https://seekingalpha.com/article/4270462-mei-pharma-time-reload-key-support-level

MEI Pharma: Time To Reload At Key Support Level

Jun. 16, 2019 8:15 AM ET

About: MEI Pharma, Inc. (MEIP), Includes: TGTX

Kenneth Pittman

Long only, value, biotech, healthcare

Summary

MEI Pharma is back at support levels where there has been significant buying interest - including a large private placement in 2018 that stoked a rally.

The MEI Pharma pipeline is progressing well and could yield additional partnerships.

ME-401 in particular is now getting the attention that I predicted in my previous article.

Overall, MEIP is back at levels where the risk/reward balance is very compelling and makes it a buy again.

Review of Stock Price Since My Last Article

I last wrote about MEI Pharma (NASDAQ:MEIP) on July 10th, 2017, with an article titled "MEI Pharma: Double Trouble Or Double Double." At the time of the article, the stock was trading at $2.76 a share and had already doubled from $1.40 a share early in 2017. The market cap at that time was about $104 million. In my article, I concluded that the chances of a "Double Double" to $5.60 a share within a year were better than the chances of a significant drop. Was I correct? Well, yes and no. On the negative side, the stock never actually made it to $5.60. It peaked at $5.14 on June 6, 2018 (11 months after my article). Still, this represents the potential of up to an 86% idealized gain. However, from my recommendation to the lowest level since ($1.89 on 4/9/18), there was a loss of 31.5%. Had an investor bought near the June 6th peak and sold at the Christmas 2018 low of $1.92, then they would have had a worst-case 63% loss.

While the stock price never actually doubled, it came closer to doubling than a 50% loss. In addition, the market cap more than doubled in that time period and remains significantly higher than it was at the time of my last article (despite the stock price being lower). This is largely due to a private placement that occurred on May 14-16, 2018. That private placement added over 33 million shares at $2.273 each along with the potential of 16.5 million additional shares through warrants at $2.54 each. Immediately prior to this placement, the company had a market cap of about $91 million and about 37 million shares. Overnight, the share count and market cap almost doubled. The confidence displayed by those involved in the private placement then stoked a stock rally to the $5.14 peak less than a month later. At that point, the market cap had gone from $91 million before the placement to $348 million less than a month later.

Since that peak, the stock price plummeted to a low of $1.91 (market cap $137 million), recovered to $3.32 (market cap $237 million), and now sits at $2.45 as of 6/14/19 (market cap $175 million). The current share count is about $71.3 million, indicating that the majority of the warrants from the private placement have not been exercised (which is also reflected on the company's last quarterly report). I would suspect, but cannot verify, that limitations on those warrants prevented them from being executed during the period immediately after the placement when the stock price was significantly higher than the warrant price. Currently, the stock price sits 9 cents under the warrant price (and 18 cents over the private placement share price). Without negative news or the need for further dilution, I'd expect this area to act as a reasonable floor for the stock price. It previously acted as some support prior to the December low - and the stock quickly recovered to around this level after the low.

Source: Yahoo Finance

Ultimately, it matters more where the stock is going rather than where it has been. Given some level of support at these levels, the question becomes if the pipeline still has the potential for significant upside.

MEI Pharma's Pipeline is Progressing Well Including Partnerships

MEI Pharma has not had any major setbacks in its pipeline since my last article in July 2017. In general, it has progressed with all elements of its pipeline in both phase and strength of partnerships. The only potential knock on the pipeline progression is that the company has not moved studies along quite as fast as some investors would like.

Pracinostat

MEI Pharma's lead compound is pracinostat, an oral histone deacetylase (HDAC) inhibitor, which is being investigated in acute myeloid leukemia (AML) and myelodysplastic syndrome. The AML study is in Phase 3 and the MDS study is currently in Phase 2. MEI is fully partnered with Helsinn Group, a Swiss-based private company, for the development of pracinostat. As part of the agreement, Helsinn pays ALL of the development costs. MEI Pharma is entitled to total milestone payments of up to $444 million, as well as tiered royalties that begin in the mid-teens. Helsinn has in turn made an agreement with Menarini, an Italian company, for the commercialization of pracinostat. MEI Pharma would owe a portion of its milestone payments and royalties to the company it bought pracinostat from originally.

