This is great. US stealth fighter F-35 uses over 900lbs of rare earth materials. The fighter is costly to began with, has huge over-runs in cost and can even burn off its own tail wing at super-sonic speed. The US is looking, IMO, for an out a way to stop production. China may have just the solution:Rare Earth Supply Is Emerging As A Key Risk For Lockheed Martin

(1,074 followers)SummaryDue to the ongoing United States-China trade war, China has subtly threaten to restrict their rare earth exports to the United States.

Unfortunately for Lockheed Martin many of their core military programs rely on these elements, such as their flagship F-35 stealth fighter yet.

If this scenario eventuates the short to medium-term impact would likely be significant and thus investors who believe this will occur should consider reducing their investment.

Introduction

Earlier this year in February I published an article outlining my investment thesis for Lockheed Martin (LMT) shares and following on from this I would like to subsequently discuss an investment risk that has recently evolved. Due to the ongoing United States-China trade war, China has recently been subtly threatening to restrict their exports of rare earths to the United States. These are widely used throughout many modern high-tech products, which unfortunately includes Lockheed Martin’s flagship program, the F-35 stealth fighter jet. Given the attention this has received from the financial media, I’m rather surprised it hasn’t yet materially impacted their share price.

Current Situation

On the surface it would initially seem that Lockheed Martin is quite well insulated from the United States-China trade war given a massive 70% of their total revenue is derived from sales to the United States government. This standpoint has recently shifted following China’s subtle threats to restrict their market dominating exports of rare earths to the United States. A single one of Lockheed Martin’s F-35 stealth fighter jets requires 920lb of rare earths, with various other military programs ranging from lasers to the warship also requiring these same elements.

I’m rather surprised China seems to be considering this path as I believe it won’t provide them with any long-term benefit and at absolute best would be a parasitic victory. Similar to how OPEC’s 1973 Oil Embargo led to a greater focus on fuel efficiency and alternative fuels as well as finding new sources of oil supply, all of which undermined their interests in the following decades.

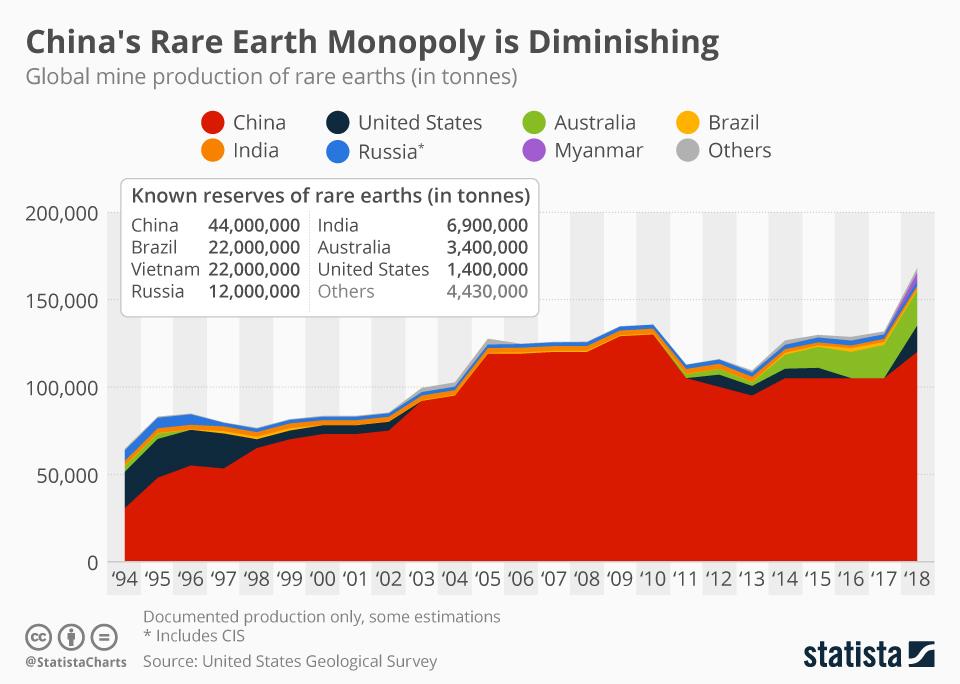

Whether China actually follows through on these threats and restricts exports to the United States remains unknown, however, considering they chose this course of action in 2010 against Japan it certainly remains a possibility. I’ve included a chart below that provides an overview of the current production and reserve landscape for the rare earths industry.

