The Economist

Electrifying everythingAfter electric cars, what more will it take for batteries to change the face of energy?

No need for subsidies. Higher volumes and better chemistry are causing costs to plummet

Print edition | Briefing

Aug 12th 2017| SAN DIEGO AND SUNDERLAND

ABOUT three-quarters of the way along one of the snaking production lines in Nissan’s Sunderland plant, a worker bolts fuel tanks into the chassis of countless Qashqais—the “urban crossover” SUVs which are the bulk of the factory’s output. But every so often something else passes along the line: an electric vehicle called a Leaf. The fuel-tank bolter changes his rhythm to add a set of lithium-ion battery packs to the floor of the Leaf. His movements are so well choreographed with the swishing robotic arms around him that he makes the shift from the internal combustion engine to the battery-charged electric vehicle look almost seamless.

Until recently, it was a transition that many found unthinkable. The internal combustion engine has been the main way of powering vehicles on land and at sea for most of the past century. That is quite the head start. Though Leafs are the world’s biggest-selling electric vehicle, the Sunderland plant, Britain’s biggest car factory, only made 17,500 of them last year. It made 310,000 Qashqais. And the Qashqais, unlike the Leafs, were profitable. Nissan has so far lost money on every Leaf it has made.

Latest updates

See all updates

- Where Britons go on holiday

GRAPHIC DETAILAN HOUR AGO- Juha, the Middle East’s heroic everyman

PROSPERO3 HOURS AGO- Justice Kennedy will take centre stage during the Supreme Court’s upcoming term

DEMOCRACY IN AMERICA5 HOURS AGO- The e-mail Larry Page should have written to James Damore

INTERNATIONAL5 HOURS AGO- A dodgy dam in Canada’s east

AMERICAS8 HOURS AGO- Why Republicans will find it hard to cut taxes

THE ECONOMIST EXPLAINS10 HOURS AGO

There were 750,000 electric vehicles sold worldwide last year, less than 1% of the new-car market. In 2011 Carlos Ghosn, boss of the Renault-Nissan alliance, suggested that his two companies alone would be selling twice that number by 2016, one of many boosterish predictions that have proved well wide of the mark. But if the timing of their take-off has proved uncertain, the belief that electric vehicles are going to be a big business very soon is ever more widely held. Mass-market vehicles with driving ranges close to that offered by a full tank of petrol, such as Tesla’s Model 3 and GM’s Chevrolet Bolt, have recently hit the market; a revamped Leaf will be unveiled in September. The ability to make such cars on the same production lines as fossil-fuel burners, as in Sunderland, means that they can spread more easily through the industry as production ramps up.