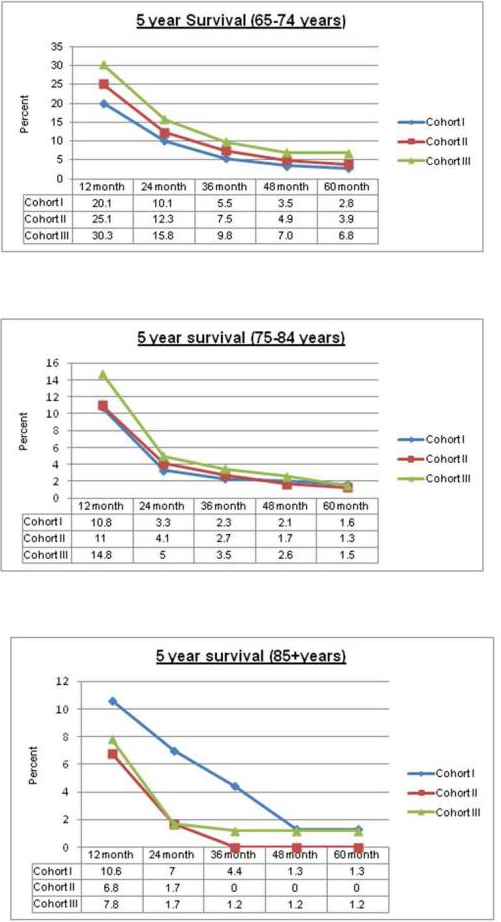

The major development with pracinostat since my last article was the initiation of the Phase 3 study in AML. This study is targeting patients over 75 years old with newly diagnosed AML or who are unfit for intensive chemotherapy. Of note, the average age of diagnosis for AML is 67, and there are many AML patients who are over 75. The survival rate for AML patients <60 is 35-40%. The survival rate for older AML patients is usually under 15%. The 500-individual study will assess overall survival of patients taking pracinostat with azacitidine vs. azacitidine alone. In a previous Phase 2 study, pracinostat with azacitidine was studied in individuals over 65 at diagnosis AND ineligible for standard chemotherapy. In this group, pracinostat plus azacitidine showed a complete remission rate of 42%, one-year overall survival of 62%, and a median overall survival of 19.2 months. A review of pooled data on AML survival at various ages shows how impressive this is compared to the norm (the charts that follow are for males, but the figures are similar for females).

Source: Cancer article - 2013 Aug 1; 119(15): 10.1002/cncr.28129

In addition to the AML study, the company is progressing in Phase 2 of the pracinostat study in MDS. Helsinn and MEI Pharma published encouraging interim results at ASH in December 2018 that showed a 9% discontinuation rate vs. 36% complete response rate at 45mg. This represented improvement in the discontinuation rate vs. an earlier Phase 2 study at 60mg. Phase 2 results including one-year survival and response rates should be available near the end of 2019. I would expect that this data will be presented at ASH 2019.

