North Channel Investments

A Small-Cap Mining Company That Is Worth Taking A Look At

Mar. 13, 2018 9:53 AM•CPPMF

Summary

Copper Mountain produced record earnings in 2017.

Strong growth prospects from the newly acquired Altona Mining Ltd. This company has a large undeveloped mining site in Queensland, Australia.

Shareholders still need to vote to approve the Altona acquisition. While it is possible it may be denied, both sides would benefit significantly from the merger.

Low valuations in comparison to other mining stocks of similar market caps.

The Altona merger could double Copper Mountain's revenues, and significantly increase their stock value.

Introduction

In early December, North Channel Investments published an article which discussed Copper Mountain Mining Corp. This article gave an overview of the company and discussed their valuations, growth prospects, and recent financial performance.

Copper Mountain recently released their 2017 fiscal year financial statements, which displayed that 2017 was an excellent year that resulted in record adjusted earnings per share. While Copper Mountain’s stock value has not increased over the last few months, there are several reasons why investors should still consider this stock. The company is currently waiting on shareholders to vote on the acquisition of Altona Mining. If this vote is approved, the company could double their revenues over the next few years.

Today’s North Channel Investments article will look at Copper Mountain Mining Corp. This article will analyze their recent financial statements, growth prospects, and current financial valuations. At the end of the article we will provide our thoughts on Copper Mountain.

Advertisement

Business Overview

Copper Mountain Mining Corp. (OTCPK:CPPMF), is a mid-sized Canadian mining company that is based out Vancouver, British Columbia. Copper Mountain produces copper, gold and silver from their mining locations. Copper Mountain has two large operations. The first of the two is the Copper Mountain Mine itself that is located in southern British Columbia. Copper Mountain owns 75% and the other 25% is held by Mitsubishi Materials Corp. Mitsubishi is one of Copper Mountains largest purchasers, where they purchase almost all of the metals produced in the Copper Mountain Mine. This open-pit mine has three main pits on the location and as of Jan 1,2018, had an expected useful life of 16 years.

The second mining location is called the Cloncurry Copper Project and is owned by Altona, a company that Copper Mountain announced that they would acquire (but it based on shareholder approval). This location is an undeveloped open pit that is located just outside of Queensland, Australia, which is a friendly mining jurisdiction. This pit has an expected life of 14 years, and has a measured and indicated mineral resource of over 2 billion pounds of copper, plus an additional 1.6 million pounds of copper in inferred resource. This project is also very large, where Altona owns 3,970 sq km of land.

Recent Financial Performance

2017 was a very strong year for Copper Mountain. The company grew their revenues significantly, which grew to $304.1 million, up from $278 million the year before. This was due to higher amounts of mined minerals and increased value in copper. When all of the resources were milled, the company actually produced less minerals than in comparison to 2016. Copper, gold, and silver production were all down from the year before. While this may have been the case, the company benefited from higher mineral prices which allowed the company to see revenues that were higher than 2016.

Source: 2017 Year End Conference Call (February)

Copper Mountain also saw lower cost of sales than in comparison to the year before, which helped the bottom line strengthen in comparison to 2016. All of these aspects allowed the company to see an adjusted EPS of $0.27 in 2017. This was significantly better than the year before, where the company saw an adjusted EPS loss of $0.09. Diluted earnings per share were $0.35 in 2017, which were much better than the $0.06 earnings that the company saw the previous year (2016). This also the highest diluted EPS that the company has posted in their existence (since 2006).

Source: 2018 Corporate Presentation – Copper Mountain

Other positive aspects of their recent financial statements include their increased current ratio, their increased cash on hand, and their accumulated deficit that continues to decrease. Their cash on hand is up to $45.3 million, a ~$13.7 million dollar increase. Their current ratio is back up to over 1 at 1.05 in comparison to the .99 that it was at the end of the year in 2016. Probably the biggest standout is their accumulated deficit, which now sits at roughly $25.7 million. At the end of 2016, the company sat at an accumulated deficit of ~$73.7 million. Based on their growth prospects, which I will discuss in a moment, the company could see a positive retained earnings within the next few years or so. Overall, not a bad year for Copper Mountain.

Growth Prospects

Most of Copper Mountain’s growth prospects lie within the tentatively acquired Cloncurry Copper Project. This mine is expected to produce 80 million pounds of copper per year as well as 17,000 ounces of gold per year. The Cloncurry Project is very similar to their Copper Mountain mine, making this acquisition a very doable task. Copper Mountain has a goal to reach 200 million pounds of copper production per year. In 2017, Copper Mountain produced 75.8 million lbs of copper from their mine and is expected to produce 75-85 million lbs/year over the next few years. The Cloncurry acquisition will aid in that goal, where it will add another 80-85 million lbs/year when working at full capacity. Both mines would contribute a total of roughly 150-170 million lbs of copper a year. This acquisition should allow the company to double their revenues once the Cloncurry mine is fully operating.

