Hi all,

Found this.....Not good for coal companies like RES

FP, can you still see any movement in the price of coal going up this year or next?

Summary

The key reasons for coal prices' multi-year bear market are continuously weakening seaborne demand, and the slow response of the supply side.

Consumption is contracting from the Atlantic to the Pacific.

Further production cuts needed to balance the global coal market.

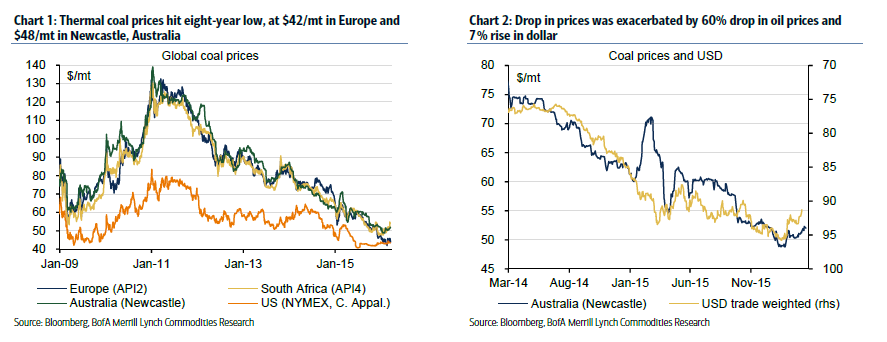

Thermal coal prices hit a nine-year low in recent weeks, touching $42/mt in Europe and $48/mt in Newcastle, Australia. The key reasons for coal prices' multi-year bear market are continuously weakening seaborne demand and the slow response of the supply side, which means it takes years for this market to rebalance. In the last two years, the drop in prices was exacerbated by the 60% drop in oil prices and 7% rise in the dollar.

Moreover, the bearish fundamentals persist, as demand continues to contract. As such, we expect prices to continue to descend in 2016 and in 2017, to force another round of production cuts to balance the market.

Consumption is contracting from the Atlantic to the Pacific

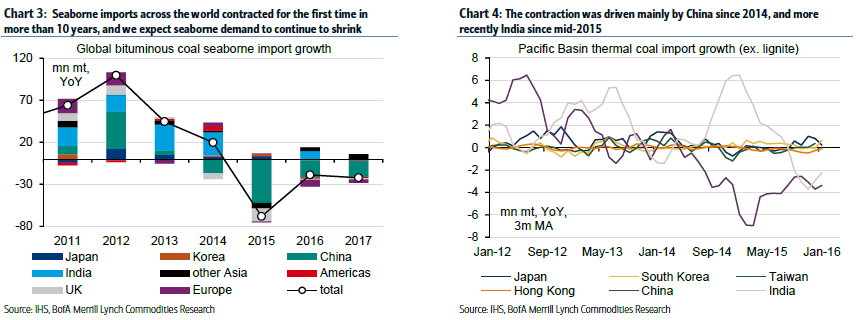

Falling demand for imports is the main driver of price weakness in the seaborne coal market. In 2015, seaborne imports across the world contracted for the first time in more than 10 years, down 9% YoY, and we expect seaborne demand to continue to shrink in the next two years at least. The contraction was mainly driven by China since 2014, and more recently also by India since mid-2015. These two countries comprise over 30% of the seaborne market, and are hence a major influence on seaborne prices. Elsewhere in the Pacific basin, both Japanese and Korean demand, together also 30% of the market, is set to contract slightly in the next two years as Korea brings new nuclear power plants online and Japan restarts old ones. In the Atlantic Basin, the picture is not much better. UK coal demand for power generation is now contracting strongly, as gas is cheaper than coal due to an oversupplied global gas market, and in our view, the European continent will soon follow to shed coal demand in favor of gas.

