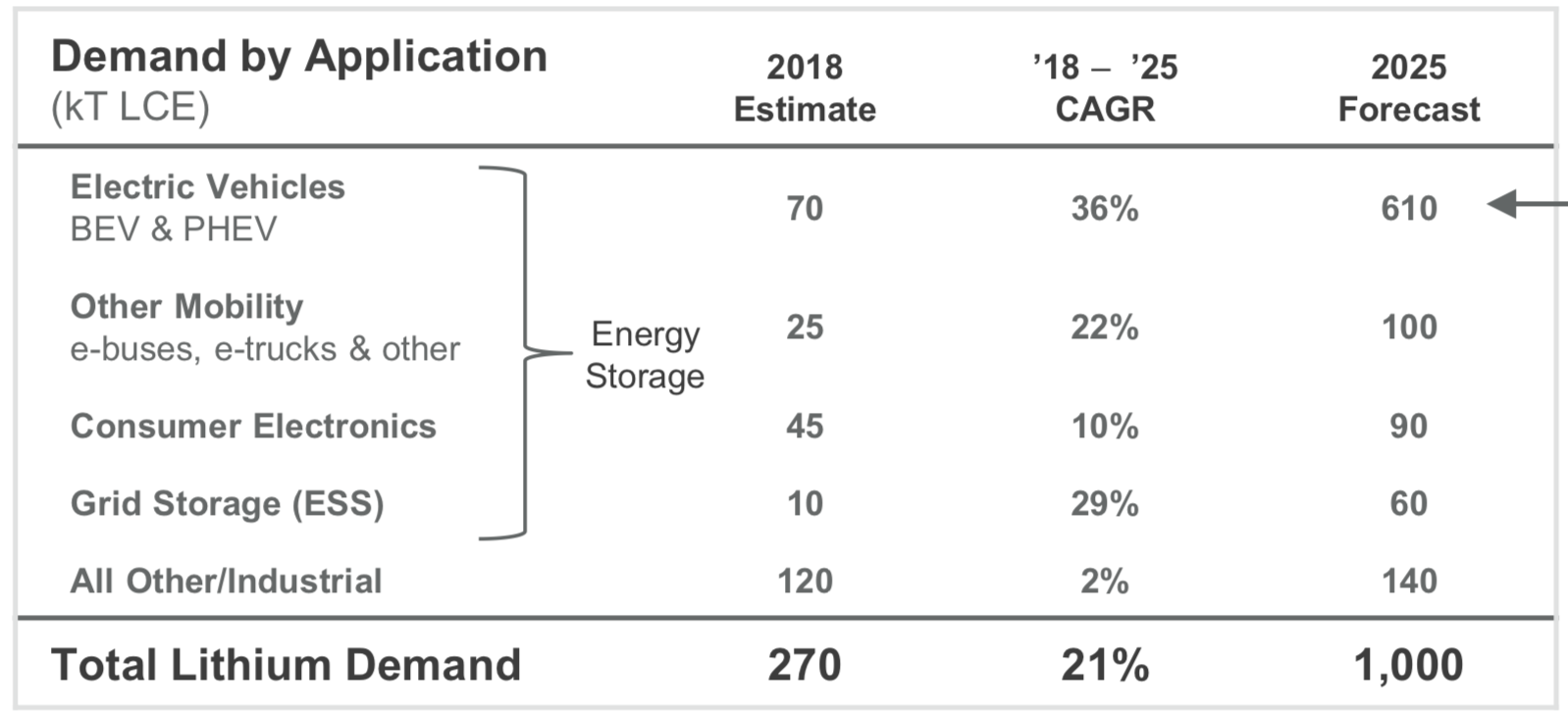

Furthermore, it's worth noting that it remains very early days in the hyper-growth story expected to materialize for both electric vehicles (EVs) and lithium, and many industry projections, such as the one recently put out by industry-leading lithium producer, Albemarle (ALB), are continually having to be revised to the upside, as market demand for lithium continues to accelerate.

The latest lithium market demand forecast from Albemarle is now registering 1,000 ktpa of Lithium Carbonate Equivalent (LCE) being needed by 2025 (total supply for 2018 was ~270kt).

Source: Albemarle February 2019 Corporate Presentation

Despite consensus at this time being that the lithium market is currently in a state of oversupply, the ever-changing nature that is inherent in a nascent sector still trying to establish itself (and by no means is anywhere near mature yet) means that the supply/demand dynamic could change drastically over the ensuing years, again, especially if new mines/expansion projects fail to come online quick enough to keep pace with the expected hyper-growth rate for lithium.

If, eventually, demand > supply (ala 2016-2018), the bear market in lithium could quickly reverse course, with prices rising again, and should that happen, a multi-asset lithium company, particularly one holding onto a world-class tier 1 deposit, like Galaxy Resources, should stand to do quite well.

Conclusion

The share price of GXY.AX tumbled down -11.62%, over a single trading session, after Galaxy Resources released its Q1 Activities Report; the downfall can be attributed primarily to suboptimal operations results at Mt Cattlin and the disappointing update on Sal de Vida announcing that to date the company has been unable to agree to terms with any third parties on a joint venture deal.

Clearly, the market was expecting more positive news from Galaxy Resources but it's important to remember that in the context of a bear market, companies more or less operate with very little slack. Mistakes tend to be more heavily scrutinized and when expectations are not met, intense market sell-off events can occur, which is precisely what was witnessed Thursday, as at one point, GXY.AX managed to set a new 52-week low, briefly touching A$1.52/share.

In contrast, bull markets are much more forgiving, and the ride up can be explosive, even for companies possessing no real solid fundamentals. However, more than half the battle is for a company to figure out a way to stay solvent throughout a bear market, so that it can later reap the rewards of an environment brimming with optimum.

As it pertains to Galaxy Resources, although the announcements released Thursday were obviously a letdown, there was by no means anything contained in the press releases that was bad enough to be considered a fatal showstopper. Certainly, there are issues at Mt Cattlin that need to be overcome, and it remains to be seen if this asset will be capable of generating free cash flow in a low price lithium environment, especially with the YOP yielding less than inspiring results, so far.

More importantly, though, management's decision to not rush into a deal to secure a joint venture for the company's flagship lithium asset, Sal de Vida, means that the team behind Galaxy has elected to focus on the long game. Fortunately for Galaxy Resources, the company has a robust balance sheet and can better afford to wait out this bear market than can be said for many of its peers in the lithium space. Time will tell if this bold move made by the company was the right one, but in the short term it has led to more pain for shareholders.

Disclosure: I am/we are long GALXF. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

GXY Price at posting:

$1.64 Sentiment: None Disclosure: Held

.