Tesla cannot manufacture high-energy lithium-ion batteries for EVs or stationary energy storage systems without plentiful supplies of cobalt, a strategic metal that’s essential in a wide variety of high-value products.

NCA cells for EVs typically need about 200 grams of refined cobalt per kWh of battery capacity and NMC cells for Powerwalls typically need about 425 grams per kWh.

Depending on product mix, Tesla’s gigafactory will require 7,000 to 15,750 tonnes of refined cobalt per year to manufacture 35 GWh of cells.

98% of the world’s ethical cobalt is produced as a byproduct of copper and nickel mining, which plays hell with normal supply and demand dynamics.

Cobalt demand growth is expected to outpace cobalt supply growth for the foreseeable future, setting the stage for persistent material shortages and far higher prices. Introductory notes

Over the last year, I've devoted a tremendous amount of time, effort and energy to studying cobalt mining, refining and processing, and learning about the cobalt sector's twists, turns and scary dark places. Those efforts gave rise to three earlier articles on Seeking Alpha.

This fourth article in the series assumes that readers are familiar with my earlier work and does not revisit issues that were adequately covered in those articles. Since this is a blog rather than a book, I can't discuss all issues and questions every time I sit down at the computer. If this article does not discuss an issue or question you consider important, please be patient because I'll get to it in due course.

While I generally agree with H.L. Mencken's observation that newspapers (and blogs) are "devices for making the ignorant more ignorant and the crazy crazier," they can be useful for diligent investors who want to understand both the facts and the unavoidable market dynamics that flow from those facts.

When I began writing about cobalt in March 2016, the LME price was $10.57/lb. On Wednesday, the LME price was $25.40/lb. and as near as I can tell the fat lady is just warming up. Since there is no "right price" for cobalt and demand will almost certainly outstrip supply by increasingly wide margins for the foreseeable future, a transitory price spike into triple digits wouldn't surprise me. Silly things are bound to happen in this Mexican standoff between inelastic cobalt supplies, soaring demand from the battery industry and inelastic demand from manufacturers of other high-value products. High-energy Batteries Need More Cobalt Than Lithium

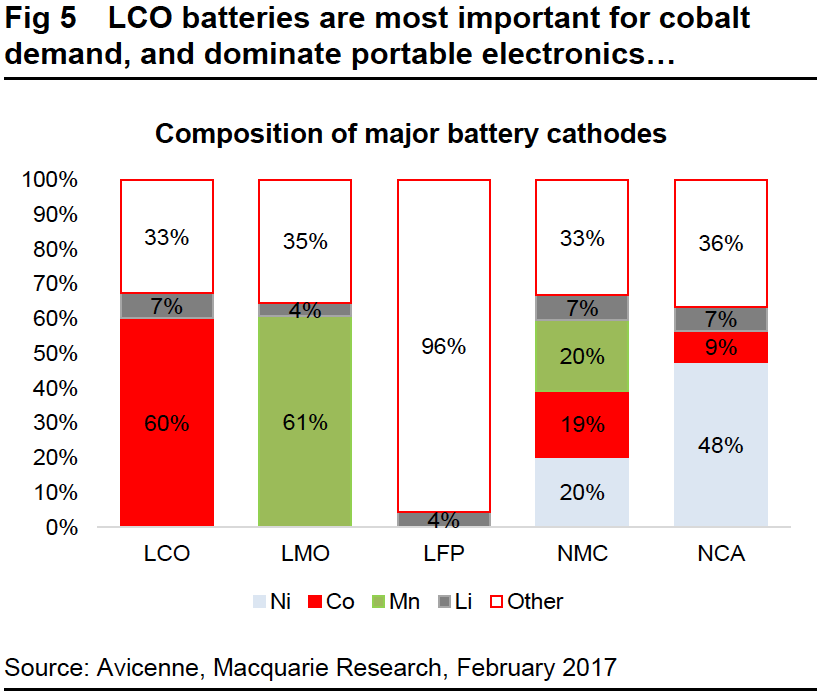

My first graph comes from a recent Macquarie Wealth Management Commodities Comment titled, " The 2017 battery metal story might well be cobalt." It shows the relative proportions of certain key metals in the cathodes of five generic lithium-ion battery chemistries. While lithium is essential in all five chemistries, the metal Goldman Sachs dubbed "the new gasoline" is only a small percentage of cathode weight and an almost insignificant percentage of cell weight. The important point is that high-energy chemistries invariably need more cobalt than lithium.

