Perhaps this article from Seeking Alpha in the US has also provided buying interest from the US given the relative valuations of its NA peer.

Summary

Cheniere is an overleveraged company with weak fundamentals in an industry with a muddy outlook.

Lots of moving parts will challenge Cheniere over the next years.

The company is definitely not on sale at $74 per share and a significant drop can occur sooner than later.

Introduction

In my previous article about Cheniere Energy (NYSEMKT:LNG), I presented the company's scary fundamentals along with the industry's moving parts while encouraging all the existing and potential investors to go against the grain by avoiding or even shorting this stock at the price of $74 per share. I strongly recommend any investor to take a look at that article first before reading this article.

In this article, I will compare Cheniere to its publicly-traded peers from the international markets. I decided to write this peer group analysis because an investor cannot find such an analysis in any financial website to date while I strongly believe that peer analysis is essential to investment research and market positioning. When it comes to my investments, peer group analysis is a primary quantitative tool kit and a vital part of establishing a valuation for a particular stock.

Frankly speaking, it was not easy to unearth Cheniere's competitors because their primary listings are in Australia and in India. These peers are Liquefied Natural Gas (OTCPK:LNGLY) that trades on the Australian Stock Exchange (ASX) under the ticker "LNG", and Petronet LNG that trades only on the National Stock Exchange of India (NSE) under the ticker "Petronet". Liquefied Natural Gas Limited From Australia

