Believe there is an potential rerating story in DRA beginning over the next few weeks and months with increases in gold prices, steady medium term improvement in production, exploration potential, upcoming asset sale and low valuation compared to peers.

Figures, ramblings and some charts below.

Stats

737M shares 8.3c sp $11.8M cash and gold $11.7 Con notes EV ~A$61M

Unhedged Gold producer Estimated cash flow for 2010 before development expenses ~US$35M Directors added 1.2M shares early May 22000m of drilling to extend life Svartliden and other projects Undervalued based on Ev/oz and cash flow No resources tax

Asset sale details,

20% of Zara project can be bought by CHN for a total of $16.2M in stages, this comprises of:

$8M cash and 2M shares by 30th June 2010 to buy DRAs 20% share. CHN have indicated they will exercise this option from their qtr report. See

In addition and not subject to the 20% agreement, CHN need to pay $4M cash on delineation of 1Moz of gold. The current resource stands at 0.944Moz, recent drilling is likely to upgrade this beyond 1Moz mid year according to CHN.

See http://www.asx.com.au/asxpdf/20100331/pdf/31pk4h99g279t2.pdf

Further, CHN need to also pay DRA $3.4M on completion of the BFS.

Therefore if CHN meet these deadlines and targets, DRA will recieve ~$13M late June to July from CHN, or 1.7cps.

The payment would further reduce pressure on DRA's cash flow to fund the con note buy back, development and exploration making investment more attract and lowering current risk profile.

Exploration potential, DRA has focused on development and has just replaced reserves/resources with a few years to spare and then using spare cash flow to pay off con notes. Expect increased cash flow and asset sale cash to be directed to increasing reserve base which will increase valuations by extending current known mine life.

Directors and related parties, Eurogold has continually increased stake in DRA.

Fall in Euro/USD exchange rate should reduce costs coupled with the rise in AUD gold price.

Cons

Extreme cold is likely to effect production and cash costs adversely in winter. 12.5M con notes outstanding valued at $11.7M, DRA is buying these back before the Feb 2011 deadline. Transition phases from open pit to underground mining. Variable grades at Orivesi. CHN will need tsx listing or other additional capital raising to pay the Zara option to DRA, details are not finalised. Gold price and currency movements cut both ways for all producers. Average to moderate cash costs. Revised production profile.

In summary DRA looks to be in a similar position to GRR late last year early this year, unloved poor profile producer but moving steadily out of debt with rising production during a period of increasing product prices. Furthermore expect DRA's average to moderate cash costs will provide very high leverage to increases in the gold price.

Together with the asset sale these features above are what i look for in potential turnaround type companies.

For those not sold on the DRA, would suggest looking at OGC, DOM, MML, AND, PRU and KRM as larger more established producers and exploration companies. Disc: owns shares in AND and OGC.

DRA Chart, 2010 downtrend (yellow) is still holding with 50dma also providing resistance at 8.3/8.4c.

Gold Chart, resistance tested from Nov 2009 highs, expect similar continuation pattern as at US$1000oz with short term consolidation here at highs, see also following goldcorp chart.

Use Goldcorp as they are large, successful, unhedged and still interested in gold mining. Currently testing 2008/09 highs would expect if these levels are broken it would confirm next phase in re-rating of gold sector. Would use current consolidation below these highs ST as a further buying op.

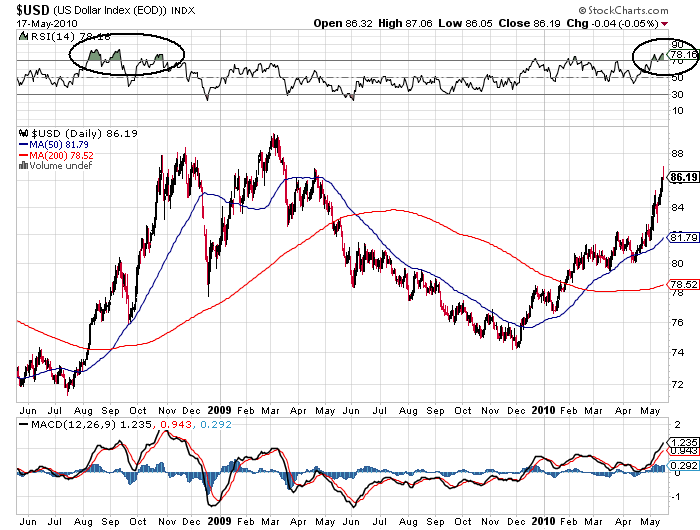

USD- Gold has shown relative strength against the USD, especially during the european debt crisis and correction in markets increasing likehood that a more sustained move in gold is unfolding. USD is now extreme overbought almost to 2008 levels, would not expect gold to travel back with USD.

DRA Price at posting:

83.0¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)