....my assessment about lithium being in protracted hibernation wasn't wrong, and it took instos and retailers too long to see the reality of the situation.

....it was never so much about the demand and the supply.

....Fact is the Chinese EV makers are dominating the global EV trade and they are self sufficient with their own vertically integrated lithium mine supply- those mines do not have to make good margins as they are owned by the EV makers; for the Africans and South Americans, it was about providing jobs for the local people and bringing $ into their countries.

....And Western EV makers are hampered by declining market share, lack of ambition and now with Trump in charge, a loss in momentum towards decarbonisation.

....and I did tell you not to wait until the loss of exuberance/momentum before considering exiting positions.

....EVs can continue to grow and in fact grow faster at the expense of a longer winter hibernation for lithium prices.

...with a forthcoming global recession in the works, and the adverse impact of tariffs serving to raise car prices, its over for the lithium trade. Many lithium stocks IMO could lose up to half of their present values in the year ahead.

...a switch to physical Gold will save the day IMO for long suffering lithium hodlers. Time is running OUT.

Morgan Stanley gives up on lithium rebound as supply woes return

Alex GluyasMarkets reporter

Mar 4, 2025 – 4.45pm

Morgan Stanley has capitulated on its recent call for investors to dive back into the beaten-up lithium sector after another surge in supply collided with concerns about US electric vehicle demand, dashing hopes for a hotly anticipated rebound in prices.

The broker turned positive on lithium in December, tipping that production cuts would ease the oversupply of the battery metal that has plagued physical markets. It also declared prices had bottomed and equities had corrected enough for “patient investors to re-enter”, nominating Mineral Resources as its top pick. The company has since dived another 40 per cent

Lithium spodumene prices have dived 90 per cent from record levels in 2022. AP

Though producers cut production in the second half of last year because of the collapse in prices, that trend appears to be reversing this year, exacerbating the sell-off in ASX-listed lithium stocks. That has caused Pilbara Minerals to sink a further 17 per cent since Morgan Stanley turned bullish in mid-December, and IGO to dive 22 per cent.

MinRes – which has also been plagued by governance issues related to its founder Chris Ellison – and IGO shares are now trading at their lowest levels in at least four years.

“Our positive outlook for lithium looks more challenged with cost curves shifting lower, idled capacity restarting and more supply coming through,” said Morgan Stanley commodities strategist Amy Gower. “A sustainable rebound in prices looks less likely.”

Sentiment in the lithium sector was more positive in September after Chinese electric vehicle battery maker CATL suspended operations at its lepidolite mine in Jiangxi, which accounts for 6 per cent of global supply.

While Morgan Stanley assumed the operation would be shut for the rest of this year, CATL restarted operations last month despite prices sitting below its cost of production.

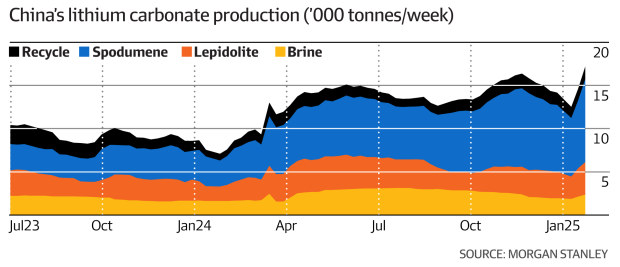

The mine is operating at a run-rate of 24,000 tonnes a year, with plans to ramp up to 36,000 tonnes. The reopening has already caused China’s domestic lithium production to surge 37 per cent since early February.

Major producer Chile is also fuelling the re-acceleration in supply, with lithium exports surging 56 per cent in January compared to the same period last year – the third-highest level on record.

The prolonged downturn in lithium prices has caused producers to aggressively cut costs. The global all-in sustaining cost for spodumene fell 14 per cent in 2024 compared to 2023 as miners streamlined operations. At the same time, there is a fresh wave of low-cost lithium supply on the horizon.

In Argentina, Eramet’s direct lithium extraction project has begun exporting and Ganfeng’s Mariana operation has started production. Sigma Lithium is on track to double its capacity by 2026, and the Manono project in the Democratic Republic of Congo is progressing faster than expected.

The combination of widespread cost-cutting and cheap lithium projects coming online is pushing high-cost producers out of the market.

“Our latest analysis suggests another shift lower in the cost curve as new supply comes through,” Gower said.

Tariff uncertainty hits US demand

Morgan Stanley acknowledged that demand for lithium had fared better than expected this year, largely driven by China. Indeed, the country’s electric vehicle sales jumped 29 per cent in January compared to last year, supported by an extension of Beijing’s trade-in scheme which rewarded consumers who traded in an old car for a new EV or plug-in hybrid with a 20,000 yuan ($4428) subsidy.

However, this was still down 40 per cent from December when sales reached a record before the expected expiry of the program.

Morgan Stanley warned that the outlook for US demand was more fragile given the potential removal of EV incentives and tariffs under President Donald Trump.

Nissan, Volkswagen and Stellantis have all delayed or cancelled US production plans recently, citing subsidy uncertainty and potential regulatory easing of EV mandates.

Morgan Stanley’s automotive team projected that global battery EV sales would grow 14 per cent in 2025 compared to the prior year, but warned that forecasts could face downside risks depending on the trajectory of sales outside of China.

....my assessment about lithium being in protracted hibernation...

Featured News

Featured News

The Watchlist

CDE

CODEIFAI LIMITED

John Houston / Martin Ross, Executive Chairman / COO

John Houston / Martin Ross

Executive Chairman / COO

Previous Video

Next Video

SPONSORED BY The Market Online