Depending on scrap rates at the cathode powder processing, cell fabrication and pack fabrication levels, NCA cells for EVs typically need about 200 grams of refined cobalt per kWh of battery capacity and NMC cells for Powerwalls need about 425 grams per kWh. In March of last year, cobalt costs in the bills of materials for NCA and NMC batteries were $4.65 and $9.88, respectively, per kWh. Yesterday those values were $11.18 and $23.75, respectively, per kWh. While rapidly escalating cobalt prices will increase battery costs, they probably won't be a deal breaker in the context of a $50,000 to $100,000 car. They will, however, squeeze manufacturing profits. More importantly, while price increases are survivable, difficulties in obtaining enough cobalt to keep the gigafactory running at capacity could range from harmful to catastrophic.

Historical Overview

Lithium cobalt oxide, or LCO, the original lithium-ion chemistry, was introduced in the mid-90s. A decade later, lithium manganese oxide, or LMO, and lithium iron phosphate, or LFP, were widely heralded as enabling battery chemistries for electric vehicles, or EVs, because their key raw materials were cheap, plentiful and readily available. The only perceived weakness in either chemistry was a relatively low specific energy (90 to 150 wh/kg) that would cap EV range at about 100 miles. Since the average American drives less than 35 miles a day, a limited range was not seen as a major design flaw and most early EVs used LFP or LMO chemistries in prismatic cells that were specifically developed for automotive applications.

Tesla (NASDAQ:TSLA) chose a different path. Instead of using LFP or LMO chemistries and automotive grade prismatic cells in small battery packs (24 kWh), Tesla saw clear advantages in using high-energy cobalt-based chemistries and commodity grade cylindrical cells in large battery packs (85 kWh).

The first advantage was low cost. The 18650 cell had been around since the mid-90s, production techniques and equipment were fully optimized, supply chains were robust, manufacturing facilities were largely depreciated and there was a large and growing capacity glut as electronics manufacturers abandoned cylindrical cells in favor of the prismatic cells required in thinner devices.

The second advantage was a radically different performance profile. By using the battery industry equivalent of a floppy disk and a cobalt-based chemistry, Tesla could build huge battery packs that:

Delivered immense instantaneous power for neck-snapping acceleration that would rarely be used;

Slowed battery degradation by keeping depth of discharge in the 10% to 15% range; and

Offered a theoretical travel range of up to 300 miles that would almost never be used.

The disadvantages of Tesla's strategy included reliance on less stable cobalt-based chemistries and greater supply chain risks. Tesla did a masterful job of engineering around safety issues and there have been fewer fires than many (including me) expected. Tesla's long-range muscle car pitch also resonated with its target demographic; wealthy buyers who prize flash and cool over environmental or economic substance. In response, several automakers including GM, Nissan, Ford and BYD that originally used small battery packs and LMO or LFP chemistries for their products are now migrating to large battery packs and cobalt-based chemistries for new products.

Historically, Tesla bought finished battery cells from Panasonic (OTCPKCRFF) which in turn bought processed cathode powders from Sumitomo Metal Mining (OTCPK:SMMYY); a Japanese company that owns a cobalt mine in the Philippines and processes its cobalt into cathode powders for battery manufacturers. To the best of my knowledge, Sumitomo's mine and refining facilities are already operating at capacity and there are no disclosed plans to triple or quintuple Sumitomo's cobalt production and processing capacity to accommodate new demand from Tesla's gigafactory.

Since inception, Tesla has been an indirect beneficiary of a secure supply chain that can support of tens of thousands of EVs per year. That supply chain was built by Panasonic and supports Panasonic's Japanese battery manufacturing operations. That supply chain is a Panasonic asset, not a Tesla asset, and unless Panasonic decides to abandon battery manufacturing in Japan, its supply chain can't be transferred to Tesla. Most importantly, Panasonic's existing supply chain isn't anywhere near enough to support Tesla's gigafactory.

When Tesla was the only automaker that used a cobalt-based chemistry, its production volumes were low and the Model 3 was little more than a PR talking point, cobalt availability was not a big issue. Now that Tesla is building a gigafactory in Nevada, several comparable factories are being built or planned to serve Europe and Asia, and most of these new factories plan to use cobalt-based chemistries, cobalt supplies are a major issue that may become the biggest "Oops!" in the history of supply chain management. Cobalt is a Minor Metal and a Byproduct

While cobalt is listed on the LME, it is properly classified as a "minor metal" because annual production is tiny compared to base metals and 98% of ethical cobalt supplies are a byproduct of nickel and copper mining. While a few cobalt-rich nickel and copper mines can produce up to a pound of cobalt for every 10 pounds of primary metal, most nickel and copper mines produce no cobalt. To put global supply statistics into perspective, in 2016, the world's miners produced:

19,400,000 tonnes, or 19,400 KT, of copper and 63 KT of cobalt from copper mines;

