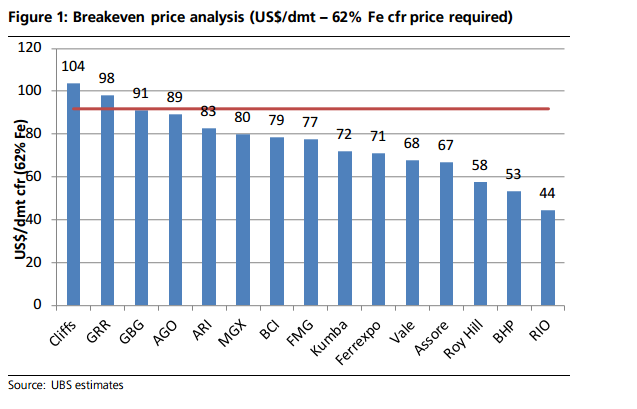

I thought this graph from the BCI thread might be of interest for holders;

With an OPEX of $41 and shipping that management has stated could be anywhere from $17-$25, our rough break even point would be $58-$66.

Per the graph above, this puts EQX in the company of the likes of Roy Hill and Vale (and not far off BHP). Not bad for a 2mtpa operation!

This does not factor in any premium that may be achieved due to the Fe content of the product.

If IO prices remain around $80p/t for 12 months+, it may be hard to attract funding in that time. The positive for EQX is that if $80p/t prices remain, there will be a lot of higher cost producers in Australia and abroad leaving the market. IMO this will, in time, create an upswing in prices. The question is, how long will this shake out take?

The big positive EQX has is the $40m in the bank and minimal cash burn ($1.5m per quarter). This provides a lot of protection in a worst case scenario of a long term $80p/t IO price and inability to lock in finance. The last thing you want is to be having to raise capital at these lows.

Good luck!

I thought this graph from the BCI thread might be of interest...

Add to My Watchlist

What is My Watchlist?

(20min delay) (20min delay)

|

|||||

|

Last

13.0¢ |

Change

0.000(0.00%) |

Mkt cap ! $17.08M | |||

| Open | High | Low | Value | Volume |

| 0.0¢ | 0.0¢ | 0.0¢ | $0 | 0 |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 1 | 5000 | 13.5¢ |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| 16.0¢ | 498509 | 3 |

View Market Depth

| Last trade - 16.12pm 17/06/2025 (20 minute delay) ? |

| EQX (ASX) Chart |

Day chart unavailable