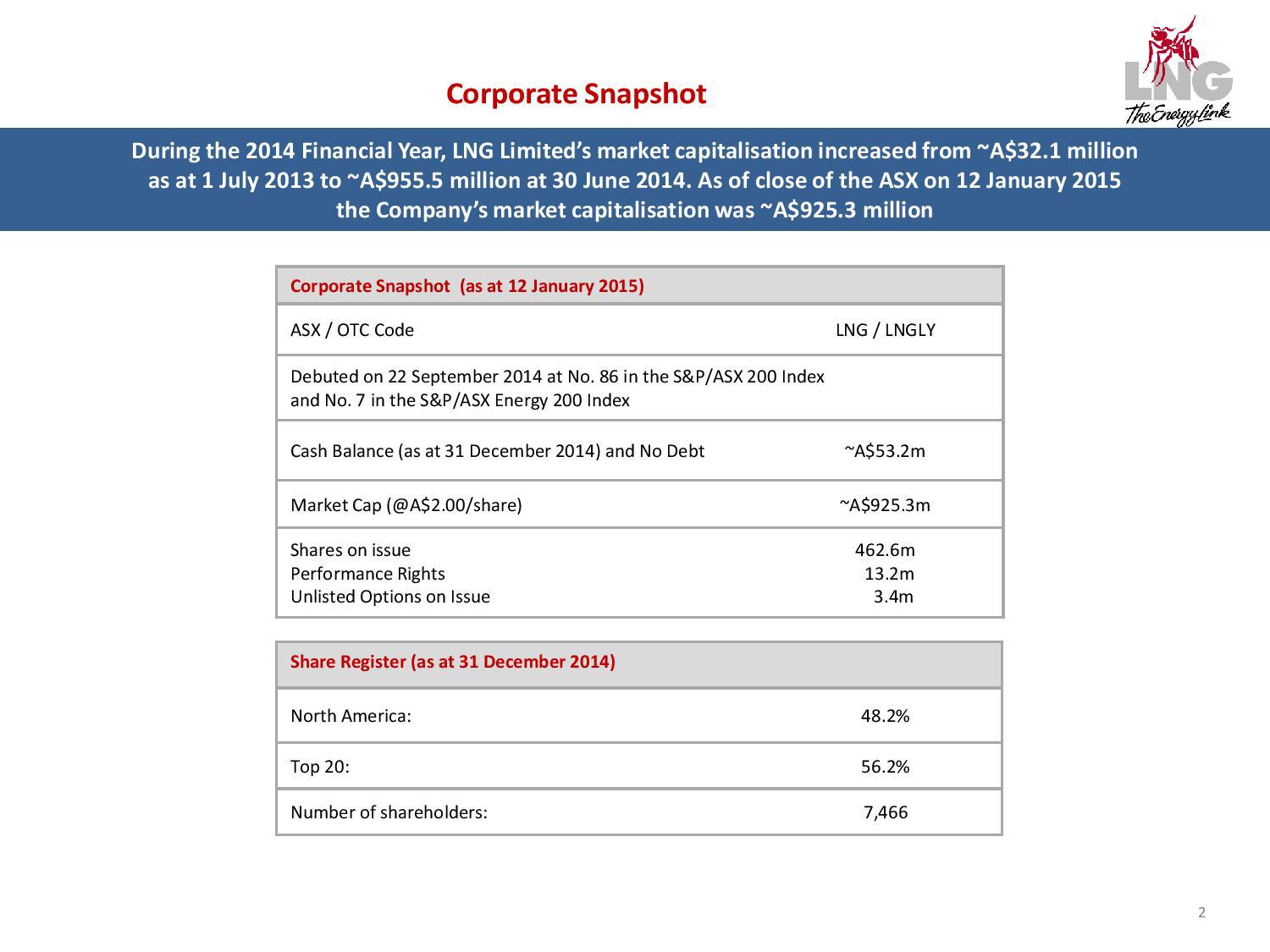

First, I will start with the fact that this company is 48% owned by North American investors, as illustrated below: (click to enlarge)

Given also that there is not currently another article about this emerging but unknown LNG player, I will present the company's assets and fundamentals first before proceeding with the calculations of the key metrics in the next paragraph: 1) The assets: The company's projects include the Gladstone LNG project located in Queensland (Australia), the Bear Head LNG project located in Nova Scotia (Canada) and the Magnolia LNG project located in Louisiana (United States).

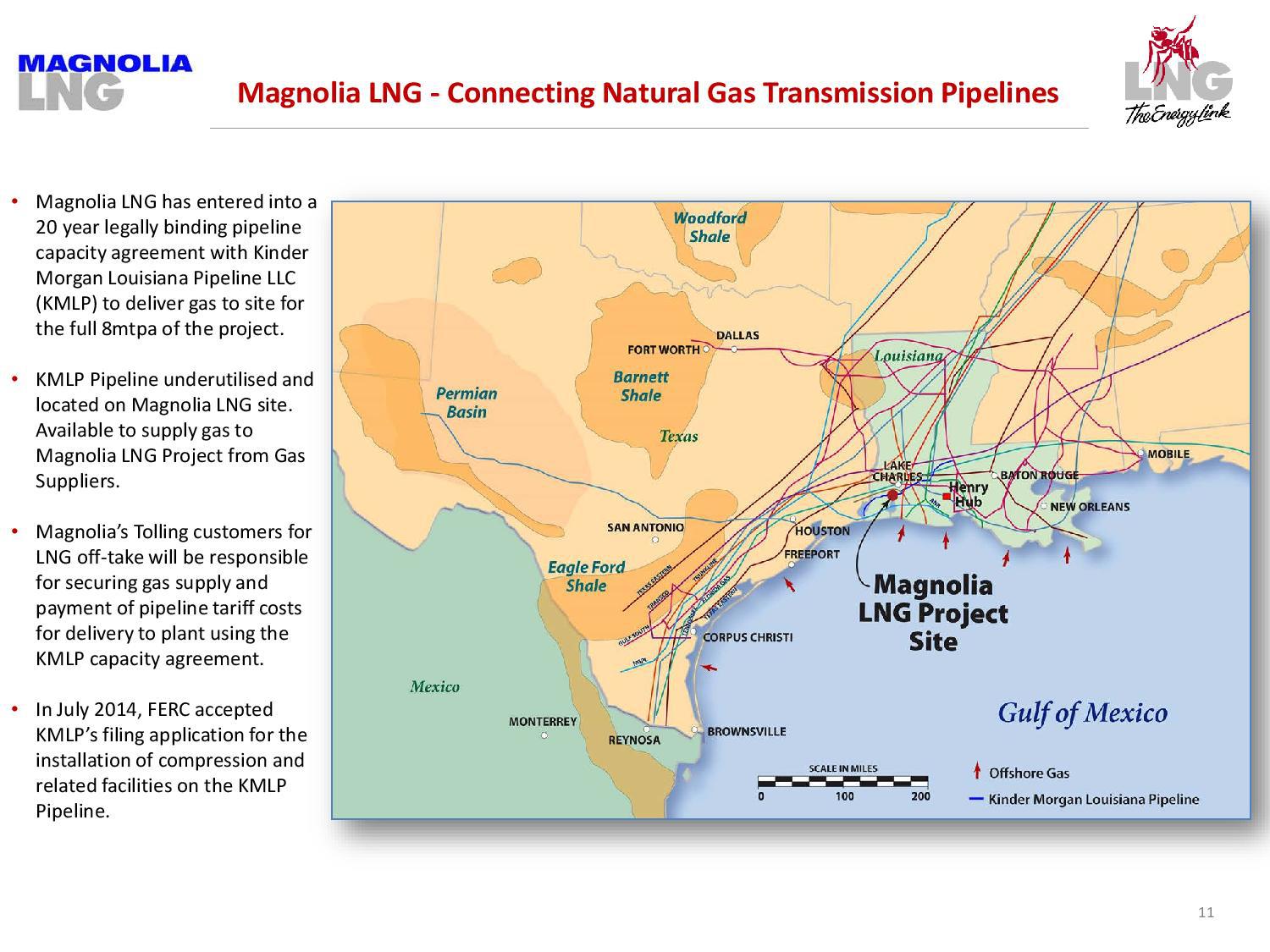

The company's Magnolia LNG project is illustrated below: (click to enlarge)

