....per Bell Potter latest projection July 2024, LTR would be making $563mil revenue @$1200/MT SC6 price but producing 325MT at a loss of -$58mil. It is strange that they have not downgrade the forecast lithium price as the price assumption is 56% above what is today.

....Should US$770/MT stick for 2025 however, we are looking at -$200mil less in revenue projection and losses could be >-$200 mil for 2025.

....this is the enormity of it for a company with market cap of $1.78B.

....months ago, I provided these metrics to LTR holders, cautioning not to be too enthused over near term production if it was going to be produced at a loss. Question is which route would LTR management take - a) produce at a significant loss OR b) go into C&M. Doing (a) would see a slow train wreck motion stock price and consume cashflow, doing (b) would see a stock price dive but conserve cash.

....LTR hodlers have a narrow timeline to decide.

Nearly 30 percent of lithium producers are losing money, shutdowns likely if prices don’t improve

By Carl Capolingua

Thu 29 Aug 24, 12:08pm (AEST)

Key Points

At Market Index, we pride ourselves in being able to bring you all the latest major broker views on all the key commodities for the Australian share market. One commodity that has particularly captured Aussie investors’ attention over the last few years is lithium. What’s currently playing out in this market appears to be akin to the classic “commodity boom and bust cycle”.

- Most key lithium minerals contracts are down close to 90% since their peak in late-2022 as those same high prices stoked a supply response that flooded the market

- As many as 30% of producers are likely losing money at current prices, a major broker suggests

- We bring you the latest views on lithium from two brokers that both agree further supply cuts are required to rebalance the market

Since Adam was a little boy, commodities have cycled through the following stages:

- Scarcity versus Demand Boom: In lithium’s case, the advent of us needing long life rechargeable batteries in just about every gadget we use in our daily lives, our automobiles, as well as energy storage.

- Demand Boom in Supply Vacuum Triggers Price Boom: Incumbents and early moves make super profits, but high prices also incentives new supply.

- Supply-side Response: All of a sudden, every micro-cap stock on the ASX appears to be switching to looking for this commodity! It’s now super easy to get funding (both debt and equity), and many of them succeed. This brings on new supply, and it hits the market at the same time the incumbents and early moves are ramping up their supply.

- Supply Meets Demand to Rebalance Price: Depending on the supply response, this can be mild, e.g. prices ease off and whilst some higher cost producers might be knocked out of the market, the incumbents and early movers usually continue to do well. Or in the case of lithium, it can be severe – see the chart below!

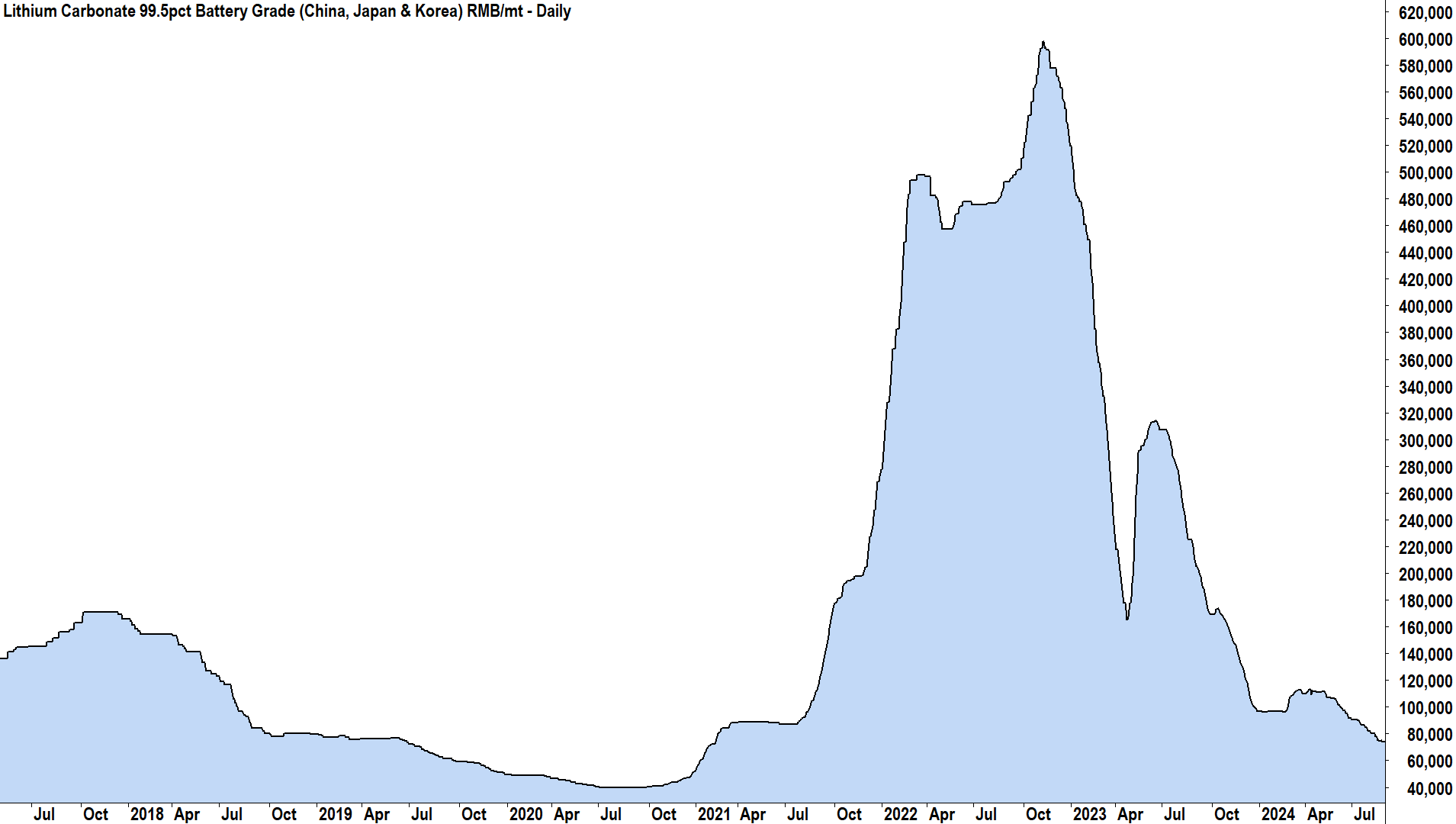

The price of lithium carbonate is down over 87% since its peak in late-2022 (Click here for full size image)

