Extract from Fiftyone Capital Report

May 2019 FundPerformance Update

SMALL CAPSOur smaller portfolio was all about the iron ore this month. As prices rallied to US$100/tonne a number of our positions performed very well. Champion Iron (CIA AU) has had a huge start to 2019 with the shares running from around $1 per share to now around $3. Another iron ore junior that has performed very well for the fund is Fenix Resources (FEX AU). We have recently added to this position as the market begins to appreciate that the ~$25m market cap is representative of less than 0.5x future free cash flow at spot prices. With CAPEX requirements of only $5m and the project progressing to development, this looks like a cash cow for investors once in production.

Another strong performer this month was Dubber (DUB AU) which rallied close to 50% over the month on no material new updates. We are holding an elevated level of cash now as we continue to review opportunities and remain cautious about taking larger, longer term positions in small caps.

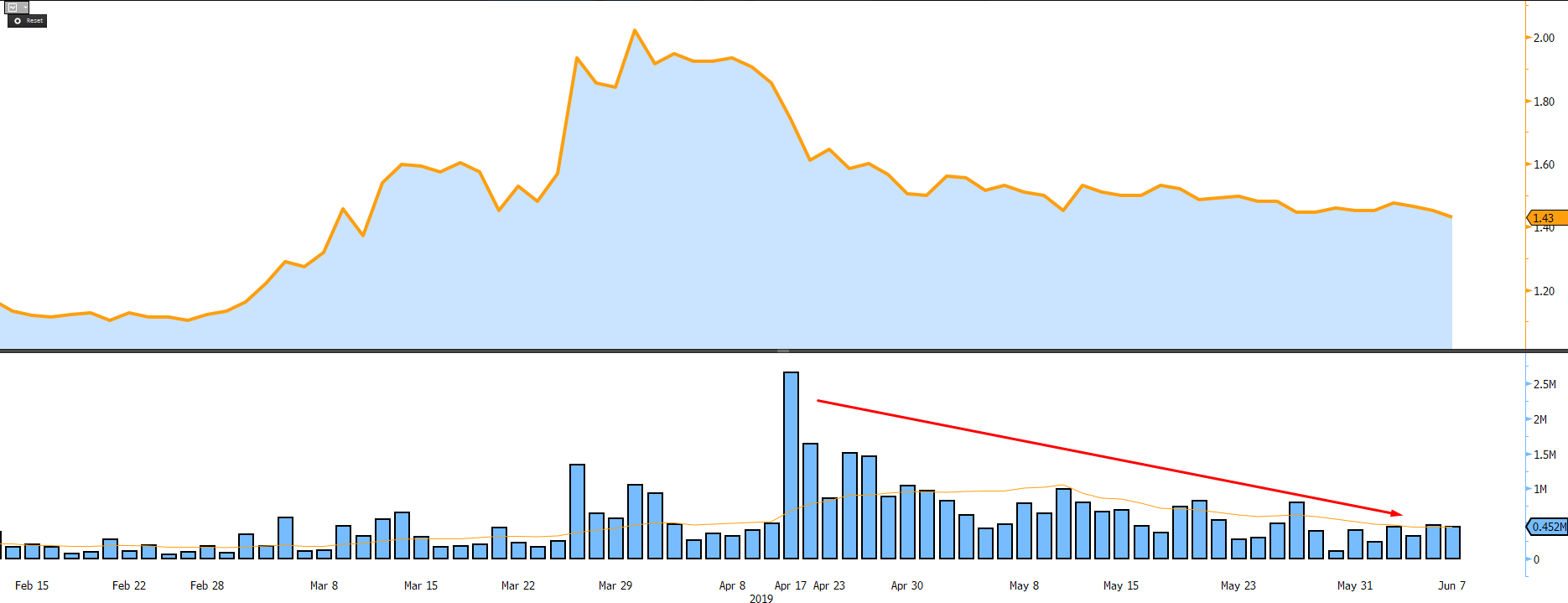

We recently caught up with Paradigm (PAR AU) for an update on how the company is progressing. The stock has continued to track sideways/down as traders flip shares from the placement. Once the placement and associated rights issue was announced we expected somewhere between 20m and 40m shares (around 10-20% of register) to turn over before the register was tight again. At the start of June (since 17th April) there has been close to 25m shares traded with a VWAP of $1.58.