All we need to live today

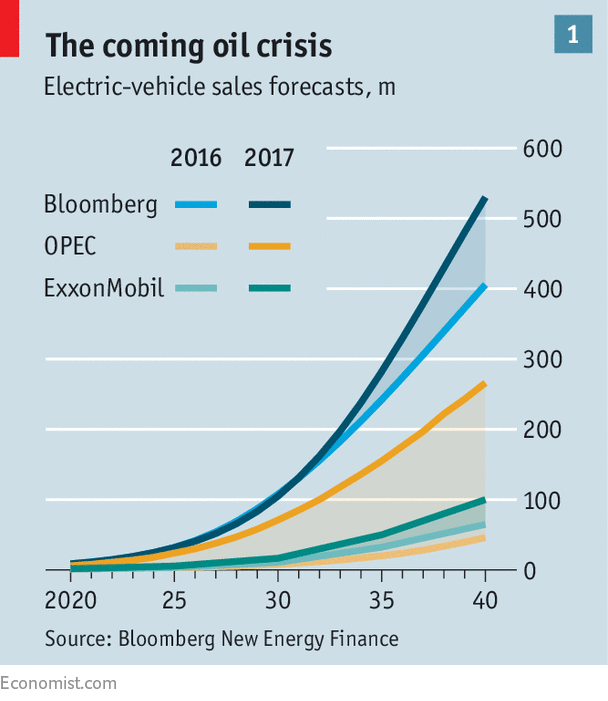

Many forecasters reckon that the lifetime costs of owning and driving an electric car will be comparable to those for a fuel burner within a few years, leading sales of the electric cars to soar in the 2020s and to claim the majority sometime during the 2030s. China, which accounted for roughly half the electric vehicles sold last year, wants to see 2m electric and plug-in hybrid cars on its roads by 2020, and 7m within a decade. Bloomberg New Energy Finance (BNEF), a consultancy, notes that forecasts from oil companies have a lot more electric vehicles in them than they did a few years ago; OPEC now expects 266m such vehicles to be on the street by 2040 (see chart 1). Britain and France have both said that, by that time, new cars completely reliant on internal combustion engines will be illegal.

That this is even conceivable is a tribute to the remarkable expansion of the lithium-ion battery business—and to the belief that it is set to get much bigger. The first such batteries went on sale just 26 years ago, in Sony’s CCD-TR1 camcorder. The product was a hit: the batteries even more so, spreading to computers, phones, cordless power tools, e-cigarettes and beyond. The more gadgets the world has become hooked on, the more lithium-ion batteries it has needed. Last year consumer products accounted for the production of lithium-ion batteries with a total storage capacity of about 45 gigawatt-hours (GWh). To put that in context, if all those batteries were charged up they could provide Britain, which uses on average about 34GW of electricity, with about an hour and 20 minutes of juice.

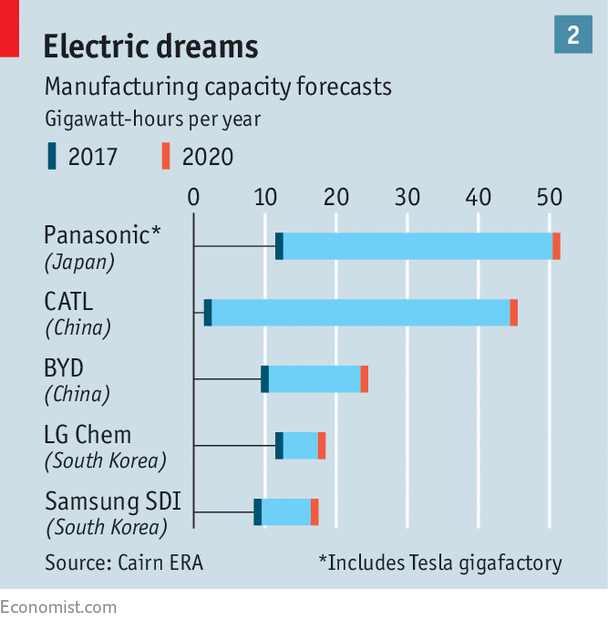

In the same year production of lithium-ion batteries for electric vehicles reached just over half that capacity: 25GWh. But Sam Jaffe of Cairn ERA, a battery consultancy, expects demand for vehicle batteries to overtake that from consumer electronics as early as next year, marking a pivotal moment for the industry. Huge expansion is under way. The top five manufacturers—Japan’s Panasonic, South Korea’s LG Chem and Samsung SDI, and China’s BYD and CATL—are ramping up capital expenditure with a view to almost tripling capacity by 2020 (see chart 2). The vast $5bn gigafactory Tesla is building with Panasonic in Nevada is thought to already be producing about 4GWh a year. Tesla says it will produce 35GWh in 2018. Just four years ago, that would have been enough for all applications across the whole world.

The gigafactory is not just for cars. Hearing of electricity blackouts in South Australia, Elon Musk, Tesla’s founder, tweeted to the state’s premier in March that by the end of the year Tesla could provide enough battery storage to make sure that the grid never fell over again. At the gigafactory they are now hard at work cramming 129 megawatt-hours (MWh) of capacity into a facility designed to keep their boss’s word. When installed on the other side of the Pacific, it will be the biggest such grid-based system in the world; but many more are on the way. Industrial-scale lithium-ion battery packs—essentially lots of the battery packs used in cars wired together, their chemistry and electronics tweaked to support quicker charging and discharging—are increasingly popular with grid operators looking for ways to smooth out the effects of intermittent power supplies such as solar and wind. Smaller battery packs are being bought by consumers who want independence from the grid—or, indeed, to store the electricity they produce for themselves so that it can be sold into the grid at the most lucrative time of day or night. Batteries are becoming an integral part of the low-emissions future.