Chinese demand contractions intensifying as coal consumers are in recession

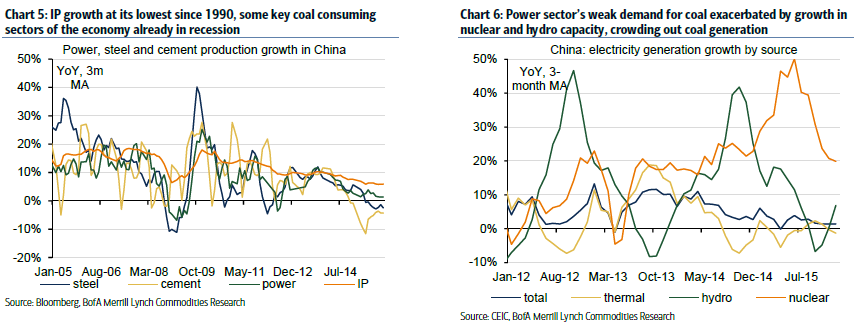

The Chinese macro picture looks increasingly weak for coal. Overall industrial production growth is at its lowest since 1990, and a number of key coal consuming sectors are already in recession, including steel and cement manufacturing. Power generation is not far behind, growing only 2% in 2015, down from a 10-year average of 10%. We expect power demand to grow by 2% each year in 2016 and 2017, and coal for power generation to contract by 4% p.a. on the ongoing switch to alternatives and improved generation efficiency. In addition, coal consumed for cement production will continue to decline due to low property starts. Overall, we see Chinese thermal coal demand falling 4%, or 100 million tons each year in 2016-17, which will force large cuts in both domestic production and imports.

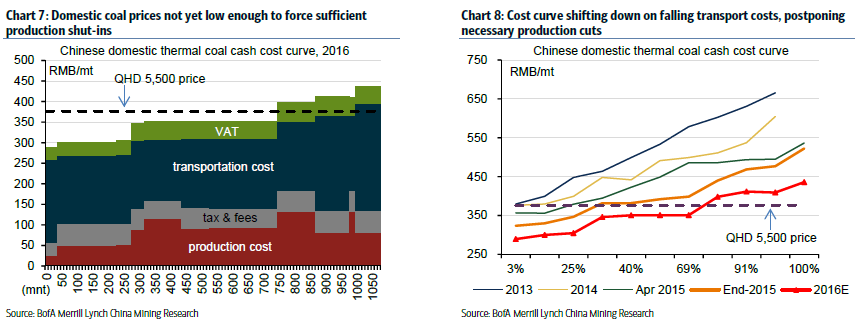

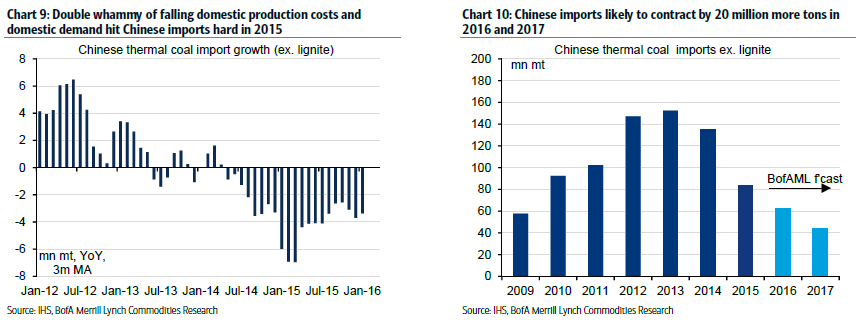

The Chinese coal market has been oversupplied for several years now, and domestic overcapacity is approaching 1 billion tons per year or 30% of domestic mining capacity. With demand set to continue to contract, we expect further production curtailments in 2016-17. Domestic coal prices are not yet low enough to force sufficient production shut-ins. Moreover, the cost curve keeps shifting down and rightwards on falling rail tariffs and expansions in rail capacity, which increases prices at the mine gate and thus postpones necessary production cuts. Delivered costs at the 70th percentile of the cost curve will fall by RMB50/mt this year to RMB350/mt. Domestic coal prices in the consuming regions in the South, currently trading at RMB380/mt (5,500kcal), will fall accordingly, in our view.

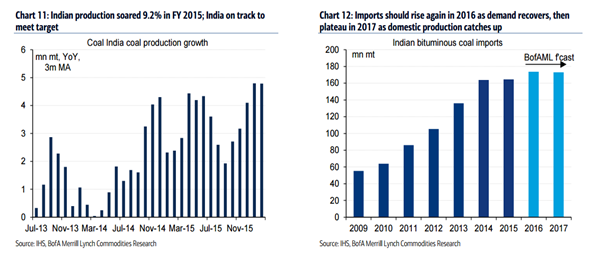

The double whammy of falling domestic production costs and falling domestic demand hit Chinese imports hard in 2015. Seaborne imports of thermal coal were down by a record 50 million tons, or 30%. Chinese imports are just a fraction of domestic coal demand, so even a small percentage drop in domestic demand in the coming years will have a huge relative impact on imports. We expect Chinese imports to contract by another 20 million tons each year in 2016 and 2017 (Chart 10), which by 2017 reduces Chinese imports by 50% from 2015 levels. In the global scheme of things, this means China alone is responsible for a 5% decline in global seaborne imports over the next two years. Needless to say, the impact on seaborne prices of the Chinese economy shunning coal is severe.

