Reading time: 4 minutes

Fears around the coronavirus have gripped markets over the past few weeks, causing the biggest one-week drop on Wall Street since the financial crisis. Last week we also saw the fastest Wall Street “correction” (i.e. 10% decline from previous peak) in history.

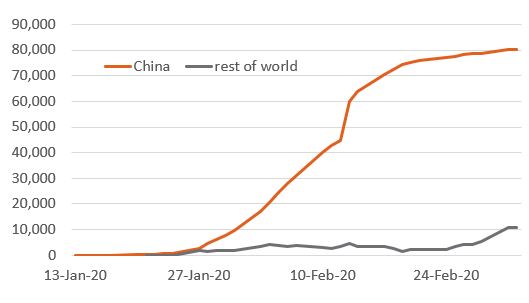

Are markets over-reacting? It’s hard to be certain, as while the coronavirus outbreak appears to have stabilised in China, the risk is that it may yet wreak havoc in other major centres of global economic activity – Europe and the United States – over coming weeks.

Coronavirus cases: China vs. Rest of world

Source: John Hopkins CSSE

Indeed, uncertainty stems from the fact the coronavirus remains distinct from the pattern of past influenza outbreaks that have afflicted the world.

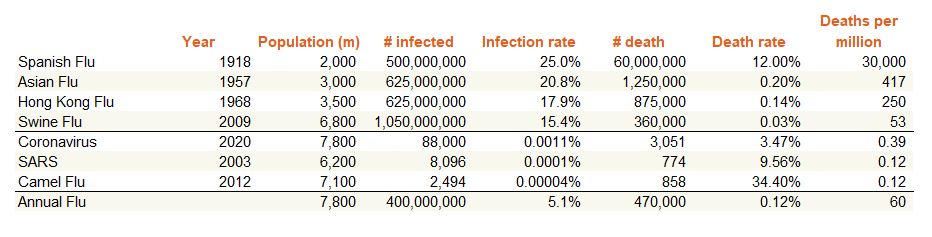

With a death rate among those infected currently around 3%, the coronavirus is somewhere between the 2003 SARS outbreak and 2009 swine flu outbreaks in terms of lethality, which had death rates of 10% and 0.03% respectively.

While the more lethal SARS outbreak ended up infecting a relatively tiny 8,000 people worldwide, the swine flu affected around 1 billion, or 15% of the world’s population. SARS was not labelled a “pandemic” by the World Health Organisation, whereas swine flu was.

The table below shows infection and death rates for major disease episodes of the last 100 years. The Spanish flu of 1918 combined extremely high infection and mortality rates to produce a huge number of deaths. Other outbreaks have had either high infection rates or high mortality rates, but have managed to avoid the catastrophic combination of the two.

For context, the common annual flu affects around 400 million (5%) of the global population each year, with a death rate of around 0.1% (500,000 people) each year.

History of Past Influenza Outbreaks

Source: WHO

Given the reasonably high coronavirus death rate, the hope is that global infection rates remain much closer to that of SARS than the 2009 swine flu and common annual flu.

Another possibility is that the fatality rate ends up being much lower than currently evident – closer to swine flu – if allowance is made for many milder cases going unreported.

For markets, what matters especially now is how bad conditions become in the world’s most important economy, the United States. While the U.S. had 6% (60 million) of worldwide swine flu cases, it had only 0.3% (27) of SARS cases. But even the 2009 swine flu outbreak ended up not as bad as feared in the U.S. and failed to derail the post-GFC rebound in both its economy and stockmarket over the year.

Indeed, the World Health Organisation was criticised for creating undue fear in 2009, which perhaps explains its reticence to date in labelling the coronavirus a pandemic.

At the time of writing, the U.S. had only 118, or 0.1%, of coronavirus cases. Again, we can only hope the U.S. outcome is closer to that of SARS than of swine flu.

Either way, economic data around the world is likely to be universally bad in coming weeks as production and tourism are disrupted. China’s weekend PMI reports on both manufacturing and services were shocking (composite PMI covering both services and manufacturing sank to 28.9!).

Trying to help will be central banks, with the Fed this week announcing an emergency 50bps cut. The RBA also cut rates by 0.25% this week.

The RBA will cut rates to get ahead of the likely slump in both business and consumer confidence in the months ahead. A follow-up rate cut in May is now anticipated, with “quantitative easing” now at least a 40% chance in the second half of the year.

Will local rate cuts hurt rather than help confidence? Perhaps. But in a time of apparent crisis, the RBA will want to feel ahead not behind the curve. Indeed, Australia now faces its greatest risk of recession since the global financial crisis, with private demand already weak, and with much less fiscal and monetary firepower to respond.

In my view, the Federal Government needs to seriously consider an economic statement, outlining further stimulus measures before the May Budget.