Newsletter on EV/Lithium:

If you believe in reincarnation, EV-related stocks must have done something awful in a prior life.

Most of them are suffering a miserable existence on Wall Street, and facing a near-term future that looks increasingly challenging.

As a result, I am recommending today that you exit three EV-related trades in our portfolio and re-allocate to timelier opportunities.

Partly, EV-related stocks are suffering from the widespread washout in the renewable energy sector that has caused many renewable energy exchange-traded funds (ETF) to crater 60% or more during the last three years.

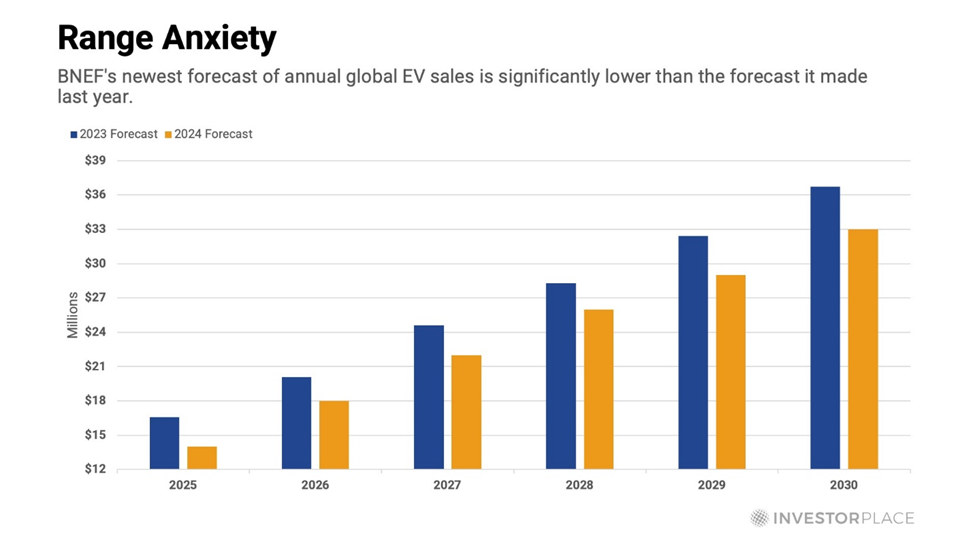

However, EV-related stocks are also suffering from sector-specific negatives – like the sudden worldwide slowdown in EVs sales growth. Bloomberg New Energy Finance has taken note of the slowdown by slashing its overly optimistic EV sales forecasts. Its newest forecast of annual global EV sales is significantly lower than the forecast it made last year.

Since shiny new Teslas and other EVs are no longer flying off of showroom floors, inventories are growing, and auto manufacturers are putting the brakes on both current and future production plans.

Volkswagen AG (VWAGY) seemed to catch a whiff of slowing EV demand last fall, when it started reducing production from its German factories, while also canceling plans to build a new $2 billion EV factory.

Bentley Motors followed Volkswagen’s lead by delaying its planned transition to all-electric vehicles for at least two years. Instead, the luxury automaker will focus on offering plug-in hybrids.

In April, Ford Motor Co. (F) announced a similar plan. The U.S. automaker said it would put some of its planned EV product launches in mothballs, in favor of delivering hybrid models.

A few weeks later, Nissan Motor Co. (NSANY) revealed it would halt plans to develop and manufacture two new EV sedan models in the U.S.

A few days after that, Nissan’s Japanese rival, Toyota Motor Corp. (TOYOF) announced it would push back the planned start of its EV production in the U.S. from 2025 to sometime in 2026.

Announcements like these have cast an artic chill across the entire EV supply chain. This chill is causing EV-related plays in the portfolio to suffer the stock market equivalent of hypothermia. They seem utterly dazed, as they stumble throughout most trading days.

The longer the chill persists, the more serious the symptoms become. The lithium market, in particular, is shuddering from the EV production slowdown.

As analysts at the investment bank, Citi observed recently…

Inflation, high interest rates, range anxiety, lack of charging infrastructure and limited product optionality has tempered global EV sales expectations, particularly in the U.S. and Europe.

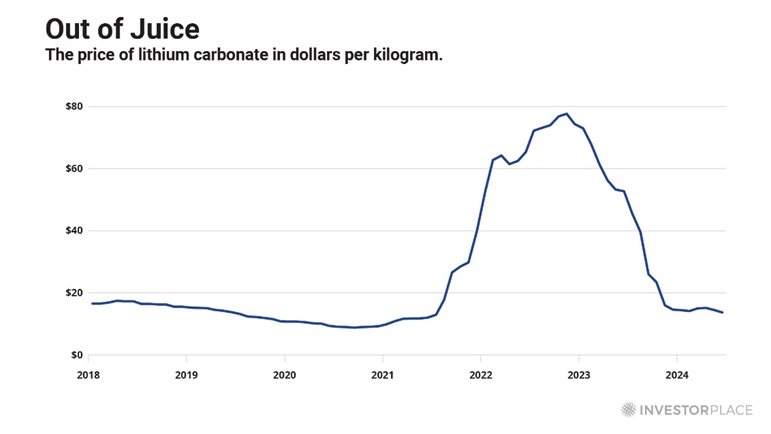

Since the EV industry consumes about 70% of global lithium supplies, the slowing growth of EV sales is very bad news for the lithium market. That’s why lithium prices have plummeted more than 80% during the last 18 months.