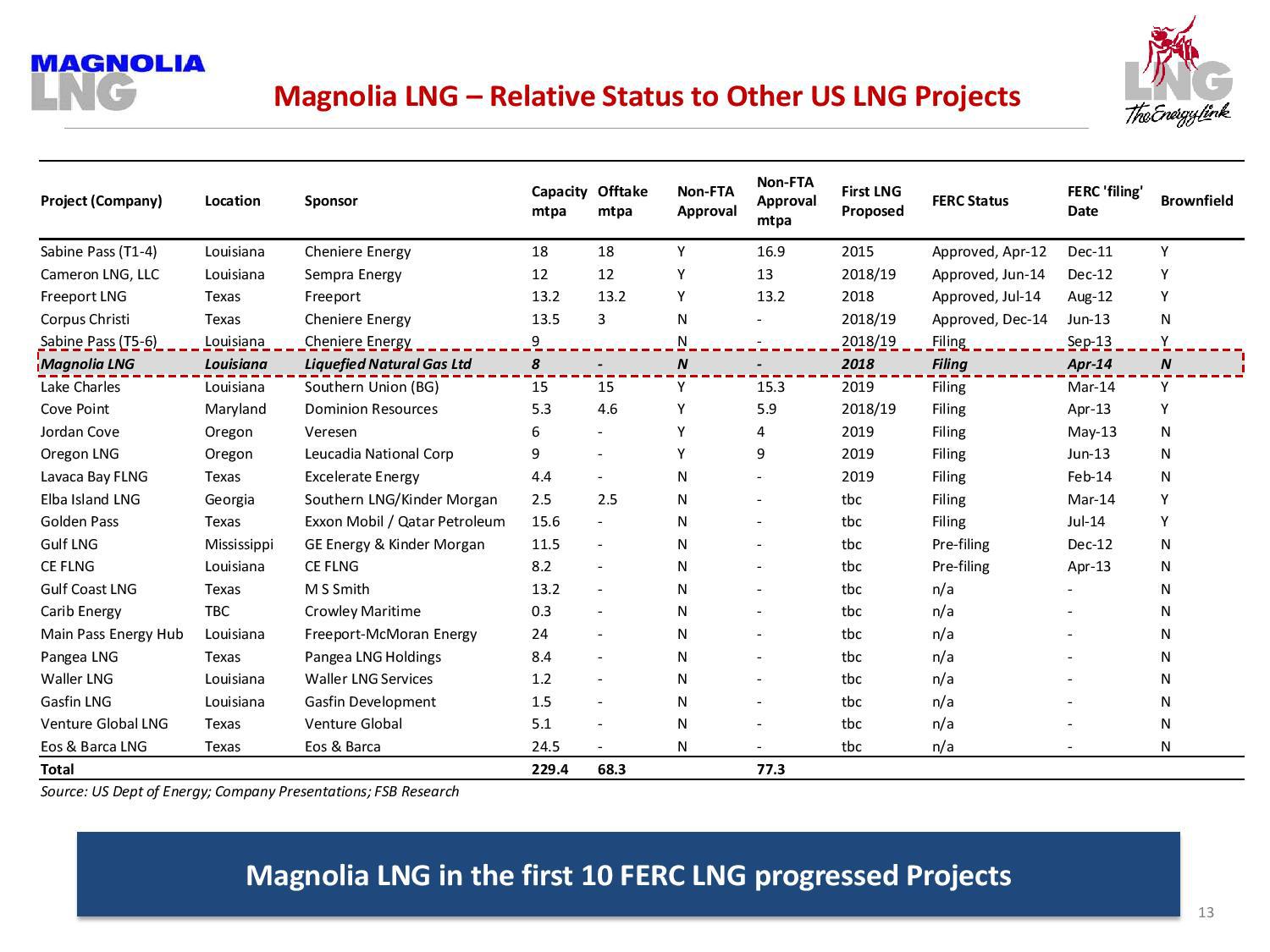

Magnolia LNG project is an 8 mtpa LNG facility with an estimated cost of $3.5 billion that targets final Environmental Impact Statement (EIS) approval by mid-2015 and first LNG export in Q4 2018, as illustrated below: (click to enlarge)