Indian imports are falling as domestic output soars

India used to make up for falling Chinese seaborne demand, but not anymore. Imports stagnated in 2015 and were flat for the first time in over a decade due to a combination of faltering demand and soaring domestic production. India has the world's fifth largest coal reserves, yet imports soared in the last 10 years to 2014 as the country struggled to increase its domestic production. The new government elected in 2014, led by Narendra Modi, fired up under the domestic mining sector by speeding up rail construction and making it easier for miners to expand. The government plans to double domestic production over 2016-20 by opening 60 additional coal mines. So far, Indian coal production soared by 9% in the first 11 months of FY 2015 (April-March 2015), and India is on track to meet its production target for the first time in years. We expect imports to rise again in 2016 as local demand recovers, and then plateau in 2017 as domestic production catches up with demand growth.

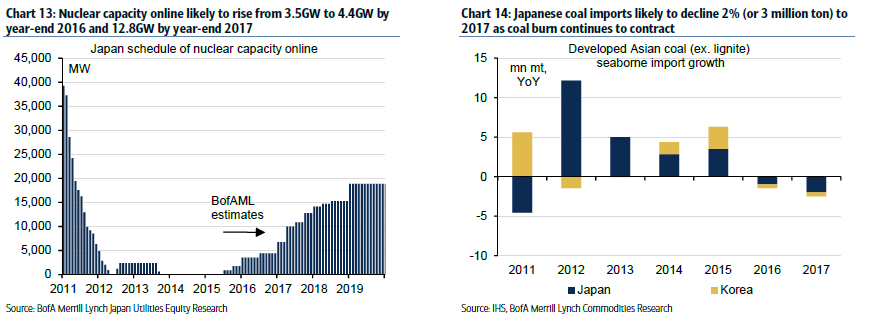

Developed Asian coal demand is contracting on nuclear start-ups

Elsewhere in the Pacific Basin, developed countries are also cutting back coal imports due to a shift to nuclear power. In Japan, three of the country's 48 reactors are now online, nuclear capacity online is expected to rise from 3.5GW at present to 4.4GW by end of 2016 and 12.8GW by end of 2017. Coal burn in power generation rose in 2013-14 on the completion of a couple of new coal fired power plants, yet coal generation contracted in 2015 as several nukes restarted and power demand has structurally declined. We expect Japanese coal imports to decline 2% (or 3 million tons) to 2017 as coal burn continues to contract. Meanwhile, South Korea is building new nuclear plants - one reactor started in 2015 and another is due in May this year. Most of the increase in nuclear output is likely to reduce coal demand, and we see Korean coal imports declining by 1 million tons to 2017.

Further production cuts needed to balance the global coal market

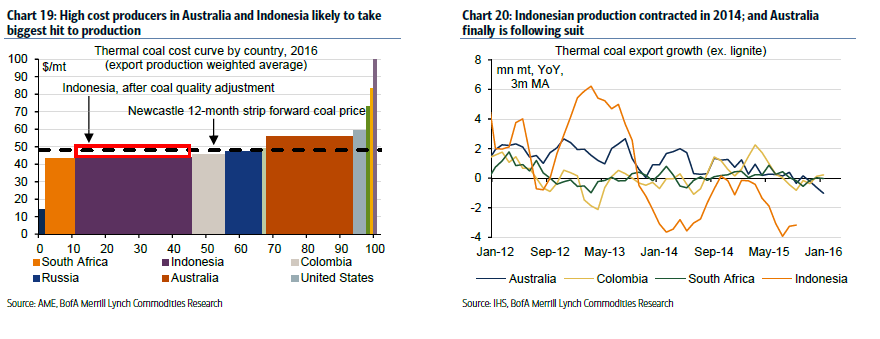

A 5% contraction in seaborne demand in 2016-17 will inflict more pain on producers. Lower oil prices, a stronger dollar, mine closures and other cost cutting measures have pushed cash cost lower in the last five years. Average seaborne FOB cash costs across the world are now $49/mt, down 23% since 2011. Yet prices have fallen much more, down 60% since 2011, and hence almost half of producers are not covering cash costs at current prices. The fact that so much production is already under water limits the downside to prices somewhat, yet the pressure on prices is still to the downside because of demand contractions. Prices will have to move lower still and deeper into the cost curve to force the necessary production cuts back to balance the market. High cost producers in Australia and Indonesia are likely to take the biggest hits to production. Indonesian production started contracting already in 2014, and now Australia finally is following suit.

