Northern Star has made another acquisition adding the Jundee mine to the portfolio.

Production to increase six-fold y-o-y based on newly released guidance.

Operational results instill confidence, but it's early days.

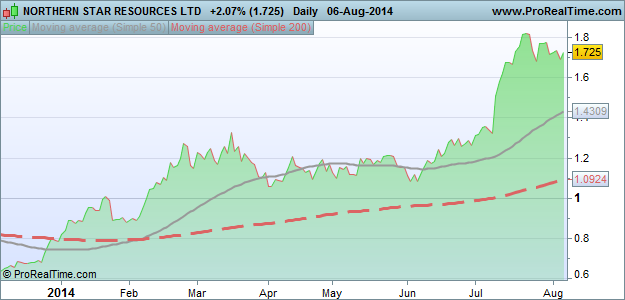

Share price has tripled since the start of the year.

Listening to Barrick Gold's (NYSE:ABX) Q2 earnings call we witnessed outgoing CEO James Skolasky stating: "More than $1.3 billion of non-core assets have been divested over the past year alone, none of which were expected to contribute any meaningful free cash flow at current prices in the foreseeable future. These efforts have lowered our cost profile and while it has meant lower production, they've strengthened our industry-leading portfolio overall which includes our five cornerstone gold operations."

We couldn't help a gleeful chuckle at the time and were all the happier to be a shareholder of Northern Star Resources (OTCPK:NESRF) rather that Barrick Gold. This gritty all-Australian gold miner has picked up three ex-Barrick gold mines in Western Australia on the cheap as we reported in early April. And judging from the data available at the moment, meaningful free cash flow will eventuate from these assets after all.

Northern Star has not stopped surprising its share holders since then, and has added the Jundee gold mine to its portfolio in May, again for what seems like a pittance this time disburdening Newmont Gold (NYSE:NEM).

Financial years end on June 30 across the board in Australia and we have been waiting with great interest for the first reports to be released by Northern Star since morphing from a small-cap also-ran to the second largest Australian gold miner within just a few months.

In the present article we will summarize the implications of the Jundee acquisition, take stock of the "new" Northern Star and summarize our findings from sifting through the operational data provided by the company so far. And as always, and as always we will provide our updated investment thesis at the end of the article. N.B. Northern Star's primary listing is on the Australian Stock Exchange where shares of the company trade with much liquidity. US-based investors might also consider using the pink sheets, but should be aware of the low trading volumes. N.B. Northern Star Resources reports in Australian Dollars. We have used an exchange ratio of A$1 = $0.93 in this article, and have added A$ values in brackets in some places to facilitate comparison with reported values. N.B. Northern Star Resources follows Australian practice with financial years starting on July 1 and ending on June 30. The Latest Acquisition: Jundee Gold Mine

The $76.7M (A$82.5M) acquisition of the Jundee underground mine was financed from cash and debt plus 10M shares for a third party in return for waiving first right of refusal to acquire the asset. This mine already has a 19 year production history and is expected to add 200+M ounces of gold annually to Northern Star's production profile for the foreseeable future.

In 2013 this mine was worked very hard for 279,000 ounces at all-in sustaining costs, or AISC, of $865/oz (A$930/oz), and Northern Star is taking a realistic approach by right-sizing production to around 200,000 ounces per annum and putting an emphasis on near mine exploration in order to expand the reserve of this mine for a meaningful mine life extension. As a result we expect AISC to increase in the current financial year.

At the time of the acquisition the mine had just 411,000 ounces in reserves, which would only support 2 years of mining at projected rates; and even when taking into account the existing additional resources and assuming a realistic conversion factor the mine life only increases to 4 years. Paulson Re-loaded?

Northern Star got started by acquiring the Paulson underground gold mine back in 2010. At the time the mine only had 8 months of mine life left. CEO Bill Beament and his team turned this mine around and has been improving and expanding it ever since. The Paulson mine remains a cornerstone asset and is expected to produce around 85,000 ounces for AISC of $1050/oz (A$1125/oz) using middle of the range values from the guidance for the current financial year.

New mineralisation keeps turning up and the resource has grown to support a rolling 5 years of mine life with plenty of near mine targets still to be assessed. Management had known this mine intimately from previous employment, and had the conviction to take it over and turn it around.

Perhaps more to the point in the context of recent acquisitions is the fact that management also has prior hands-on experience with the assets taken over from Barrick Gold. Most members of Northern Star senior management are ex-Barrick members of staff and know the Plutonic, Kanowna Belle and Kundana mines well. In the conference calls in the wake of these acquisitions Mr Beament was oozing confidence that he could create value where Barrick could not (Of course, that's his job).

As it happens, we have had conversations with a geologist previously employed by Barrick Gold at one of the assets now in Northern Star's possession and were credibly told that working at this particular mine was overly bureaucratic, that there were too many layers of management, and that information from the engineers and geologists often didn't make it up high enough in the food chain to be of any consequence.

Mr Beament runs a much leaner operation than the majors, and when he promises (as he has) to extend these mines' lives and lower costs we are tempted to take his word for it, in expectation of a repeat performance of his achievements at the Paulson mine. Operational Results

The newly discovered Pegasus lode at the East Kundana mine complex can be accessed quite inexpensively from existing underground infrastructure and is set to be in production within a year. Annual contributions are currently projected at 50,000 ounces. The resource for this lode is wide open and currently stands at 763,000 ounces at a grade of 11.4 g/t.

Using drill data generated by Newmont Mining the company has also announced a resource and reserve update for the Jundee mine. 120,000 reserve ounces have been added, replacing most of the gold mined this year so far. And total resources have also increased. A substantial drilling program is under way.

And drilling at the Titan discovery at the original Paulson mine continues to show strong intercepts.

Especially developments at the East Kundana mine complex are very promising. Northern Star Has a 51% interest in the JV operating this asset and we can see much potential for value being added in the very short term. In this context it is worth noting the other JV partners, two inter-related small-cap miners with almost exclusive exposure to this mine: Tribune Resources (ASX:TBR) with a 36.75% interest in the JV and Rand Mining (ASX:RND) with a 12.25% interest. Your humble scribe is currently pondering a speculative investment based on the emerging Pegasus discovery.

Back to Northern Star, now. The group guidance for the 2015 financial year that started on July 1 2014 has been set at 550,000 to 600,000 ounces at AISC of $977/oz to $1,023/oz (A$1,050/oz to A$1,100/oz) - quite astonishing for a company that produced around 100,000 ounces per annum at similar costs just a year ago.

Through all these transformations Northern Star has maintained a strong balance sheet, and has been able to keep a cap on the share count. Investors have honored the effort and the share price has been going from strength to strength as evidenced by the chart at the start of this article. Takeaway & Investment Thesis

Management had assured investors that it was well prepared to bed down this massive expansion move, and performance so far confirms this claim. The company has formulated the goal of turning the company into a go-to name for international investors seeking exposure to gold in the safe jurisdiction of Australia. What's missing at the moment are large reserve bases at the individual mines to underpin mine longevity. CEO Bill Beament has made a point of addressing this issue by initiating an aggressive exploration campaign across all assets.

Financial results for the past financial year will be published within another month. These results will provide another important data point on the impact of the acquisition on the bottom line. We will await the release of this report before adding to our holdings.

Northern Star has been paying dividends, and it will be interesting to see if this year's dividend will differ from previous returns to shareholders.

Should management be able to deliver on promises made with regards to the performance of the "new" Northern Star, then we would expect a share price with a A$2 handle before the end of the year.

NST Price at posting:

$1.86 Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)