Dex, here is a post I made recently regarding some figures for the 500MW stage. If anything, they are overly conservative regarding future NEM prices. Fair warning to the regulars that it is just a repeat, so please tune out when appropriate!

"We have rather weak figures for calculations, but if you're up for it, the figures are as follows (all figures are up for debate, are for discussion purposes only, and have been fueled by seafood, beer and plenty of wine):

The plant has been estimated to cost roughly $2B for 500MW installed capacity. I believe this to be inclusive of drilling costs, though management are understandably reluctant (and unable) to publish specific figures.

On top of this, an estimated $350M - $500M will be sunk on over 500 km of transmission infrastructure, bringing total development costs up to roughly $2.5B.

Lets put a figure of 10% maintenance downtime on the plant (a reasonably standard figure in other operating plants), giving just under 8000 operational hours. Being a non-fluctuating, base load provider, lets assume the 500MW plant runs near to capacity (I'll use a capacity factor of 0.9, giving 450MW, to satisfy any conservatives) for those 8000 hours (have separated the downtime from the C.F to be specifically conservative for this fledgling operation).

450MW x 8000 hours = 3.6 million megawatt hours.

Using this roughly derived figure of 3.6 million MWh per annum would allow us to calculate an estimated annual revenue, if only we had a magic projector for where taxes, quotas, credits and demand will take us over the next 5-10 years. Looking at current projections, and slightly exaggerating them to include the constraints being introduced for power generation, I would estimate a spot price of roughly (yes, I'm using that term a lot) $65/MWh (I would be very interested to hear other thoughts on where this price may lie), depending on who they initially market the electricity to. I feel this to be a particularly conservative estimate.

So, from here, gross revenue could be estimated at $234M per annum. Operational expenditure has been estimated at roughly $5/MWh, and fuel costs are $0/MWh, giving an operational expenditure (using the full figure of 8765 hours) of about $20M per annum.

Using these rough guides of revenue and opex, we could calculate an annual net income of $214M.

Now comes the debt facility. I have no idea how this will be structured, and what rates they will be paying. The options are too wildly variable to put anything other than a broad range of figures up for discussion. Will the company make a pro-rata offer to existing shareholders? Will any major placements be made to significant investors? How much will be financed by debt?

If the majority of the funding is via debt, then it could take up to 15 years repay the loan, if minimal funds are set aside for exploration and the development of other projects (an unlikely scenario in my opinion). More likely will be a compromise between repayment and exploration, and the shareholder's interests will be of primary concern.

The economic life of a localised project is at least 50 years, possibly ranging up to 100 years. New wells can be drilled at an ongoing expense, extending project life further. The beauty of the geothermal model is that once the large capex is repaid, the system operates at a low cost with no fuel costs, ideal for dividends and further inorganic growth.

I can see market bullishness when the idea of virtually limitless, base load, emission-free energy is shown as viable by the flow test and subsequent electron production at the pilot plant. Using that as a guide, I feel $320M undervalues a company with such potential for future earnings (~$200M/annum at a glance) and highly reliable dividends. Commodities rise and fall, but the demand for power can only increase with Australian growth.

One more here Dex, regarding the specific advantages presented by GDY

The massive temperature advantage enjoyed by GDY does not only extend to unparalleled capex reductions at the initial construction phase. Huge capital savings are also facilitated by the exceptionally long commercial life of the Cooper Basin HFR project.

Please feel free to respond with any corrections/criticism.

Taking the widely-quoted 500MW installed capacity, a comparison can be made against other projects in the sector. The 500MW system is actually a series of 50MW modules, which will be developed incrementally until the target production is met (and, as such, capacity can be readily and predictably scaled up from 500MW). Plant costs should be reasonably static across the different projects (with the exception of the Kalina Cycle, which should eventually be implemented by GDY, and attracts a higher price than off-the-shelf Rankine), though Capex will vary wildly according to geofluid temperature and flow rates.

The key driver of the differing capital costs (and the fundamental factor in GDYs *expected* very low cost/MWh) is the number of wells needed to supply production at 280C. GDY, having modeled the flow rates and temperatures, have calculated that 4 injection and 5 production (extraction) wells will be required, for a total of ~90 wells to supply 500MW. My estimate for cost/well is ~$15M (inclusive of 5 additional Lightning Rigs and larger drilling workforce working for inflated incomes) If anyone could help me tweak this figure towards greater accuracy, it would be greatly appreciated.

As it stands (all estimates are in current terms, not adjusted for inflation), roughly $1.35B of the expected $2.7B capex ($2B project cost + $0.7B infrastructure cost) is accounted for as drilling costs.

For a lower grade resource, say at 200C (the expected targets of GRK and PTR), many more wells will need to be drilled to reach the same capacity. Taking the example of GRK (PTR are pursuing the HEWI model at their flagship Paralanna project, an unproven modification of the HDR model) and assuming either company achieves the prodigious flow rates demonstrated at HAB3 (a generous assumption), power output per well will be over 50% lower. As a conservative estimate, this lower quality project will require about 10 injection and 11 production wells, which, if drilling costs remain static, will incur 230% of the capital costs of GDYs wells, at $3.1B (i.e 2.3 x 90 wells @ $15M/well = $3.105B).

Now, it's easy to see that these figures are highly dependent on the actual average drilling costs for the whole project. None of the figures used above are an accurate representation of real costs, but more of an estimate based on current projections. The figures are used to demonstrate the immediate capital advantage GDY have over any Australian competitor.

The crucial factor, once the immense initial advantage is accounted for, is resource life.

Put simply, the wells drilled by GDY will be productive for 100 years longer than the wells drilled by our previous example, GRK.

100 years longer.

That is, the particularly significant costs of drilling new wells while the depleted ones regenerate (which could take centuries) will occur far less often for GDY.

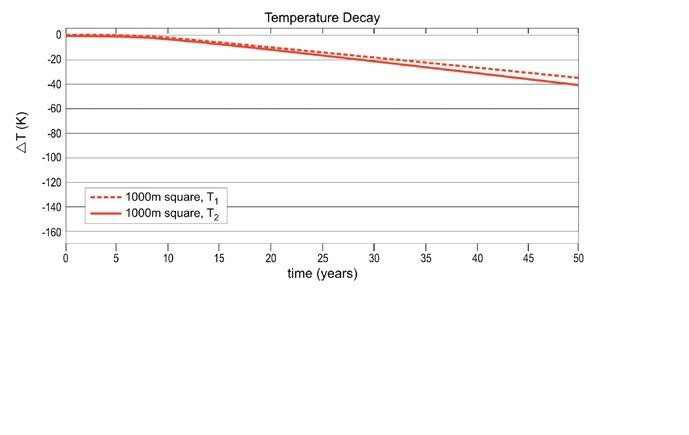

While other projects may have a commercial life of ~50 years, GDY will be able to profitably extract heat for 200% longer. According to current depletion rate models, it will take 100 years for wells spaced at 1000m intervals to drop from 280C to 200C. Replacing existing wells could incur a cost equal to the initial development cost.

For GDY, replacement will occur every 150 years @ $1.35B, for an average of $9M/year.

For GRK, replacement will occur every 50 years @ $3.1B, for an average of $62M/year.

It is this mechanism of capital advantage that will secure GDYs place as sector leader, and will ensure investment dollars are chasing quality, not speculative leverage.

RNE Price at posting:

0.0¢ Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)