Tanim Asset Management would seem to agree with you..

"Given the timing of this acquisition and the strategic value RHP offers, we see a high likelihood of competing bids emerging from either an ASX listed company like Data3 (DTL.ASX) or another global player. The bid (with franking credit) is worth $2.56 but we think a price of $3.00+ is more reasonable. "

rhipe (RHP.ASX)

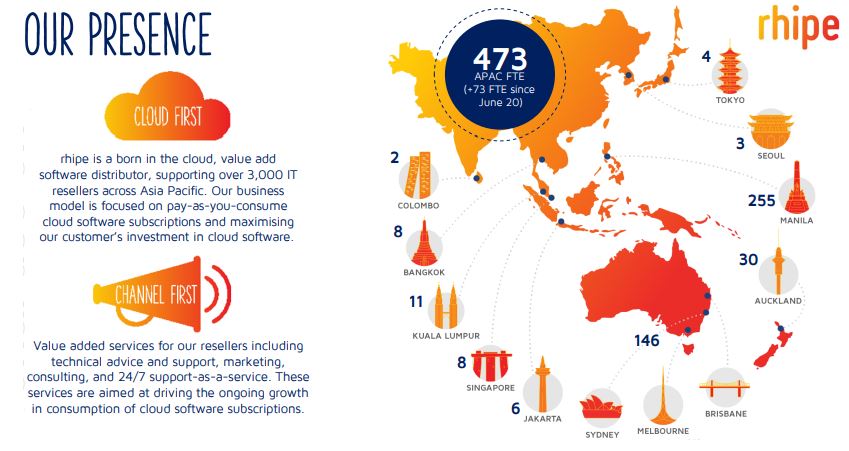

rhipe is a software reseller and is a strategic asset with 3,000+ resellers across ten countries in the APAC region. They predominantly sell Microsoft products (70% of sales) which provides other acquirers an opportunity to offer other vendor solutions - think Google, AWS, Symantec etc - to its product range.

Source: RHP 1H FY21 Results Presentation

RHP have been expanding in the APAC region, including a Japan JV in 2019, while also growing their portfolio of vendors to offer more solutions. Additionally, RHP have been focusing on building their own IP so they can offer their own software products as a standalone or in bundles with their resale products. Author: Ron Shamgar.

Returning to the takeover offer, the bidder, a company called Crayon (CRAYN.OL) - is listed in Stockholm and has a very similar business model to RHP in Europe. CRAYN has already raised the funds for the deal through a bond offering so they are fully funded and ready to go. The due diligence and the Scheme Implementation agreement took only three days to complete once the offer was announced.

CRAYN has made this bid for RHP at a cyclical low given their exposure to South East Asia which has been heavily affected by Covid. This impacted their share price; RHP was trading at around $2.40 pre-Covid and has traded roughly in the $1.50 - $2 range since. As touched upon above, RHP has been investing significantly in Japan and Korea of late. Japan is the largest Microsoft market outside of the US and the upside of the 2019 transaction is yet to impact earnings for RHP.

We estimate significant synergies (approximately $10m p.a.) for CRAYN from the acquisition. RHP is cashed up with $54m on the balance sheet and no debt. Based on FY22 forecasts, the RHP bid values it at 15.5x EV/EBITDA but with synergies the multiple is closer to 11x. Other recent software deals have seen multiples range from 18x for Hansen (HSN.ASX) to 49x for Altium (ALU.ASX).

Given the timing of this acquisition and the strategic value RHP offers, we see a high likelihood of competing bids emerging from either an ASX listed company like Data3 (DTL.ASX) or another global player. The bid (with franking credit) is worth $2.56 but we think a price of $3.00+ is more reasonable.

Watch this space.

Tanim Asset Management would seem to agree with you.. "Given the...

-

- There are more pages in this discussion • 14 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Add RHP (ASX) to my watchlist

Currently unlisted public company.

The Watchlist

LU7

LITHIUM UNIVERSE LIMITED

Alex Hanly, CEO

Alex Hanly

CEO

SPONSORED BY The Market Online