Indonesian producers are taking the brunt of production shut-ins

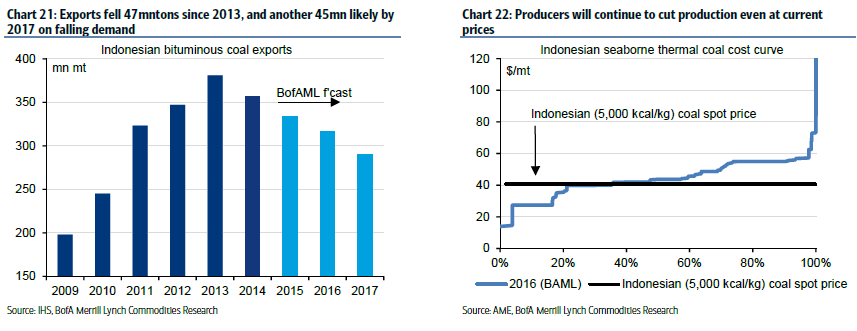

Indonesia is the largest single exporter into the seaborne market with its 40% market share, and the country is taking the brunt of the production cuts. Exports peaked at 380 million tons in 2013, and then fell by 47 million tons or 12% to 2015 as prices of Indo grades dropped by over 30% to $41/mt (for 5,000kcal). We expect another 45 million ton decline in export by 2017. We do not, however, think prices need to drop by another 30% to force similar sized production cuts to 2013-15. The cost curve is stabilizing as oil prices are starting to find a bottom - oil comprises as much as half of operating cash costs in Indonesia. And moreover, more than 60% of producers are already not covering operating cash costs at current prices, which means production will likely continue to fall even at current price levels.

Australian producers are pitching in with supply cuts

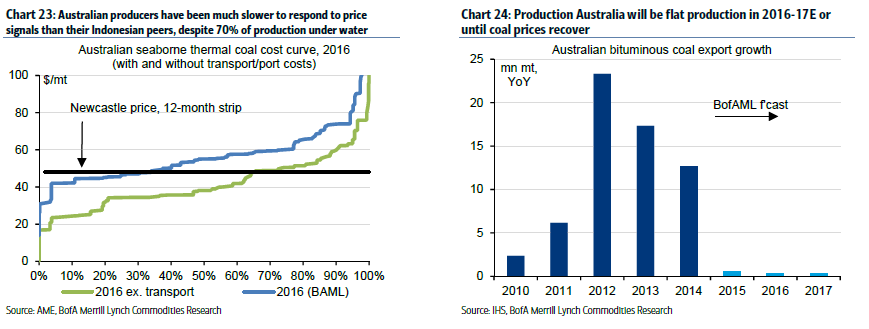

Australian producers have been much slower to respond to price signals than their Indonesian peers, and production cuts so far have been limited. This despite that 70% of production is not covering cash costs at the moment. The lack of supply response is mainly due to the structure of Australian rail and port capacity contracts. These contracts are typically take-or-pay with 10-15 year duration which makes the transport cost effectively a sunk cost that is incurred whether the capacity is used or not. Stripping out transport costs to get the variable cash costs, only 30% of producers are not covering variable cash costs. This is a sizeable chunk of production at 35 million tons. So far, Glencore (OTCPK:GLCNF) has shown restraint by reducing its Australian exports by 2 million tons in 2015, and total Australian exports were flat in 2015 after four years of strong expansions on mine ramp ups (Chart 24). We think production cuts will continue to offset mine ramp-ups in Australia for overall flat production in 2016-17, or at least until coal prices recover.

In conclusion, the coal market is in a secular decline and it has not yet reached a point of stabilization. To stabilize, we need to see more bankruptcies and supply cut to respond to a structural decline in demand. We don't see any investment opportunities in this sectorand think investors would be better off looking at natural gas or renewable energy sectors.

http://seekingalpha.com/article/3961065-coal-prices-9-year-lows-downside-ahead

Hi all, Found this.....Not good for coal companies like...

Add to My Watchlist

What is My Watchlist?