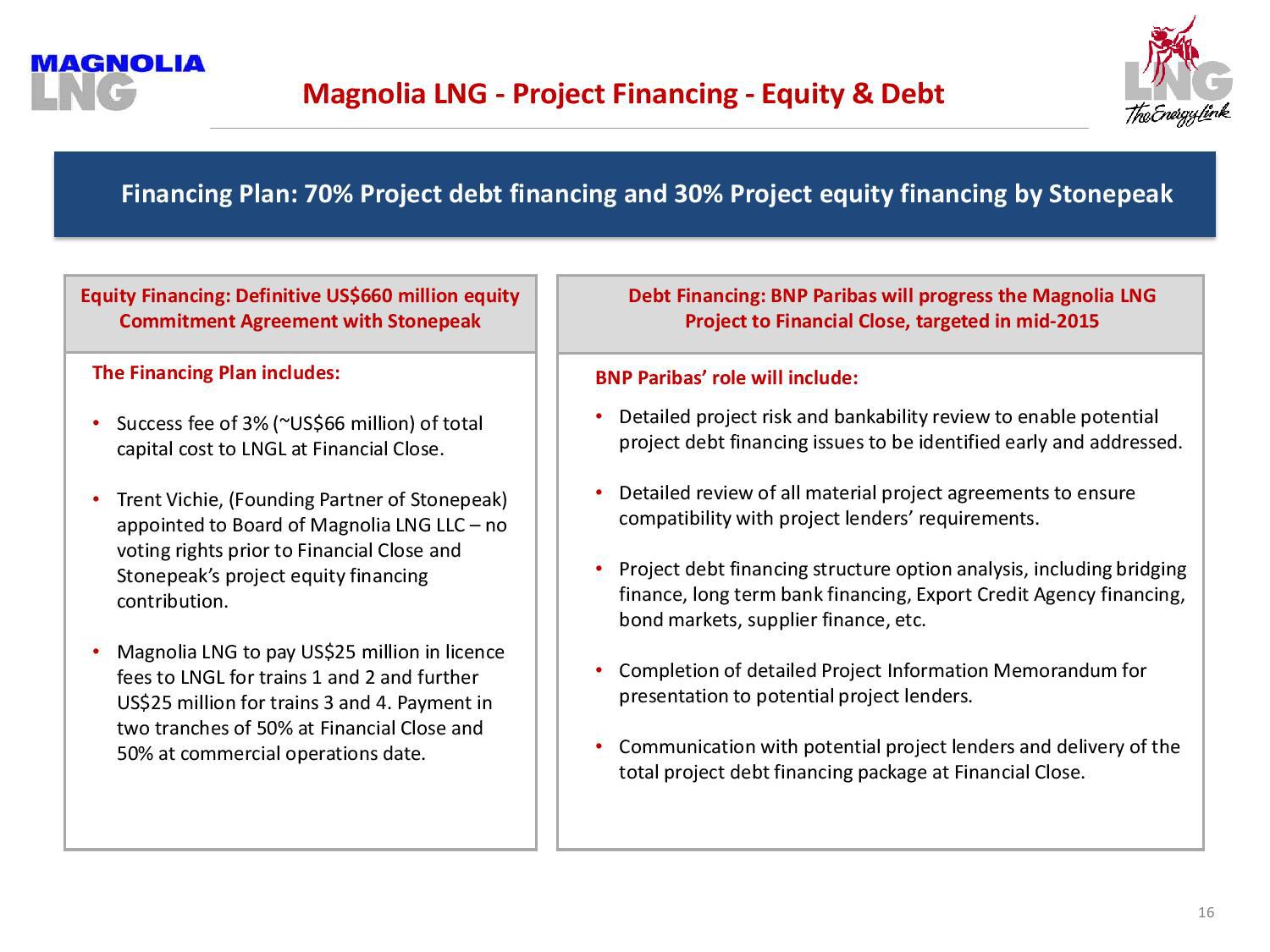

Debt from BNP Paribas (OTCPK:BNPQF) will fund 70% of this project ($2.45 billion) and equity financing will cover the remaining 30% ($1.05 billion), as illustrated below: (click to enlarge)