Source: 2018 Corporate Presentation

The Cloncurry Project also has other geographical benefits. The location is fairly close to rail, roads, local smelters, refineries, and ports. The area also has a strong skilled workforce. These will allow the Cloncurry Project to keep costs low, where cash costs per unit of copper is expected to be $1.65 (US). This estimated cash costs for a pound of copper within Copper Mountain was $1.74, meaning both will see very similar profitability. The mines expected output is a combined 3.6 billion tonnes of copper between inferred and confirmed resources and should allow Copper Mine to see steady revenues for years to come.

That being said, Copper Mountain and Altona shareholders will need to vote in order for the acquisition to be made possible. Both companies have also refrained from putting a firm date on when mining operations were expected to begin in the Cloncurry Mine. I attempted to get some answers, where I emailed Copper Mountain’s investor relations to get a better sense of expected dates. I recieved the following response:

“The voting by both Company’s shareholders will be completed March 26, 2018 as to whether the transaction moves forward. We are currently working on a bankable feasibility study, which should be completed by June. The production decision by the board will follow.”

This means that if the acquisition is voted through, investors will be waiting some time before the Cloncurry mine begins to produce. While this may be the case, investors still have a few reasons to invest in Copper Mountain right now regardless of shareholder approval. The company is currently completing drilling programs and engineer studies that will aim to determine additional copper supplies in the Ingerbelle resource (portion of the Copper Mountain mining location). If these studies are determined correct, Copper Mountain’s useful life will increase by 10 years.

As we all know, mineral prices can often positively or negatively affect mining companies. 2016 was year of struggles, were copper prices on average throughout 2016 were $2.19 (US) per pound. Currently, copper prices are much stronger. As of markets closing on March 7, 2018, copper stood at $3.12 per pound. Evidently, Copper Mountain’s revenues will be affected by the market. Good news is that copper is a mineral that is of increasing demand. China consumes over half of the global copper production and are expected to increase their demand in coming years. Electric Cars, major appliances, and cell phones are all common items that use copper. Demand for these products are growing, and manufacturers will continue to require copper.

Source: Copper Mountain 2018 Corporate Presentation

Going further, Copper Mountain is also going to continue to look for acquisition opportunities as well as attempt to find new methods to maximise productivity and minimize costs. While these are all simply just the company stating their goals, I expect that they will find ways to do so. This expectation is backed up by the fact that the company cut their operating costs in 2017 in comparison to the previous year. Operation costs in 2017 were cut while actually extracting more pounds of unrefined minerals from the ground. Overall, Copper Mountain is headed in the right direction and prospective investors should be fairly impressed with where the company is headed regardless of the Cloncurry Mine Project.

Why is now the time to buy this stock?

Despite the fact that shareholders still need to vote on the merger, I find it very hard to believe it will get denied. This merger would benefit both parties, and Copper Mountain’s management made the benefits very clear in their 2017 year-end presentation. Seen below is a slide from the presentation that states the benefits for both companies.

Source: 2017 Altona Acquisition Presentation

Some of the notable benefits would be increased cash flows within the immediate and long term, as well as Altona benefiting from Copper Mountain’s experience. Copper Mountain is an open pit mining site, which will be very similar to the operations in Cloncurry. Altona shareholders would also receive a premium on their shares in exchange for Copper Mountain shares, which is another bonus for Altona shareholders. I would be very, very surprised if this deal did not go through based on the fact that there are significant bonuses on both sides if they merged.

Based on the fact that it is unclear when operations will begin at Cloncurry, it is very difficult to make an assumption as to what changes we will see in Copper Mountain’s profits in the short run. In the short run, the company may post lower earnings as the Cloncurry project will pay out more than they earn in the first year or so as they get up and running. That being said, if you are considering Copper Mountain, you should buy for the future.

Source: 2017 Altona Acquisition Presentation

Copper Mountain is expected to produce another roughly 80 million pounds of copper in 2018, with or without the Cloncurry Project. This is very similar to what the annual production is expected to be from Cloncurry. With both mines at optimal production, Copper Mountain would produce 155-170 million pounds of copper a year,~40,000 oz of gold between both mines, as well as the 200,000+ silver from the Copper Mountain Mine. Copper prices are expected to stay very similar over the next few years, where they are estimated to increase annually by 1.8%.With all of this in mind, a rough (but conservative) estimation of their potential earnings is as follows:

Total Estimated Revenue = USD$551 million per year X 1.20 (Exchange rate of Canadian dollar) = CAD$661.2 million

- Copper - 160 million lbs X 3.10/lb = $496 million USD

- Gold is currently around $1,300/oz X 40,000 = $52 million USD Gold forecasts vary over the next few years, however the median throughout appears to be 1,300/oz.