“Lithium Supply Reacting”

In its latest research report on the lithium market titled “Lithium Supply Reacting”, Morgan Stanley suggests that finally the supply side in the lithium market is beginning to react to the current low-price environment – albeit “slowly”.

Many lithium minerals, including the hard-rock “spodumene” variant produced by Australian producers like Pilbara Minerals (ASX: PLS), Mineral Resources (ASX: MIN), IGO (ASX: IGO), Liontown Resources (ASX: LTR), and until recently, Core Lithium (ASX: CXO), must be converted into lithium carbonate before being purchased and used by battery manufacturers. For this reason, lithium carbonate is often considered to be the lowest common denominator in the lithium-battery supply chain.

Morgan Stanley’s research into the Chinese battery industry value chain shows that converter margins are under pressure, and this has triggered a 10% reduction in lithium carbonate production since the end of June.

Apart from this, at the proverbial coal face of supply – major projects are beginning to be curtailed, with the broker pointing out these recent announcements:

“Current prices are starting to cut into the cost curve, raising the likelihood of production cuts” the broker notes. Morgan Stanley predicts that at the current lithium carbonate price of US$9,000/t, it is nearing the 70th percentile of the cost curve. This means that almost 30 percent of existing producers are doing so at a loss.

- Arcadium Lithium (ASX: LTM): Paused investment in its James Bay project, slowed timeline of Argentinean projects, considering idling Mt Cattlin in Australia

- Piedmont Lithium (ASX: PLL): Delayed Carolina project in the USA by 2 years

- Albemarle (NYSE: ALB): Scaled back Kemerton lithium hydroxide refinery operations

Exhibit 1: The lithium price currently sits on the 72nd percentile of the cost curve Source: Company Announcements, Morgan Stanley Research (From “Lithium Supply Reacting”, Morgan Stanley Research, 23 August 2024) (Click here for full size image)

Morgan Stanley notes this pressure on producers is beginning to have an impact – particularly on higher cost supply. In addition to converters scaling back activity, the broker says, China's domestic lithium (lepidolite) production – long considered the key swing factor in the lithium market – is down 10% since the end of June.

Peak season is coming…

In a section titled "Peak season demand coming", Morgan Stanley is points out that the third quarter (i.e., the current quarter) is associated with a seasonal peak in battery manufacturing demand. The broker also adds that additional support is being received from the Chinese government’s doubling of trade-in subsidies for electric vehicles.

Indeed, sales of EVs in China are up 31% year to date, notes Morgan Stanley, but the greater preference towards plug-in hybrids (PHEVs) – that are less lithium intensive – is hurting overall demand for lithium from China’s EV industry.

Exhibit 7: But PHEVs are gaining share, with sales up 87% YTD Source: CEIC, Morgan Stanley Research (From “Lithium Supply Reacting”, Morgan Stanley Research, 23 August 2024) (Click here for full size image)

Lithium bulls should take heart from this comment from Morgan Stanley on this item: “As prices move deeper into the cost curve and supply slows, the upcoming peak season demand could prompt price stabilisation, or even a slight recovery.”

Inventory growth slowing?

Morgan Stanley also notes that the current wall of lithium supply is only one piece of the lithium pricing puzzle. Record inventories of lithium carbonate “are still an overhang” notes the broker, but inventories at converters and battery manufacturers are showing a “slowing pace of increase”. The broker goes on to note, “downstream players starting to restock on lower prices”.

And then there’s UBS

UBS has also shared its thoughts about the lithium market in its latest update released on Tuesday titled “Lithium – Handbrake”.

The broker notes a worsening demand outlook for global EV sales predicting that global automotive battery demand will be “up to 10% lower through to 2030”. When you add in the growing trend towards PHEVs, there are “significant implications for lithium demand”, the broker says.

UBS believes the 10% decline in global EV sales by 2030 will have “a similar impact for lithium demand…these changes result in global lithium demand down ~10% to 2030” by the broker’s revised estimates.

What should investors do with their ASX lithium shares?

UBS concedes that some supply is being deferred, but so “it is not enough”. This has led the broker to mark-to-market its lithium minerals forecasts for current spot prices, and as a result, it has downgraded its 2025 and 2026 chemical and spodumene prices by as much as 23%.

While we don't observe any large-scale curtailments (yet) it is clear that the stress of low prices needs to drive production curtailment and delay/deferral of growth projects. CXO's Finniss C&M was tip of the iceberg and will likely see other shuts if spodumene prices persist around spot of ~$770/t (SC6, spodumene) for the next 1-1½ years (as we now forecast).

– UBS

EV/Lithium, page-1043

Featured News

Featured News

The Watchlist

NUZ

NEURIZON THERAPEUTICS LIMITED

Dr Michael Thurn, CEO & MD

Dr Michael Thurn

CEO & MD

SPONSORED BY The Market Online