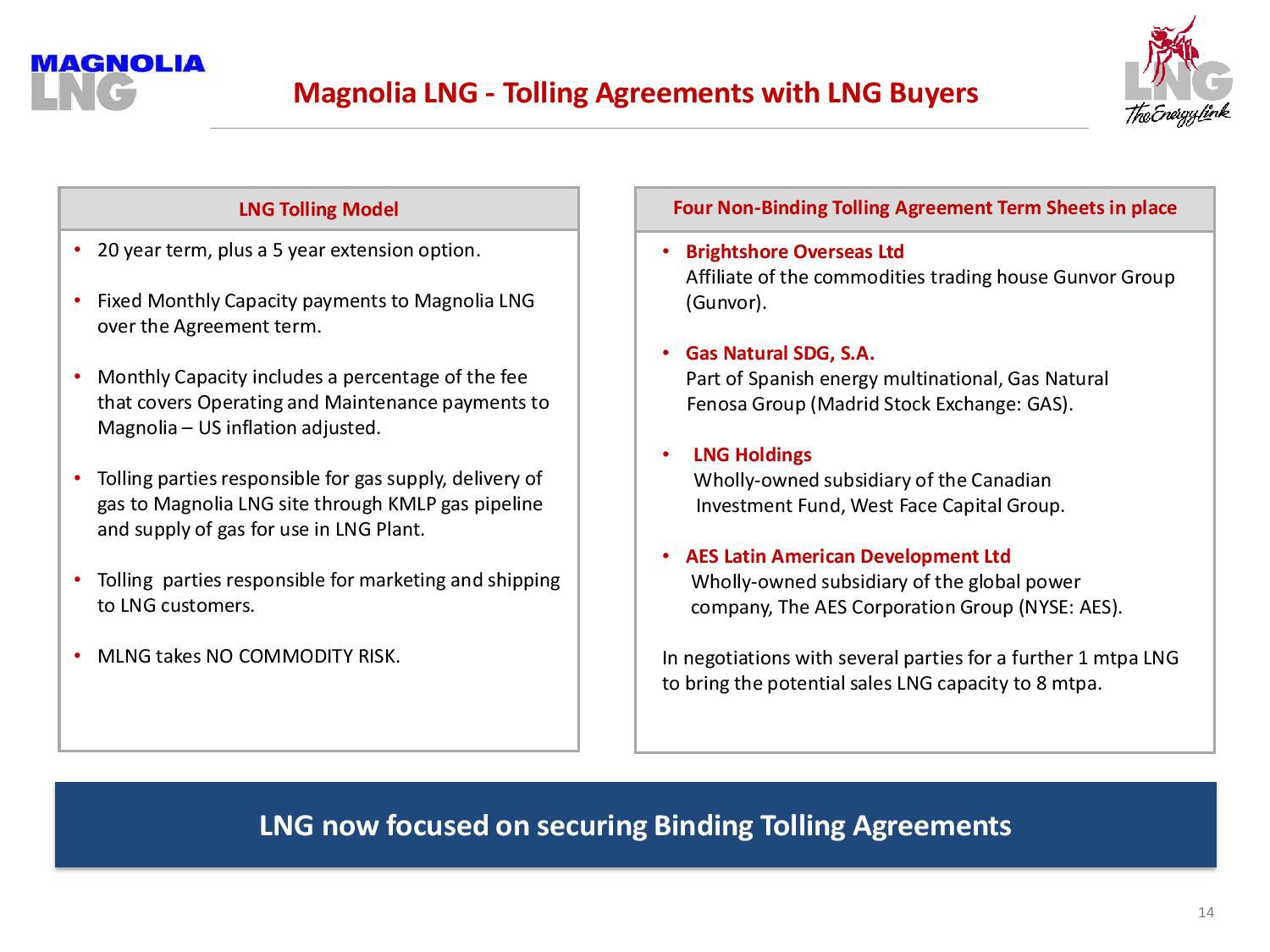

Also, the company currently is in negotiations with several parties to secure Binding Tolling Agreements, as illustrated below: (click to enlarge)

The company's Bear Head LNG project is illustrated below: (click to enlarge)

and below: (click to enlarge)

The company purchased 100% of the stock and assets of Bear Head LNG Corporation in August 2014 from Anadarko Petroleum (NYSE:APC) for $11 million. The Bear Head facility is expected to have a production capacity of 8 mtpa with potential for future expansion. A final investment decision on the project is expected in 2016. If the project gets the green light, the company anticipates that the Bear Head LNG export facility could be in commercial operation in 2019.

The company's Gladstone LNG project is illustrated below: (click to enlarge)

Gladstone LNG is a mid-scale 3.8 mtpa LNG plant that will be developed in two stages, with Stage 1 consisting of a 22km gas pipeline, LNG processing train (Train 1), 200,000 m3 LNG storage tank and jetty/ship loading facilities for up to 153,000 m3 LNG ships. Stage 1 will have a nominal LNG production capacity of 1.9 mtpa and a guaranteed capacity of 1.5 mtpa.