- Silver is currently around $15.00/oz X 200,000 = $3.0 million USD Silver Forecasts vary, but are expected to decrease after 2022.

Operating income was roughly 16% of their revenues which was lower than their adjusted earnings due to gains on foreign exchange. Although simplistic, applying this income ratio forward would give Copper Mountain $105.8 million dollar net income per year. With the merger, the company is expected to have roughly 187.6 million outstanding shares. This would be an average EPS of $0.57/year. Their diluted EPS for 2017 was 0.35, that is a ~62% increase.

Source: 2017 Altona Acquisition Presentation

Keep in mind this is a very conservative and basic concept of how I predicted earnings. That being said, the demand for copper is expected to continue due to China’s copper needs. Copper is their main revenue, where the mineral price should stay very solid for years to come.

This estimation is also something that I would expect once the mine is running at optimal performance at both locations. Chances are that this would not happen until 2020 or later. Regardless, Copper Mountain has the ability to grow their earnings and their operations significantly with the acquisition of Altona.

Comparison Against Competitors

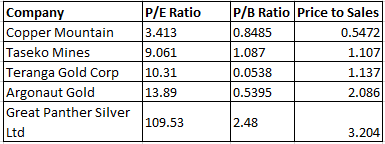

Next, I will compare Copper Mountain to other similar, small market-cap mining stocks. This gives investors an idea of where Copper Mountain’s valuations currently stand against other companies in the sector. All data was taken as of markets closing on March 12, 2018. The chart is seen below:

Source of Data: YCharts

This chart concludes that Copper Mountain’s ratios are very low when compared to other mining peers. Their price to sales ratio & PE ratio are all lower than other competitors. Their PB ratio is also slightly under the group average. Copper Mountain’s low valuations seem to suggest that the company is currently undervalued.

One of the reasons why I believe they are currently undervalued is the fact that investors are waiting on the outcome of the shareholder voting, which will take place on March 26, 2018. While it is possible that it could be voted down, I can’t see it happening as the merger would benefit both shareholders and both companies. My expectation is that once the vote gets approved. Copper Mountain’s share value will increase due to increased confidence in the company’s future.

Final Thoughts

Copper Mountain has several aspects that make them an attractive investment. Their low valuations, respectable growth prospects and their strong 2017 performance indicate that the company is headed in the right direction. Investors should consider all risks within this stock, as the company’s revenues are highly dependent on mineral prices. That being said, the demand for copper should continue to be strong going further as it is a material that is needed in a plethora of consumer and commercial products. Investors should be patient with the Cloncurry Project, where high expenses within the first few year or so due to expansion and development of the mine will cut into profit margins. That being said, the acquisition of Altona will allow Copper Mountain to grow their revenues and their earnings in the long run, where I expect earnings will be significantly higher than what they are today. In the long run I see Copper Mountain moving toward the sector’s average in valuations, where their PE will be closer to 8-10. Copper Mountain’s stock currently sits at $1.20 CAD. From the research I have done, various experts of various websites have estimating Copper Mountain’s price will increase to $1.60-$1.80. I think this very realistic in the short run (over the next year or so). In the long run, the stock price will receive another significant boost after 2019 once Cloncurry is running at full steam. In the long run, if the company earnings an adjusted EPS of $0.40 at a conservative PE of 6, that’s double the stock price that it is today.

On the other hand, if Cloncurry flops, the company still has growth prospects within their own operations. Copper Mountain is still an undervalued company, and I expect management to search for other acquisition opportunities going forward if Altona doesn’t pan out. Overtime, their stock value should increase and investors will be rewarded.

To conclude, there is huge speculation within this stock, and there is definitely some risk. For some who want to play it safe, waiting for the shareholder voting results is not a bad idea. Regardless of how you play it, Copper Mountain has great potential ahead, and the Cloncurry Project could lead to significant gains for investors and the company. That being said, if you do invest…be patient with their performance. The Cloncurry Project will take a short amount of time before it is at optimal performance, but investors will need to stick around to see excellent rewards. To conclude, Copper Mountain should be considered by investors. Keep an eye on March 23. This Copper mining stock could allow you to strike gold.

Clickk here to read our previous Copper Mountain article.

Note: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in CPPMF over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Copper Mount and Altona.

-

- There are more pages in this discussion • 26 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)