2,250 KT of nickel and 30 KT of cobalt from nickel mines; and

2 KT of cobalt from Bou-Azzer in Morocco, the world's only primary cobalt mine.

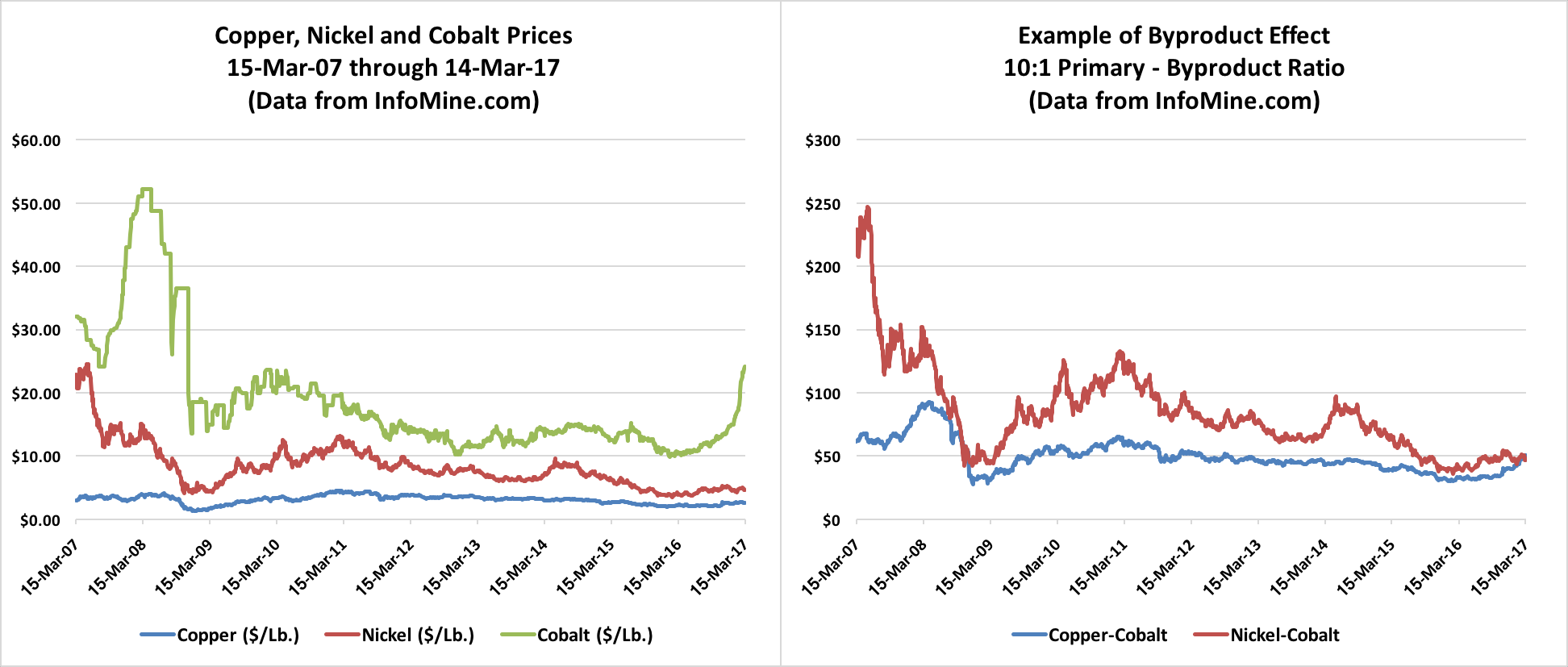

The biggest issue with byproduct metals like cobalt is that they don't exhibit normal supply and demand behavior. I've prepared a couple graphs to try and show you why.

The graph on the left uses daily price data that I got from InfoMine.com and shows the 10-year price histories for copper, nickel and cobalt. You can see at a glance that the post-crash period has not been kind to copper and nickel miners. In fact, the only bright spot for several years has been cobalt, which surged from $10.50 to $25.40 in the last year. The graph on the right shows the overall impact of the cobalt price surge on the total revenue of copper and nickel miners that produce one pound of cobalt for every ten pounds of their primary metal.

There is a modest revenue benefit, but it's nothing to write home to mother about and it doesn't even come close to justifying enormous new investments to develop mines to service expected battery industry demand that may not develop at all, or may develop more slowly than expected. Since mine development and major expansions frequently involve billion dollar investments and a decade of permitting, development, engineering and construction, projects that aren't already under way won't have any impact on the cobalt supply landscape for the foreseeable future. Likely Changes in Cobalt Production

Cobalt is an odd commodity because 25% of the metal contained in produced ores is never fully refined. There's a yield loss of about 10% at the refinery level and another 15% ends up in low cobalt alloys. So, when discussing cobalt supply and demand, it's critical to remember the 25% shrinkage between mine mouth and refinery gate.