Hopes for a rapid recovery are probably just wishful thinking. Despite the EV-driven shock to lithium demand, the global supply continues to grow, along with widespread plans to boost supply even more in 2025 and beyond.

Contrarian-minded investors might be tempted to buy into the doom and gloom in the lithium market, rather than sell out of it at these depressed levels.

One such investor is RBC Capital Markets analyst Kaan Peker, who slapped a “Buy” rating on Arcadium Lithium plc (ALTM) this week. The intrepid analyst bases his bullish outlook on Arcadium’s plans to spend $1.6 billion to boost lithium output from 61,000 tons to 142,000 over the next three years.

Unfortunately, Arcadium is not the only lithium producer in the world that is planning to boost production. And unless pricing improves, production growth will not increase profits, it will increase losses.

Interestingly, Peker’s bullish thesis anticipates that Arcadium will generate negative free cash flow for at least the next three years. That is what a “bullish” analysis looks like in the depressed lithium sector.

To be clear, I am not throwing stones at Peker’s analysis. After all, I recommended Arcadium at nearly double today’s price and have been completely wrong. Maybe his “Buy” recommendation will produce a better result.

Lithium stocks like Arcadium could be close to becoming great contrarian trades. But at the risk of being wrong twice about the same stock, I recommend selling it and moving on to other opportunities.

The once-promising lithium market is facing daunting headwinds. Although the worst of the selloff may be over, the catalysts for higher prices might take their sweet time showing up.

To stage a sustainable recovery, the lithium market must overcome the dual threat of sub-par demand growth and excessive supply growth. Both of these threats seem highly likely.

In addition, the lithium market now faces at least two possible “Black Swan” risks – unexpected shocks that could derail a bullish narrative.

First, as Popular Mechanics reported recently…

A new study from the University of Pittsburgh and the National Energy Technology Laboratory (NETL) estimates that up to 40 percent of the U.S.’s lithium needs could be supplied by wastewater produced by hydraulic fracturing operations from Marcellus shale gas wells in northern Appalachia.

You heard that correctly; wastewater from fracking operations could potentially supply a huge percentage of projected U.S. lithium demand.

Admittedly, this technology has not yet advanced from the laboratory to the Marcellus Basin, but it could probably advance faster than new technologies typically do.

That’s because the folks who run fracking operations have both the deep pockets and the reputational incentive to bring this new technology to life. Oil companies might relish the opportunity to contribute to the “greening” of planet Earth by converting wastewater into an essential EV component.

A second possible Black Swan risk could be a Trump re-election in November. If he were to occupy the White House a second time, his new administration might reverse some of the policies the Biden administration prioritized, like funding various green energy initiatives. Trump has signaled that likelihood already.

That potential Black Swan event, if it were to occur, might not cause any serious widespread challenges for lithium producers, but it could cause difficulties for specific companies like Lithium Americas Corp. (LAC).

This hopeful lithium miner obtained a “conditional” $2.3 billion loan to help develop its Thacker Pass lithium project in Nevada. But the company has not yet received a nickel of that pledged funding.

In order to begin drawing on that loan, Lithium Americas must first satisfy certain “technical, legal, environmental and financial conditions,” according to the Department of Energy.

Satisfying these conditions could take a few more months. Therefore, the longer the funding delay lasts, the greater the risk that a Trump administration might pull the loan.

Many other companies in the renewable energy sector face similar hypothetical risks.

To be clear, I am not making any specific predictions about a second Trump administration. I am merely pointing out that the risk of withdrawn funding is probably greater than zero.

Nine out of 10 times, I want to be a buyer of down-and-out names, in down-and-out sectors. As such, I “should” be a buyer of lithium stocks and other names in the EV supply chain.

But these opportunities have become so complicated and fraught with additional risks that they fail to provide a compelling risk-reward proposition.

In the current environment, the lithium market and most EV-related plays remind me of a memorable line from the late Charlie Munger, Warren Buffet’s long-time investment partner…

At Berkshire [Hathaway] we have three buckets: yes, no and too hard.

The EV sector broadly, and the lithium market specifically, have become “too hard.” Therefore, I recommend selling EV-related plays and reallocating to better opportunities.

Newsletter on EV/Lithium: If you believe in reincarnation,...

Featured News

Featured News

The Watchlist

PAR

PARADIGM BIOPHARMACEUTICALS LIMITED..

Paul Rennie, MD & Founder

Paul Rennie

MD & Founder

SPONSORED BY The Market Online