...Shapiro is one of my most respected home-grown investigative journalist.

...I applaud his honesty in telling the inconvenient truth, which in the past got him a lot of flak from aggrieved investors in denial

...but that didn't deter him.

This week, the world’s safe haven functioned like an emerging market

The usual flight to safety toward long-term US government bonds occurred at first but has since very much reversed. The reversal shows no signs of slowing.

Jonathan ShapiroSenior reporter

Apr 11, 2025 – 10.20am

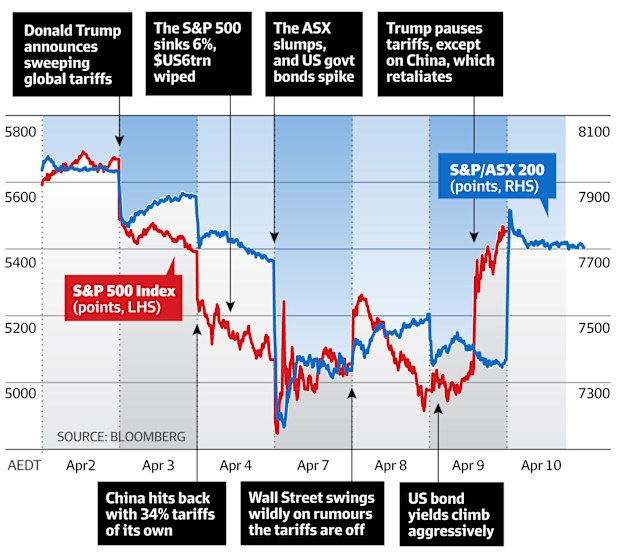

This week it’s been a tale of two markets. Global equity markets have been in a state of chaos, swinging from panic to relief and back to panic as US President Donald Trump wavered on tariffs but held the line on China.

Meanwhile, the bond market has been defying Trump, with long-term yields nudging higher to worrying levels, forcing him to call a 90-day truce with trade partners. The usual flight to safety toward long-term US government bonds occurred at first but has since very much reversed.

The reversal shows no signs of slowing.

That stocks and bonds have been falling together is unusual and unsettling. For decades investors have relied on gains in bonds to offset losses in stocks via a so-called 60/40 portfolio strategy.

But there is another disconnect that is even more profound. The US dollar has been falling alongside the slide in the value of bonds, which in turn has sent yields rising. A 2 per cent fall in the greenback over the past two days has been accompanied by stubbornly high and rising long-term bond rates.

On Friday morning, the US 10-year rate was hovering around 4.42 per cent – well above this week’s low of 3.8 per cent – while the 30-year rate is around 4.9 per cent. This is emblematic not of the world’s safest and most trusted market but of an emerging market caught up in a capital retreat.

We did see an emerging market-style blow-up in the United Kingdom back in October 2022 when then-prime minister Liz Truss’s ill-fated budget triggered a cascade of selling in long-term UK gilts.

But this is the US, the home of the global reserve currency.

“It is highly abnormal for the US: there are only four other episodes in the last 30 years in which the dollar depreciated more than 1.5 per cent with the 30-year yield up more than 10 basis points,” according to analysts at Evercore, a New York investment bank.

Those four include the aftermath of the global financial crisis in February 2009, the European sovereign debt crisis of October 2011, the 2013 taper tantrum and November 2016, when Trump was first elected.

There are sound reasons for US bond yields to rise.

If global growth slows, but tariffs keep prices high, interest rates cannot come down. This is the dreaded stagflation scenario.

But those higher interest rates usually attract yield-seeking investors. Not this time. US bonds and the US dollar are falling in what appears at the surface to be a global retreat of foreign investors.

After a volatile Asian trading session on Wednesday, Westpac financial markets strategist Martin Whetton felt as if history and markets had lurched into a paradigm. “The ultimate risk-free curve of US treasuries, the ‘golden collateral’, the actual instrument any investor from Tennessee to Tokyo can buy, is being challenged,” he told clients. “That money did not scramble to secure US dollar funding, via the basis markets, to buy Treasuries and the US dollar for safety, is startling and a sharp warning,”

Increasingly, macro investors are pointing to a buyer strike amid a loss of faith in the US.

“US exceptionalism went out the window a long time ago. Now it is a question of if people fear US assets,” Jens Nordvig, the founder of research firm Exante, told The New York Times. “If they can do these extreme restrictions on trade, even with the closest allies, can they do restrictions on capital flows as well? Nobody knows. There is no limit here.”

Theories are swirling about who is selling their US bonds. The highly leveraged hedge fund community – must surely be a contributing factor. They’re an increasingly influential marginal buyer and seller of treasuries, and whipsawing markets always weaken their hands.

Some suggested China may have been dumping some of its $US700 billion of US bonds, while others believed it was in fact Japan, a country that sits on more than $US1 trillion of US bonds. Are foreign sellers dumping their bonds to weaken the US, or have they just decided there’s too much risk?

“Trump needs to back away from tariffs to allow foreigners to earn dollars to buy treasuries, or needs to balance the budget by raising taxes, and cutting benefits,” said Russell Clark of Brumby Capital, a macro-focused fund.

“As he expressly promised to not do either of these things – I suspect we continue to see the US treated as an emerging market. And that means all US assets look suspect – just like a classic emerging market crisis.

...Shapiro is one of my most respected home-grown investigative...

Featured News

Featured News

The Watchlist

P.HOTC

HotCopper

Frazer Bourchier, Director, President and CEO

Frazer Bourchier

Director, President and CEO

SPONSORED BY The Market Online