Heath, thanks for your post.

NFA. GLTA

You say we are hell bent on pointing out incorrect flaws. Can you let me know what I have posted that is incorrect? More than happy to do further research and confirm and adjust my views.

Is it Almonty being 5 years late with Sangdong?

Is it Almonty still using costs from 2016?Is it Almonty not being the biggest western producer?

Is it Almonty not being “the last man standing” and only western supply when it comes to Tungsten production?

Is it Almonty not having “always made a profit from our mines”

Or was it something else? Let me know.Yes EQRs December quarter was not great.

Mt Carbine had to go into dry crushing then the processing plant had to shutdown for a few weeks due to lack of water. They only received 130mm of rain compared to the 800mm+ they received in the 2023 Dec quarter. They have however increased the Dam capacities and took the down time to implement water recycling upgrades on multiple parts of the plant. This should remove this risk going forward next Dec quarter.

They also used this time to focus on stripping to get to higher grade ore. Nothing out of the ordinary here. They will only have to move this large amount of dirt once. They are now hitting the higher grade ore and accordingly should have a good few years of higher grade access. Stripping costs money and returns no reward so that is also reflected in the quarter.Saloro the spanish operation has had many upgrades and changes to its processing over the last year plus. It is now generating cash and will continue to. The above issues were all Mt Carbine and was the reason the Dec quarter numbers were down so much. Mt Carbine might not be great this quarter but the next it should be doing very well.

Almonty paid for that report. Pop it in the bin. Why are you comparing Paid for reports with ASX financial reports?“Global EQR MRE is 41.7mt @ 0.23% WO3, over both projects, and that includes low grade stockpiles.” This is incorrect.

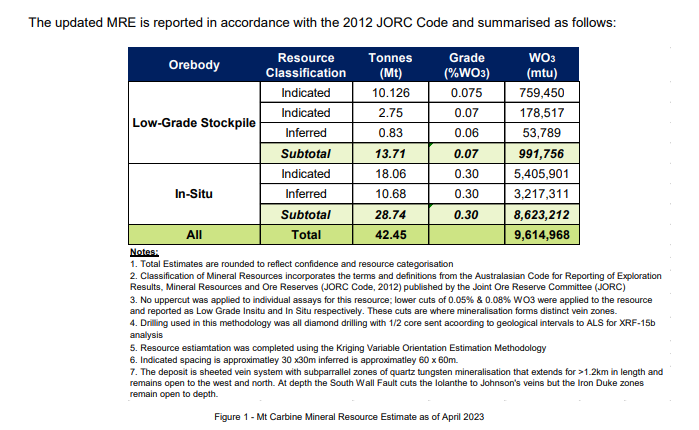

The diagram of resources you are posting for EQR is just the Open pit and Low grade stockpile at Mt Carbine. As Scott has said the open pit resource only includes a portion of the known ore body.

There is also the underground component. It includes a resource of 2.36mt @1.05% currently. See announcement on12th April 2022.

There is a lot more to be drilled out there.So yes the underground at Sangdong may be twice the grade of the open pit but it is less than half the grade of Mt Carbine underground. Also the reason why the open pit has quite a low grade is because unlike Sangdong it can be put through ore sorters to uplift the grade allowing a low cut off of 0.05%. As can be seen from the half yearly report:

“This rise in Sorter product is attributed to the newly commissioned ejection system at Tomra XRT Ore Sorter #2 (completed in mid-June 2024), and combined with a solid yield of over 10%, contributed to an increase of feed grade at the Gravity Plant from 0.438% WO3 for Q4 FY2024 to 0.545% WO3 for Q1 FY2025.” (yes it dropped in the dec quarter as they sourced mostly from the Low grade stock pile while stripping happened)

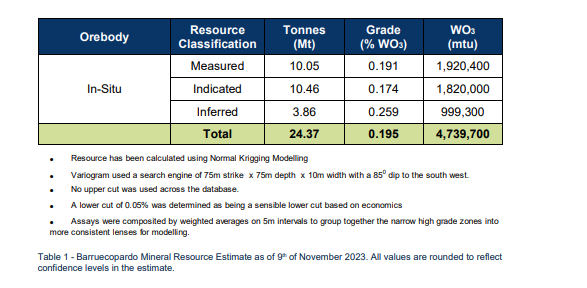

Even though the open pit grade is lower than the ore from Sangdong underground, once it has been sorted (low cost) it is then sent to the process plant at a higher grade(0.545%WO3) than the Sangdong ore. This grade will only increase as the high grade Mt Carbine ore is hit. Saloro is in the process of getting its 3rd XRT sorter and is also experiencing substantial uplift in ore grade for a low cost. The lift in grade is not as noticeable yet as they are processing previously discarded as waste ore due to its low grade and turning it into now economic ore. A huge plus for Saloro.As you only presented the Mt Carbine resource. Here is the Saloro MRE

EQR also has the Iron Duke resource, a resource of 5.8 million tonnes at an average grade of 0.59% tungsten WO3. It is adjacent to the current Open pit. Also a higher grade than Sangdong.

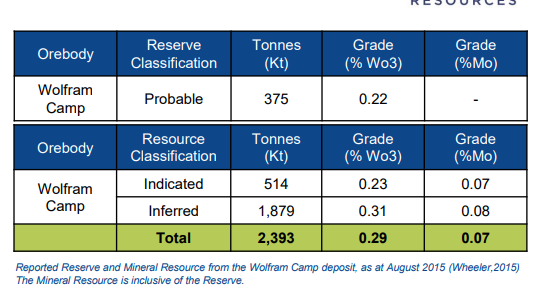

And of course EQR now has the wolfram camp resource. This is the resource Almonty purchased for $16m CAD then spent another $10m+ on it to only discarded it as an abandoned mine.

Both Mt Carbine and Saloro had 10 year mine plans as of 1st feb 2024. Both will be extended a long way past that. Also Mt carbines planned underground had a 10yr plan based on its current status. There will be a lot more drilling here. Both Mt Carbine and Saloro have many ore expansion prospects. These are not turning off any time soon.

I think you need to do a bit more research. I think it is fine to compare two tungsten mining companies. Perhaps our next comparison can be regarding current production?Did you see EQRs new announcement today? Strange that Almonty is the last man standing when EQR announces things like this. Surely someone should let Lewis know so he doesn't embarrass himself again and again.

2 years worth US $124m. This is not all of their production. They have other offtake agreements and like the announcement states.

They still plan on acquiring the largest western ferrotungsten smelter in Vietnam and feeding it with their concentrate.

Heath, thanks for your post. NFA. GLTAYou say we are hell bent...

Add to My Watchlist

What is My Watchlist?

(20min delay) (20min delay)

|

|||||

|

Last

$5.42 |

Change

0.070(1.31%) |

Mkt cap ! $62.65M | |||

| Open | High | Low | Value | Volume |

| $5.37 | $5.42 | $5.16 | $201.7K | 38.55K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 2 | 1300 | $5.30 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $5.70 | 155 | 1 |

View Market Depth

| Last trade - 16.10pm 30/07/2025 (20 minute delay) ? |

| AII (ASX) Chart |