When large buyers emerge, we would expect that shares of PAR should begin trending higher again given the turnover witnessed since the placement. Volumes have started to dry up as less sellers are willing to part with their stock at current prices. Given there are no large institutional owners with a >5% holding it seems only a matter of time before they begin to creep onto the register. To own a position greater than 5% it will require buying close to 10m shares on market. Now that the company is fully funded, all further accumulation will need to be done on market.

Volumes since the placement have been declining indicating less and less willing sellers

Our view remains that Paradigm is not a widely understood or widely owned company. As a result, the stock trades at a Market Cap of $275m and cash of over $80m (EV below $200m) which as we outline below drastically undervalues the business. There seems to be a clear disconnect between what the market is saying, and what the data is saying. Such disconnects won’t last and it’s likely a pharma deal validating our views could be the catalyst to see a material re-rating in the share price.

By way of example, the company recently reported successful results for their Ross River Phase 2A safety trial. With such a small sample set it was pleasantly surprising to see such strong results with near remission being seen in the people treated with iPPS. The next step is likely to start discussions with the US department of defence (DoD) who could start to purchase iPPS from Paradigm to treat service men and women who are suffering with chikungunya (CHIKV).

The best case is the DoD are happy with the results and safety and order anywhere from $1m - $5m worth of product to begin treatments. Worst case, they want to run another trial in CHIKV and will either fund or co-fund this trial (which is not a bad outcome). There are thousands of service men and women with CHIKV and no current treatment. Our estimates are a course of treatment would cost between $3000 - $5000 per treatment ($3-$5m per 1000 people). We rank the probability of purchasing before a trial at 50/50 odds – Given the strong safety profile and lack of alternative treatments there is a good chance they move forward with purchases. This is something the market seems to be completely overlooking.

Just by way of comparison and example, PolyNovo (PNV) has recently been granted a contract from the DoD to purchase their product NovoSorb. PNV’s current revenue is $5.7m (although now ramping up to >$1m per month) yet has a market capitalisation of $852m or EV around $830m. Given Paradigm is less than $200m EV and could have similar revenue from their ChikV indication as early as July/Aug it looks very cheap by way of comparison (noting this is only for their ChikV/RR indication).

Depending how things progress, this indication could easily justify Paradigms existing market cap. A deal with a pharma could be in the range of US$100m - US$200m (AUD $142m - $285m) or materially higher should the DoD also start purchasing and using the product. Given the safety profile and quality of the results Paradigm may also apply for provisional approval in Australia to treat Ross River. Again, near term revenue the market doesn’t seem to believe is possible. The disconnect between commercial reality and the market pricing will not last.

The big upcoming catalysts are likely the filing of the IND with the FDA. Upon a final trial design for OA and MPS its likely big institutional investors and big pharma are going to start taking a serious look at the company. We continue to bang the table as any deals for OA or MPS are going to be materially higher than the current market capitalisation of the company. The upfront of these deals are likely to be around 10-20% of total deal size and could add significantly to Paradigms cash balance.

Given Paradigm now has 3 indications that look highly likely to be commercialised it won’t be long before the stock re-rates to reflect the future revenues. Any pharma deal could see a substantial upfront component which would further de-risk the company. It’s an extremely exciting 12 months ahead during which time we are hopeful:

A pharma deal will be done for OA/MPS

DoD purchasing for RR/ChikV & potential Pharma Deal

TGA provisional approval granted for OA and first revenue in Aus

MPS patients being treated successfully under SAS

IND’s filed and trials underway for MPS & OA (with improved trial design)

NFL Players treated and excellent press/results seen

The simple fact is that Paradigm has a safe and effective treatment for diseases that have no existing effective treatments. While not commercialised yet, it certainly looks like they will get there from the results released to date. When they do, the company will have a market capitalisation that measures in billions. The commercial reality is far better than what the market is currently pricing. Making this one of the most asymmetric opportunities we have identified on the ASX.

Fiftyone Capital Update

Add PAR (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

27.5¢ |

Change

-0.010(3.51%) |

Mkt cap ! $96.19M | |||

| Open | High | Low | Value | Volume |

| 30.0¢ | 30.0¢ | 27.0¢ | $45.01K | 159.2K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 3 | 17942 | 27.0¢ |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| 28.0¢ | 9634 | 1 |

View Market Depth

| Last trade - 16.10pm 02/05/2024 (20 minute delay) ? |

|

|||||

|

Last

27.5¢ |

Change

-0.010 ( 3.51 %) |

||||

| Open | High | Low | Volume | ||

| 29.0¢ | 29.0¢ | 27.0¢ | 41613 | ||

| Last updated 15.59pm 02/05/2024 ? | |||||

| PAR (ASX) Chart |