The chance to change

The fundamental operating principles of the lithium-ion battery are easily understood. When the battery is charging an electric potential pulls lithium ions into the recesses of a graphite-based electrode; when it is in use these ions migrate back through a liquid electrolyte to a much more complex electrode made of compounds containing lithium and other metals—the cathode. The fundamental operating principles of the battery business, on the other hand, are considerably more opaque, thanks to an almost paranoid taste for secrecy among suppliers and the baffling economics of the Asian conglomerates that lead the market.

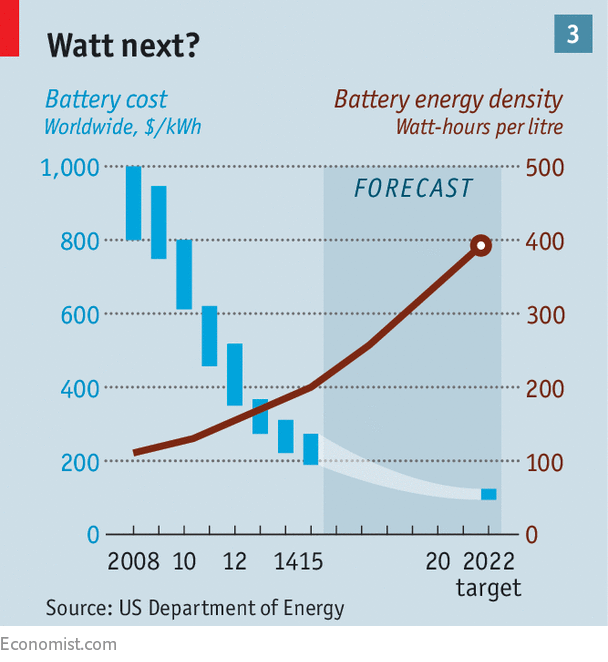

All the big producers are adding capacity in part because it drives down unit costs, as the past few years have shown (see chart 3). Lithium-ion cells (the basic components of batteries) cost over $1,000 a kilowatt-hour (kWh) in 2010; last year they were in the $130-200 range. GM says it is paying $145 per kWh to LG Chem for the cells that make up the 60kWh battery for the Bolt (the pack, thanks to labour, materials and electronics, costs more than the sum of its cells). Tesla says that cells for the Model 3 are cheaper. Lower costs are not the only improvements; large amounts of R&D investment have led to better power density (more storage per kilogram) and better durability (more discharge-then-recharge cycles). The Bolt comes with a battery warranty of eight years.

But getting prices down this way has not just produced cheaper, better batteries. It has also resulted in significant overcapacity. Cairn ERA estimates that last year the manufacturing capacity for lithium-ion batteries exceeded demand by about a third. Both it and BNEF say that the battery manufacturers are either losing money or making only wafer-thin profits on every electric-vehicle battery they produce. Despite the seeming glut, though, they all have plans to expand, in part to drive prices even lower. Mr Jaffe explains their thinking as that of the “traditional Asian conglomerate model”: sacrificing margins for market share. This may be a sound strategy given the ever-greater hopes for electric vehicles in the near future. But at the moment it is also one that looks rather unnerving. Although Mr Jaffe believes that increased demand for both electric vehicles and stationary storage will justify the rush to expand, he accepts that, for now, “It feels like a gold rush—but there’s no gold.”