In its 2016-2017 Cobalt Market Review, Darton Commodities Limited reported that total mine mouth cobalt production was 120.4 KT in 2016 refined cobalt production was 93.5 KT. Of that total, over half (47.2 KT) was used in battery manufacturing and the balance went into a variety of high-value products including super-alloys, hardened tools and materials, pigments, catalysts and magnets.

Darton also reported that the global cobalt supply and demand balance shifted from surplus to deficit in 2016. Looking forward, Darton predicted that the cobalt supply deficit was likely to widen, driven primarily by soaring demand from the battery industry. It then observed that rapid expected growth in the EV sector could drive battery industry demand-to 89.1 KT by 2022. Darton ultimately concluded that a battery industry demand ramp from 47.2 KT in 2016 to 89.1 KT in 2022 "could seriously challenge the cobalt supply chain."

It was a genteel British way of saying "when pigs fly!"

Over the next few years, five significant cobalt projects are expected to come online, including:

The planned 2018 recommissioning of Glencore's (OTCPK:GLCNF) Katanga Mine (OTCPK:KATFF) with a capacity of 22 KTPY;

The planned 2019 commissioning of Eurasian Resources' Metalkol RTR project with a Phase I capacity of 14 KTPY and an eventual Phase II capacity of 21 KTPY;

The possible 2020 commissioning of eCobalt's (OTCQB:ECSIF) Idaho mine with a capacity of 1.5 KTPY;

The possible 2020 commissioning of Fortune Minerals' (FMTDF) Mine in the Northwest Territories with a capacity of 1.6 KTPY; and

The possible 2021 commissioning of Clean TeQ Holdings' (ASK: CLQ) Syerston mine in Australia with a capacity of 3.2 KTPY.

Collectively, these projects have the potential to increase the embodied cobalt content of mined ores to 165.3 KT per year over the next five years, but only if:

eCobalt, Fortune Minerals and Clean TeQ Holdings can arrange suitable financing to pay their development, construction, commissioning and working capital costs;

All five projects are successfully completed on schedule and within budget; and

All five projects are commissioned without problems and prove capable of producing at or near their design capacities.

If the embodied cobalt content of mined ores actually ramps to 165.3 KTPY, the refined cobalt available to users will be roughly 124 KTPY. After deducting 45 KTPY of cobalt that's used to manufacture other high value products, the maximum supply available to battery manufacturers will be about 79 KTPY, or roughly 10 KTPY less than forecast 2022 battery industry demand.

While the five projects discussed above will increase cobalt supplies significantly in the short-term, I've not seen any discussions of other substantial cobalt projects that can sustain, much less increase, cobalt production in the medium- to long-term. Investment conclusions

Without sustained growth in cobalt production, there can be no sustained growth in high-energy lithium-ion battery production.

Without sustained growth in high-energy lithium-ion battery production, there can be no sustained growth in EVs and stationary energy storage system production and both technologies will be capped at levels that aren't even close to relevant until somebody develops an alternative battery technology that doesn't need cobalt.

The unlimited growth potential story that's driven Tesla's stock to nosebleed levels is, quite simply, a myth. The world can't produce enough cobalt to support worldwide production of more than a few million EVs per year. When you start factoring the likely growth of stationary energy storage into the equation, potential EV production rates plummet.

When I was in kindergarten we made festive holiday chains from construction paper. It appears Tesla used equally durable techniques when building a supply chain for the gigafactory.

To paraphrase Psalm 118, The [metal] the builders rejected has become the cornerstone. Without a clear solution to its cobalt supply challenges, Tesla's cobalt dependent business model will struggle mightily as the global cobalt supply and demand imbalance worsens. Fun with photographs

I took this picture in Houston, Texas on February 22nd using my trusty iPhone. The car is clearly a Tesla but it has a lower roofline than a Model S and a nose that resembles the Model X except for the proportions and the air dam at the bottom. My impression when I took the picture was that I'd spotted a Model 3 beta in the wild but I didn't bother to take a closer look.

Let the speculation begin. Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

BMT Price at posting:

20.5¢ Sentiment: Buy Disclosure: Held

CRFF) which in turn bought processed cathode powders from Sumitomo Metal Mining (OTCPK:SMMYY); a Japanese company that owns a cobalt mine in the Philippines and processes its cobalt into cathode powders for battery manufacturers. To the best of my knowledge, Sumitomo's mine and refining facilities are already operating at capacity and there are no disclosed plans to triple or quintuple Sumitomo's cobalt production and processing capacity to accommodate new demand from Tesla's gigafactory.

(20min delay)

(20min delay)