Stage 2 will comprise a second LNG processing train (Train 2), which will double the LNG production capacity to 3.8 mtpa. No additional LNG storage tank capacity or jetty/ship loading facilities will be required for Train 2. 2) The fundamentals: Based on the company's latest report (as of September 2014), I created the table below (1 USD = 1.26 AUD):

Column 1

Column 2

0

{colgroup}

1

{col}{/col}{col}{/col}

2

{/colgroup}

3

RevenueFY 2015 (*)

< $1 Billion

4

StockholderEquity(Sep 2014)

$70 Million (**)

5

Total Liabilities (Sep 2014)

$4 Million

6

Total Liabilities / Stockholder Equity (Sep 2014)

0.06

7

EV(Jan 23, 2015)

$1 Billion

8

Net Debt(Sep 2014)

-$50 Million

9

EBITDAFY 2015(*)

No Forecast

(*): Estimate.

(**): Including the placement of August 2014.

The company has been losing money while also having low debt ratios and negative operating cash flow over the last quarters. However, this is a result of the fact that the company's growth story from its core operations hasn't begun yet.

Once the company completes its Magnolia LNG project, the total liabilities-to-equity ratio is estimated to be approximately 2.5 times. Petronet LNG From India

This is another obscure stock with no analyst coverage in North America to date; so let's first take a closer look at the company's assets and fundamentals, according to the latest quarterly report: 1) The assets: Petronet LNG is engaged in the import, re-gasification, and supply of LNG in India. The company owns and operates an LNG regasification terminal with the name plate capacity of 10 mtpa at Dahej in the state of Gujarat, as well as an LNG terminal with a name plate capacity of 5 mtpa at Kochi in the state of Kerala, as illustrated below: (Source: Petronet's website)

and below: (Source: Petronet's website)

and below: (Source: Petronet's website)

Also, the company has signed a firm and binding term sheet for developing a third land-based LNG terminal at Gangavaram Port, Andhra Pradesh on the east coast of India with an initial capacity of 5.0 Mmtpa, and is currently in the process to build it.

Actually, Petronet LNG is doing in India the opposite of what Cheniere will be doing in Texas. And, those investors who want to deepen their knowledge of these plants can also take a look at the privately-held Canaport LNG in Canadaand GNL Quintero in Chile. 2) The fundamentals: Based on the company's latest report (as of September 2014), I created the table below (1 USD = 61.4 INR):

Column 1

Column 2

0

{colgroup}

1

{col}{/col}{col}{/col}

2

{/colgroup}

3

RevenueFY 2015 (*)

$7 Billion

4

StockholderEquity(Sep 2014)

$880 Million

5

Total Liabilities (Sep 2014)

$1.2 Billion

6

Total Liabilities / Stockholder Equity (Sep 2014)

1.36 times

7

EV(Jan 23, 2015)

$2.52 Billion

8

Net Debt(Sep 2014)

$163 Million

9

EBITDAFY 2015(*)

$358 Million

(*): Estimate. Cheniere Energy

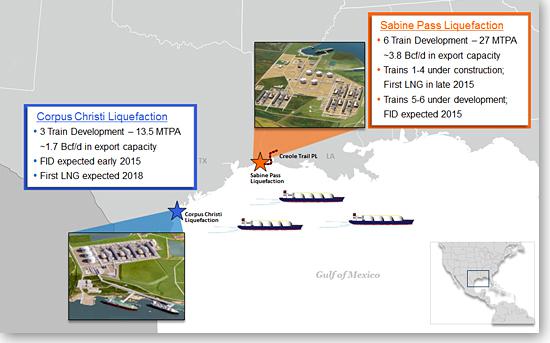

As a reminder, I will briefly present again Cheniere's assets and fundamentals that will help us draw conclusions into the next paragraphs: 1) The assets: Cheniere's Sabine Pass Liquefaction (SPL) terminal has 6 trains (T1-6) with a total capacity of 27 mtpa while the Corpus Christi Liquefaction (CCL) terminal has 3 trains (T1-3) with a total capacity of 13.5 mtpa, as illustrated below: (Source: Cheniere website)