There are, though, other valuable metals in the picture. Making more batteries means acquiring more lithium, as well as various other metals, including cobalt, for the cathodes. These make up about 60% of the cost of a cell. Being assured of a constant supply of them is as much a strategic consideration for battery-makers as mastering electrochemistry. Since 2015 lithium prices have quadrupled, says Simon Moores of Benchmark Mineral Intelligence, a consultancy. Cobalt’s price has more than doubled over the same period; prices of chemicals containing nickel, also used in cathodes, are rising too.

New supplies of lithium should not be too hard to find; there are thought to be at least 210m tonnes of the stuff, says Mr Moores, compared with current annual production of 180,000 tonnes. New fields are being opened up. In July SQM of Chile, the world’s biggest lithium producer, said it would invest $110m in a lithium joint venture in Western Australia. Cobalt is more tricky. Not only are supplies scarcer, but a lot comes from the Democratic Republic of Congo. This raises both ethical problems (production can rely on child labour) and business ones (no one wants to depend on warlords for a vital resource). LG Chem has said it is trying to reduce the cobalt component of its battery cells, while continuing to improve their performance. Further down the road, recycling the metals from old batteries could make the industry much more sustainable.

One of the reasons manufacturers are confidently piling on capacity despite costlier raw materials is that, at the moment, little else can compete with their wares. Other battery technologies that sound as if, in principle, they might have advantages are often touted—but none of them enjoys the decades of development that have turned lithium-ion devices from an intriguing idea into a dominant technology. This work has generated a huge amount of knowledge about the fine details of manufacturability, the choice of electrolytes and the ever more sophisticated nanotechnology of the metallic cathodes.

Kenan Sahin, who heads CAMX Power, an American company that supplies materials for cathodes, says the lithium-ion battery’s cost and weight, its ability to charge and discharge repeatedly, its durability and its safety have all been achieved through an endless process of fine-tuning, rather than eureka moments. He likens battery chemistry to drug discovery in the pharmaceutical industry. “It’s really difficult. Whatever you have needs to work at large scale and the side-effects have to be acceptable,” he says. This is all hard for a would-be usurper to emulate. For the foreseeable future, ever-improving lithium-ion technology—perhaps with new solid electrolytes—will make the running, benefiting from yet more refinements the more applications it supports.

Until now, the mainstay has been a cylindrical cell called the 18650, which looks like a rifle shell. It is 65 millimetres long, 18mm in diameter and has an energy density of perhaps 250 watt-hours per kilogram. (The energy density of petrol, for comparison, is about 50 times greater; but the cell can store that much energy hundreds or thousands of times.) Tesla and Panasonic have now developed the 2170, a bit longer and wider; Mr Musk says it will be the most energy-dense battery on the market. The company says that the cost of driving a Model 3, released in late July to rave reviews, will be half that of any of its previous vehicles. At the car’s launch Mr Musk seemed a bit overawed at the prospect of producing 500,000 such vehicles next year: “Welcome to production hell,” he told the assembled workers.

On August 7th Tesla announced plans to sell bonds worth $1.5bn to support its expansion, giving a badly needed breather to the equity market, where it usually raises cash (and where its value has risen by two-thirds over the past year). The company has said that it has 455,000 pre-orders for the Model 3, which, if taken up, would generate enough cashflow by year-end to start shoring up the company’s finances. If it all goes to plan, Mr Musk hopes to see the gigafactory become the largest building in the world, cranking out 100GWh a year—and to be joined by further gigafactories elsewhere; the next would probably be in China.

All this presupposes that electric vehicles really are poised for take-off. There is no doubt that they are getting better and cheaper. But there are other constraints on their use, most notably charging. In Britain 43% of car owners do not have access to off-street parking and thus would not be able to charge cars at home. Nor are domestic supplies always up to the strains of, say, an 11kW charger; using the kettle or immersion heater during the six hours it would take to charge up a 90kWh battery could blow the fuses. The answer will be fast-charging stations, possibly like petrol stations; some car companies are beginning to build them as a way to assuage the “range anxiety” that turns some drivers off electric vehicles. Whether such facilities can expand fast enough to allow the industry’s expansive ambitions to be fulfilled remains an open question.

