TIG Operating Update

TIG is pleased to update operating performance as of the end of August 2018 at Project F.

Coal mining and production

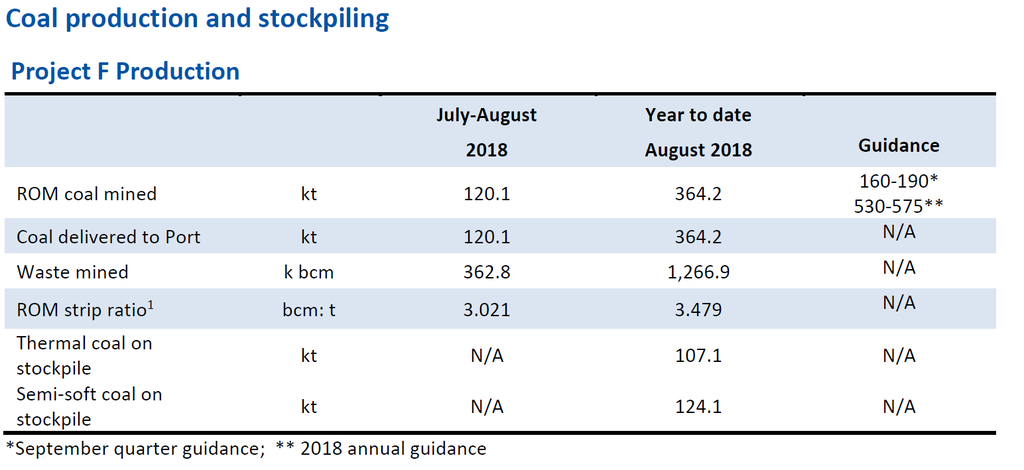

▪ Production for the months of July and August has been 120.1 thousand tonnes (“kt”of coal mined and delivered to our port at Beringovsky, bringing the year to date production to 364.2kt.

▪ As of 31 August, TIG has 231.2kt of coal on our port stockpiles.

Coal sales and shipments

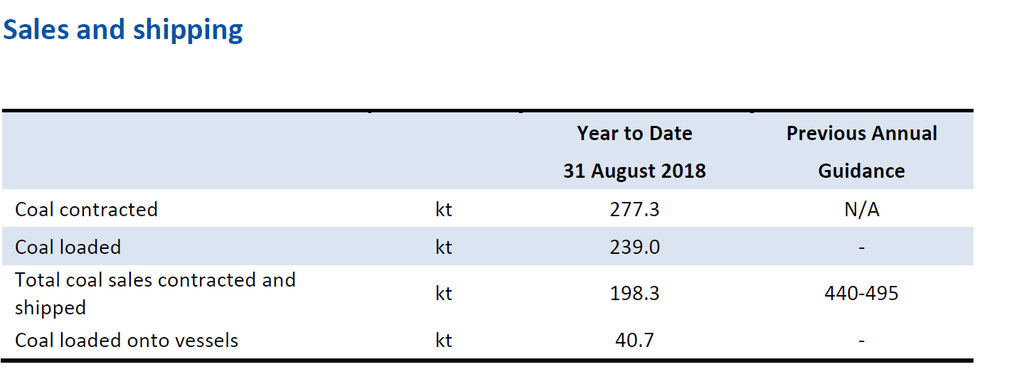

▪ Coal sales agreements in place as of 31 August total 277kt, of which 198kt is oxidized material for the thermal market and 79kt is semi-soft material for the steel sector.

▪ Coal shipped during the 2018 season to 31 August was 198.3kt with 40.7kt partially loaded onto vessels at the port.

▪ Our customer base has broadened further to include Japan, Korea, Taiwan, China, Cambodia and Vietnam.

TIG’s coal mining levels have increased through the summer months of July and August, as expected, and we are currently on track to achieve the previously reported guidance for the September quarter and for 2018. During July-August, we have mined 120.1kt in total, of which 34.4kt is thermal and 85.7kt semi-soft coals. At 31 August, of the 231.2kt of coal on stockpile at Beringovsky Port, 80kt is committed to complete existing sales contracts, with a further 90kt under negotiations on new contracts.