Image Source: Statista.

The Potential Impact

Accessing the potential impact to Lockheed Martin’s earnings is unfortunately difficult to exactly estimate as there are many uncertainties, however, broad estimates indicate it could be quite significant. The uncertainties range from determining exactly which rare earths are restricted, the extent to which they’re restricted and the actions taken by their management and the United States government to mitigate the situation.

During the last year the F-35 program accounted for 27% of their total revenue and 68% of their aeronautics business segment revenue. If the most extreme scenario eventuated, whereby they were forced to temporarily halt their production completely, their business segment operating profit would decrease by approximately $1.54B or 27% assuming their aeronautics margins remained static. This is unlikely as there would certainly be various fixed costs that would remain changed, thus leading to margin compression and hence even lower earnings.

Although this estimate may sound too extreme it’s important to remember that in the short to medium-term sourcing or replacing these rare earths elsewhere could be very difficult and costly if at all possible. Furthermore, they are also widely used throughout their various other military programs and thus even if the impact to the F-35 program is minimized, it’s likely to impact their other programs as well and thus further hurting their earnings.

Valuation

Implementing this risk into my original valuation is also quite difficult as it depends a binary outcome and thus the intrinsic valuation will either remain unchanged or drop significantly. My original article estimated the intrinsic value for shares to be $360.16 to $398.65, which I continue to support providing China doesn’t restrict rare earth exports. Due to the aforementioned uncertainties it’s impractical to determine an estimated intrinsic valuation for the alternative scenario, however, it’s safe to say it would certainly be under $300 per share.

When I first published my valuation their share price was $301.50 and has since rallied steadily to $349.08 at the time of writing. The investment decision moving forward will depend on an investor’s belief regarding the outcome of these trade tensions. If it’s believed that China will restrict rare earth exports they should consider selling or at least reducing the size of their investment. On the contrary if the opposite outcome is believed, they should consider continuing to hold as the current market price no longer provides as significant upside as earlier this year to justify buying more shares.

Final Thoughts

Even though I don’t wish to derail my topic, I would like to mention that I believe the West should actually be thankful for China threatening to restrict rare earth exports now rather than in the future. It’s considerably more convenient for this risk to be brought to the forefront during times of peace between the world’s major militaries.

Whilst I cannot and don’t wish to forecast whether a future military conflict between the United States and China, Russia or North Korea will occur, it’s an undeniable long-term risk. If the previous situation of blindly relying on China were to continue and a military conflict were to occur in the future, it would be the worst possible time for the United States to suddenly lose it’s vital rare earth supply. Losing this supply would impede their ability to rapidly increase production of high-tech military equipment when it’s urgently required. By this risk being brought to the forefront now, it provides the West time to lower their reliance on China regardless of what the future may bring.

Finally, I personally feel that by merely threatening to restrict rare earth supply to the United States, China has shown short-term thinking and is effectively shooting themselves in the foot in the long-term. Even if they reverse course and cease threatening to restrict rare earth exports, I believe it’s too late as the West will continue seeking to reduce its reliance on China, both at the corporate and government level. This applies to the allies of the United States, with the Australian Defense Minister stating this has become an issue of strategic importance for Australia and the other Pacific allies of South Korea and Japan.

Conclusion

Although the prospects of China restricting their rare earth exports to the United States would certainly cause a significant disruption to Lockheed Martin in the short to medium-term, I believe it wouldn’t prove to be a permanent problem. Eventually the supply deficit will prompt new supply outside of China as well as research into alternative minerals. Granted the short to medium-term impact would still hammer their share price and thus investors should consider reducing their investments if they believe such an outcome will eventuate.

Notes: Unless specified otherwise, all figures in this article were taken from Lockheed Martin’s 2018 Annual Report, all calculated figures were performed by the author.

Disclosure:I am/we are long LMT.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

China/US Trade War, page-162

Add LYC (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

$5.93 |

Change

-0.020(0.34%) |

Mkt cap ! $5.542B | |||

| Open | High | Low | Value | Volume |

| $6.04 | $6.04 | $5.93 | $23.75M | 3.975M |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 8 | 128544 | $5.92 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $5.95 | 12481 | 2 |

View Market Depth

| Last trade - 16.10pm 28/06/2024 (20 minute delay) ? |

| LYC (ASX) Chart |