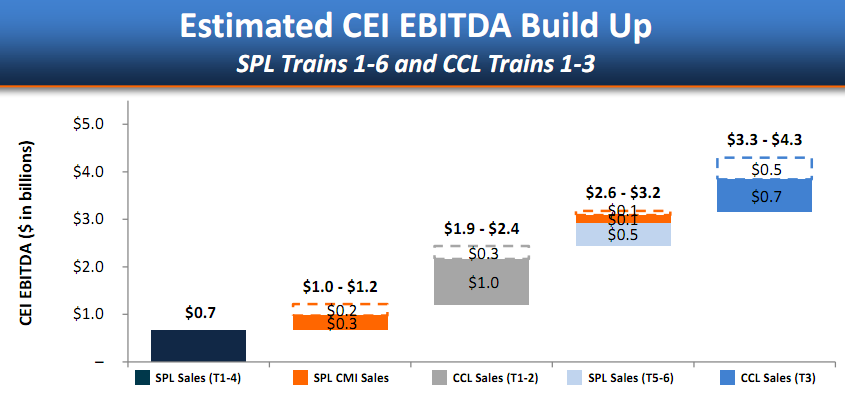

The final investment decision about the CCL project is still pending. Assuming that the CCL project will get the green light, Cheniere's total capacity from both projects will be 40.5 mtpa. 2) The fundamentals: Let's start with the fact that Cheniere's total liabilities-to-equity ratio currently is a whopping 78.5 times. The company also estimates that the 9 trains will generate adjusted EBITDA between $3.3 billion and $4.3 billion, as illustrated below: (click to enlarge)

For my calculations, I will use the average EBITDA of $3.8 billion.

By deducting the average EBITDA of $1.15 billion generated by CCL Sales (T1-2) from the total average EBITDA of $2.9 billion, thanks to SPL Sales (T5-6), I find that Cheniere's first facility (Sabine Pass) will generate approximately $1.75 billion EBITDA (2.9 - 1.15 = 1.75), once all the 6 trains are up and running.

Therefore, the second facility in Corpus Christi is estimated to generate the remaining $2.05 billion EBITDA (3.8 - 1.75 = 2.05), once it is fully operational.

Let's find now Cheniere's key metrics based on these EBITDA figures and the following two scenarios: A) No more debt for the completion of SPL:As of September 2014, Cheniere had approximately $9 billion long-term debt, $1.1 billion working capital surplus, almost $8 billion net debt and negative stockholder equity at $152 million. Also, Cheniere's market cap is $17.5 billion and the Enterprise Value is $25.5 billion, at the price of $74 per share.

Under this scenario, there are two options, depending on the company's pending decision about Corpus Christi: i) Sabine Pass Only: Based on an average EBITDA of $1.75 billion, Cheniere's Net Debt-to-EBITDA ratio is 4.57 times (8/1.75) and the EV-to-EBITDA ratio is 14.57 times (25.5/1.75) at the price of $74 per share, assuming that the company will not load more debt for the completion of this facility by 2019. ii) Sabine Pass and Corpus Christi:According to the company, the Corpus Christi Liquefaction Project, which is being designed for up to three trains with expected aggregate nominal production capacity of approximately 13.5 mtpa of LNG, will cost approximately $12 billion. The company has said that the project will be funded from a combination of debt and equity financings, but the final financing structure has not been completed yet.

As a result, we do not currently know the relative proportion of shareholders' equity and debt used to finance this project. However, it seems that this project will be mostly funded by debt, based on the latest corporate press release linked above:

"All financing commitments have been obtained for the Liquefaction Project, including a portion of the proceeds from $1 billion of convertible notes issued by Cheniere Energy, Inc. in November 2014 and the recently announced approximately $11.5 billion of debt commitments received from several financial institutions in December 2014".

According to Bloomberg, Cheniere is planning to raise as much as $11.5 billion of debt to help fund the construction of its Corpus Christi facility, and the company has tapped 18 banks to arrange the financing.

After all, we can safely assume that the company's net debt will swell to approximately $20 billion upon completion of the second facility in Corpus Christi.

Assuming also that Cheniere will remain at the price of $74 per share by the completion of the Corpus Christi project, the company's enterprise value will be $37.5 billion by the time it begins exporting LNG from its second facility.

Based on an average EBITDA of $3.8 billion, Cheniere's Net Debt-to-EBITDA ratio is 5.26 times (20/3.8) and the EV-to-EBITDA ratio is 9.87 times(37.5/3.8) at the price of $74 per share, assuming that the company will not load more debt for the completion of the first facility (Sabine Pass) by 2019. B) More debt for the completion of SPL: This is the most likely scenario, because Cheniere has a long way to go before it completes this facility. The cash of $1.4 billion in September 2014, coupled with the negative operating cash flow, supports the belief that Cheniere will have to incur more debt to finance the completion of the Trains 3, 4, 5 and 6.