Production for the July-August period has been positively influenced by taking delivery of two additional Scania haulage trucks, an excavator and bulldozer at the end of June and TIG has taken delivery of a further two Scania haulage trucks at the Beringovsky Port on 4 September, which are expected to further enhance haulage capacity.

TIG Project F Pit operations summer 2018

Mining and haulage tonnages are in line with expectations and the majority of coal mined during the July and August months is sourced from the deeper benches in the pit. Coal qualities mined through to the end of the shipping season being expected to remain in line with that mined for the two months to 31 August.

TIG has reached the half way mark of our shipping season and, as of 31 August, TIG had executed six 2018 sales contracts for approximately 277kt of coal in total (123kt more than was reported in the June 2018 Quarterly Activities Report). Of this, 198kt is thermal and 79kt semi-soft coal sales. Our customer base has broadened further to include Japan, Korea, Taiwan, China, Cambodia and Vietnam.

Our coal products have been well received with coal quality testing of shipments achieving and exceeding client expectations. After a slow start influenced by unexpectedly adverse weather conditions in June, coal loaded to 31 August is 239kt. The results for the first half of the shipping season places us well to realise our sales tonnage targets, given the port stockpiles of 232.1kt in addition to expected September and October production of between 120kt to 140kt. We currently expect to end the season in line within the previous sales guidance range of between 440 and 495kt.

Beringovksy Port coal stockpiles: Summer 2018

Given the seasonal nature of our shipping season and the experience gained to date, there are a number of optimisation challenges remaining, including the execution of coal mining, haulage, sales and cargo loading practices and processes with our objective being the best seasonal outcomes in respect of both the tonnages and types of coal mined and sold.

We have invested in our value creation chain during the summer period by:

1. Adding an excavator and bulldozer to our mining operations;

2. Expanding our haulage capacity by acquiring, through finance lease arrangement, and commissioning into operations four additional Scania haulage trucks; and

3. Investigating opportunities to enhance our port stockpiling and vessel loading practices.

Beringovsky Port vessel loading operations: summer 2018

Coal Outlook

Prices in the metallurgical coal market in Asia have remained relatively strong during 2018 and although Premium low volatile hard coking coal (HCC) price declined from around US$250/t in early January to approximately US$184/t currently, market demand remains strong. In the previous TIG update it was noted that supply concerns had resurfaced in Australia due to rail issues in Queensland, which supported the HCC price over recent months and these concerns should continue to help provide a strong price outlook. This situation has not changed.

The Q3 2018 (July to September) SSCC quarterly pricing was agreed between Japanese steelmaker JFE Steel and certain Australian suppliers at US$137/t FOB Australia, which was effectively a roll-over of the Q2 settlement. In the last month, SSCC has come under some pressure, with the current spot price around US$121/t FOB Australia. It appears unlikely to soften further however, in fact it should be expected to rebound as high-quality thermal coal prices should provide a floor for SSCC at above the current SSCC price level.

Thermal prices have been strong this year. In January, the NEWC thermal coal index was at levels around US$110/t FOB basis 6000 kcal/kg NAR. Current NEWC pricing is around US$115/t – very little movement from the previous TIG update, however physical sales from Russia are pricing lower than the NEWC levels in competition for market share, with published FOB Vostochny prices currently around US$112/mt basis 6000 kcal/kg NAR, but deals are being done well below the published figure. The lower quality coal types (5500 kcal/kg NAR) are also heavily discounted, with 5500 NAR coal reportedly selling at less than $65/t FOB Australia today.

With most coal miners generating relatively strong profits at the current price levels, a supply response should be expected. Indonesian exports are now likely to be 25 million tonnes above previous estimates according to a report by the Indonesian Ministry of Energy and Mineral Resources on 16 August in which it revised its production target from 485 Mt to 510 Mt. Most forecasters expect prices to soften into 2019, and we are seeing some seasonal softness from China during the current quarter. However, there is little evidence of easing in market pricing for NEWC thermal or hard coking coal at present.

Add to My Watchlist

What is My Watchlist?

(20min delay) (20min delay)

|

|||||

|

Last

0.3¢ |

Change

0.000(0.00%) |

Mkt cap ! $39.20M | |||

| Open | High | Low | Value | Volume |

| 0.0¢ | 0.0¢ | 0.0¢ | $0 | 0 |

| TIG (ASX) Chart |

Day chart unavailable