This uncertainty about the speed at which electric-vehicle usage will grow is one of the things that makes stationary storage an attractive alternative market for the battery-makers. Installations such as the one recently built in a nondescript lot on the outskirts of San Diego, California, by San Diego Gas & Electric (SDGE) have none of the glamour of glistening new models hitting showrooms. It is a 384,000-cell car battery impersonating a trailer park: the dullest Transformer ever. But its ordinariness is part of its beauty, says Caroline Winn, chief operating officer of SDGE; the utility uses it to offer power at times of peak demand. Modular construction meant the 120MWh facility—just a touch smaller than the one Tesla has promised South Australia—was ready to go only eight months after the start of the project. It runs so quietly it is hardly audible. Building a gas turbine to do the same job would have been cheaper but would have taken years, in the unlikely event that local residents had given it the go-ahead in the first place. The battery facility “is a lot prettier than a gas turbine,” Ms Winn says.

The final source of energy

For Tesla and other big battery-makers grid-storage projects are the most attractive part of the electricity market; they offer contracts that use up otherwise surplus capacity in satisfyingly large job lots. But there is also demand for batteries to go “behind the meter”. Tesla serves this market with its Powerwall domestic battery pack, designed to complement the solar panels and solar tiles it offers. Nissan, too, is looking at behind-the-meter applications. It is working with Eaton, an American power-management company, to put “second-life”, or partially used, Leaf batteries into packs that can provide businesses and factories with back-up power, thus replacing polluting diesel generators. The first big customer is the Amsterdam Arena, home to AFC Ajax, a football club.

Such systems do not necessarily compete on price; but governments are providing various incentives for them. In May the New York State regulator gave Con Edison, a utility, the right to allow business customers to install batteries in Brooklyn and Queens to export electricity to the grid. New York, with a rickety grid that dates back over a century to the days of George Westinghouse and Nikola Tesla, is struggling to integrate more renewable energy into its supplies, and storage offers it a new way to manage peak power demand. Jason Doling, a state energy official, says the programme should be ideal for high-rise blocks; powering lifts from the battery in mornings and evenings when electricity prices are highest would be a boon.

The New York fire department remains concerned that lithium-ion batteries in buildings pose a fire hazard, however. When they are being installed, it keeps its engines on standby. As the externally combusting fiasco of Samsung’s Galaxy Note 7 smartphones reminded the world last year, lithium-ion batteries can, if badly or over-ambitiously designed, short circuit in incendiary ways. In general, however, new materials and ceramic coatings for electrodes have made the batteries for cars very safe.

Setting aside concerns about combustion, companies that install batteries for behind-the-meter storage, and indeed for grid storage, say they are hampered by outdated regulation and by insurance problems. This limits the funding available to them, according to Anil Srivastava, who runs Leclanché, a Swiss battery-producer. They also need to find ways to make stationary storage pay. Sometimes, as in San Diego, it is pretty much the only solution to the demands of a regulator: the California Public Utilities Commission was worried about blackouts in Los Angeles in the wake of a leak at the Aliso Canyon gas-storage facility in 2015. When price is more of an object, the batteries need to find more than one service to provide, a procedure known as “revenue stacking”. For example, a system might be designed to offer power to the grid for short-term frequency regulation as well as providing a way of dealing with peak demand.

It sounds complicated. But finding more than one way to sell the same thing is second nature in the battery business, as it fine-tunes its wares for every market and every scale. And though today’s exuberance may look a little scary, in the long run that ability looks likely to see the industry do very nicely indeed.

This article appeared in the Briefing section of the print edition under the headline "Electrifying everything"

You’ve seen the news, now discover the story

Get incisive analysis on the issues that matter. Whether you read each issue cover to cover, listen to the audio edition, or scan the headlines on your phone, time with The Economist is always well spent.

Enjoy 12 weeks’ access for £12

View comments

Reuse this content

Add to My Watchlist

What is My Watchlist?