My conservative estimate is that Cheniere will load another $3 billion in debt to complete Sabine Pass by 2019, given that T3-4 are 50% complete (contract price ~$3.8 billion) and the construction for T5-6 (estimated contract price $3.5-$4 billion) has not started yet.

Under this scenario, there are again two options, depending on the company's pending decision about Corpus Christi: i) Sabine Pass Only: In this case, the Net Debt rises to approximately $11 billion and the Enterprise Value reaches $28.5 billion at the price of $74 per share.

Based on an average EBITDA of $1.75 billion, Cheniere's Net Debt-to-EBITDA ratio is 6.29 times (11/1.75) and the EV-to-EBITDA ratio is 16.29 times(28.5/1.75). ii) Sabine Pass and Corpus Christi: In this case, the Net Debt rises to approximately $23 billion and the Enterprise Value reaches $40.5 billion at the price of $74 per share.

Based on an average EBITDA of $3.8 billion, Cheniere's Net Debt-to-EBITDA ratio is 6.05 times (23/3.8) and the EV-to EBITDA-ratio is 10.66 times(40.5/3.8). The Key Metrics

And in this paragraph, let's summarize all the previous results at the table below:

Column 1

Column 2

Column 3

Column 4

0

{colgroup}

1

{col}{/col}{col}{/col}{col}{/col}{col}{/col}

2

{/colgroup}

3

EV ($ million) (Jan 23, 2015)

Net Debt ---------- EBITDA

EV ---------- EBITDA

4

Liquefied Natural Gas Limited (20 mtpa)

1,000

No Official Forecast

No Official Forecast

5

Petronet LNG (20 mtpa)

2,520

0.46

7.04

6

Cheniere With SPL Only (27 mtpa) (No more debt for the completion of SPL)

25,500

4.57

14.57

7

Cheniere With SPL &CCL (40.5 mtpa) (No more debt for the completion of SPL)

37,500

5.26

9.87

8

Cheniere With SPL Only (27 mtpa) (More debt for the completion of SPL)

28,500

6.29

16.29

9

Cheniere With SPL &CCL (40.5 mtpa) (More debt for the completion of SPL)

40,500

6.05

10.66

Based on all these figures, I come to the following conclusions where the numbers speak volumes and underline Cheniere's gross overvaluation: 1) Liquefied Natural Gas Limited with 20 mtpa currently has enterprise value at $1 billion. 2) Petronet with 20 mtpa currently has enterprise value at $2.52 billion. Petronet is a proven, profitable and growing company with a healthy balance sheet and a very low Net Debt-to-EBITDA ratio. 3) Assuming a negative investment decision about CCL, Cheniere will have only SPL with 27 mtpa and its enterprise value ranges between $25.5 billion and $28.5 billion at the price of $74 per share, depending on the additional debt for the completion of the Train 3, 4, 5 and 6. 4) Assuming a negative investment decision about CCL, Cheniere's enterprise value at the price of $74 per share is 27 times (on average) higher than Liquefied Natural Gas Limited's current enterprise value although Cheniere's capacity is 1.35 times higher than the Australian company's capacity. 5) Assuming a negative investment decision about CCL, Cheniere's enterprise value at the price of $74 per share is 10.7times (on average) higher than Petronet's current enterprise value although Cheniere's capacity is 1.35 timeshigher than the Indian company's capacity. 6) Assuming a positive investment decision about CCL, Cheniere will have SPL and CCL with 40.5 mtpa and its enterprise value ranges between $37.5 billion and $40.5 billion at the price of $74 per share, depending on the additional debt for the completion of the Trains 3, 4, 5 and 6. 7) Assuming a positive investment decision about CCL, Cheniere's enterprise value at the price of $74 per share is 39times (on average) higher than Liquefied Natural Gas Limited's current enterprise value although Cheniere's capacity is 2.03 times higher than the Australian company's capacity. 8) Assuming a positive investment decision about CCL, Cheniere's enterprise value at the price of $74 per share is 15.48times (on average) higher than Petronet's current enterprise value although Cheniere's capacity is 2.03 timeshigher than the Indian company's capacity. My Takeaway

The best investors choose their trades very meticulously and invest only when the greater probabilities are on their side. In fact, they are willing to miss an investment if not all the probabilities line up in their favor.

To me, this is the case with Cheniere, which does not fit my bill at $74 per share. To me, many factors spell trouble for Cheniere's future, as presented both in this article and in my previous one linked above. As such, I will not buy the LNG euphoria and the LNG speculation that have been priced into Cheniere, given also that a climate of fear is an investor's friend while a euphoric world is an investor's enemy.

My comments: Perhaps instead value investors are starting to piece together the LNG.AU story esp. following the recent (further) buying by Baupost.