Introduction

After London Mining and African Minerals went under and now Atlas Iron has suspended the production of iron ore at its Australian assets, a lot of eyes have turned on the iron ore sector and the speculation of what company might be the next one to shut down has started. Last month, I published an article wherein I stated Fortescue Metals would very likely survive the current crunch despite its sizeable debt position. The company's most recent update, however, indicates I might have been a little bit too conservative.

Fortescue's update

Fortescue shipped approximately 40 million tonnes of iron ore in the first quarter of CY 2015 (which is Q3 of the company's financial year). That's a little bit less than the previous quarter, but what attracted my interest was the company's C1 cash cost. Whereas Fortescue had a production cost of approximately $28.5/wmt in the previous quarter, it was able to reduce this by 9% to just $25.9/wmt in the last three months. The majority of this cost savings very likely has been caused by a cheaper Australian Dollar and I had already anticipated this in my original article.

However, the company's official cost guidance for 2016 was what really got me excited. Fortescue Metals thinks it will be able to continue to reduce the C1 cost of its iron ore towards $23-24 in the current quarter and a stunning $18/wmt in the next financial year. This cost reduction will be the result of continuous cost cutting measures of Fortescue after announcing a new labor agreement and consolidating several mining contractors at the Christmas Creek project. Additionally, the Salomon Hub will be supplied with natural gas which will further reduce the power costs.

What will the impact be on the company's financial performance?

Okay, it's good news, but let's now determine how good and important this news actually is. Fortunately Fortescue's IR department is doing a good job to calculate the all-in cost per tonne of iron ore.

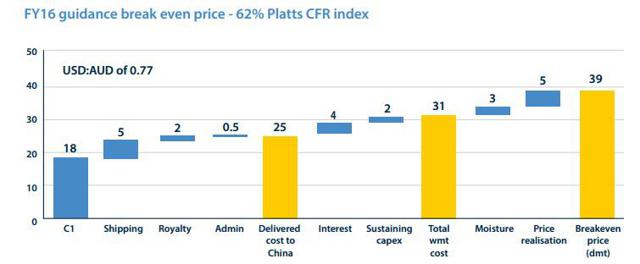

(click to enlarge) Source: press release

Source: press release

In my original article, I was assuming an AISC of $36/wmt. This has now been reconfirmed as the previous image shows an expected AISC of $39/dmt, which already includes the corrections for the moisture content and the grade which is lower than the benchmark grade. As the current benchmark price is approximately $49/dmt, Fortescue's operating margin will be roughly $10/t. At a production rate of 147 million dry metric tonnes per year, this results in an operating pre-tax cash flow of $1.47B per year, which is $120M per year higher than the result I came up with based on an iron ore price of $55/dmt.

So yes, this is an excellent achievement and if the iron ore price would indeed increase again to $55/dmt, Fortescue would be generating in excess of $2B in operating cash flow. But even at $49 iron ore, Fortescue remains profitable and should be able to reduce its net debt position of $7.4B even further.

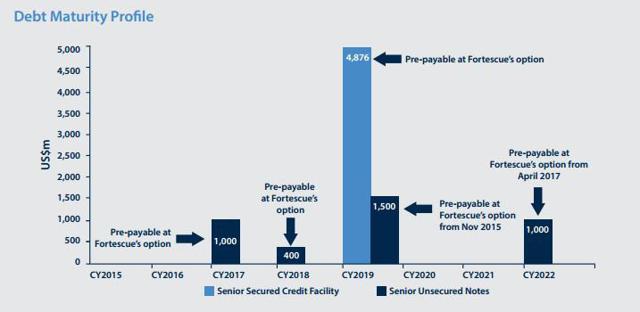

Source: press release

Source: press release

Only $1.4B of debt will have to be repaid within the next 3 years and this will easily be covered by Fortescue's update after-tax cash flows. However, the $6.4B due in FY 2019 will have to be refinanced but the company should be able to do so at a decent rate as it will have proven to the market it has been able to cut expenses to remain profitable. On top of that, I would expect the net debt position to be less than $5B by FY 2019 thus reducing the risk profile of the company.

Investment thesis

Fortescue's financial performance in financial year 2016 will be better than I anticipated despite the fact the iron ore price is trading 10% lower than when I wrote the previous article. I remain convinced Fortescue Metals will be one of the few iron ore producers left standing after the current crisis. The higher cost producers will be pushed out of the market whilst the larger producers that can benefit of economies of scale will be able to survive.

Despite its sizeable net debt position, Fortescue could be a good bet on a rebounding iron ore price as it will even remain profitable at the current market price.

seeking alpha

(20min delay)

(20min delay)