ME-401

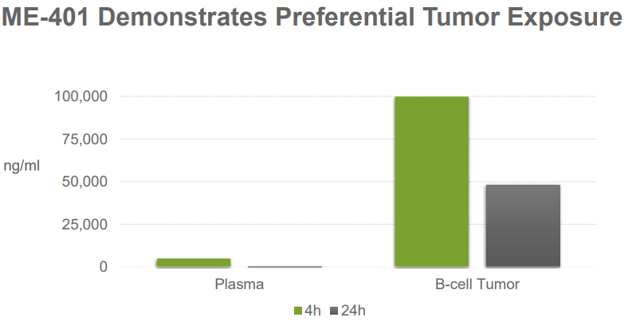

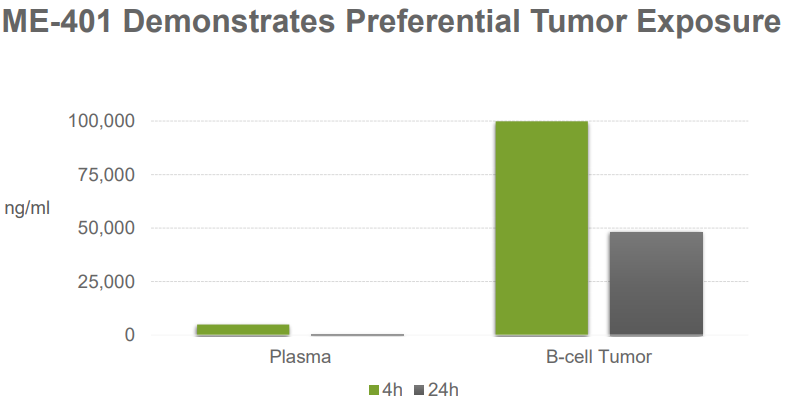

In my previous article, I indicated that I was even more bullish on ME-401 as part of MEI's future than I was on pracinostat. Even though pracinostat has advanced well, I remain more bullish about ME-401 for multiple reasons. As I covered in my previous article, ME-401 is a next-generation PI3K delta inhibitor. Compared to the current PI3K delta inhibitors, ME-401 is more selective and appears to have an improved therapeutic window. To illustrate this, compare plasma levels vs. levels in a B-cell tumor:

Source: MEI Pharma April 2019 Investor Presentation, Slide 12

ME-401 has had significant forward progress since my last article as outlined below:

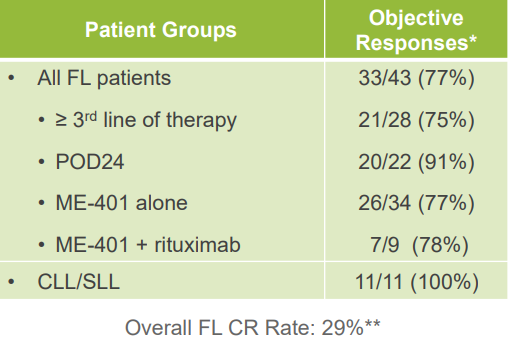

- Positive Phase 1b Data - ME-401 completed its Phase 1b study in June 2018. In this study, it demonstrated a 90% objective response rate in relapsed or refractory follicular lymphoma, chronic lymphocytic lymphoma, and small lymphocytic lymphoma (FL, CLL, and SLL). In particular, the 86% response rate in relapsed and refractory follicular lymphoma was quite impressive. The median duration of response has not yet been reached as of the last investor presentation.

Source: MEI Pharma April 2019 Investor Presentation, Slide 13

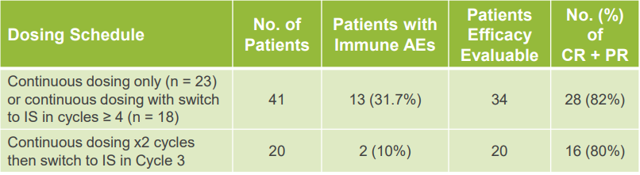

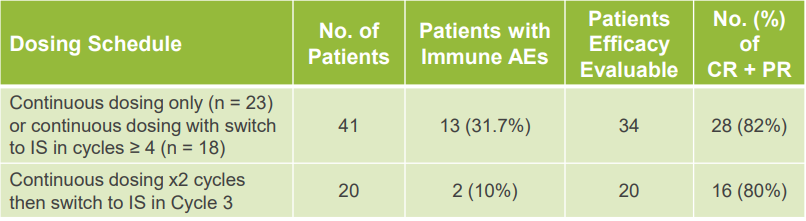

The Phase 1b study also showed an improved tolerability profile compared to current PI3K delta inhibitors - particularly with intermittent schedule dosing. Efficacy remained similar with intermittent schedule dosing vs. continuous schedule dosing.

Source: MEI Pharma April 2019 Investor Presentation, Slide 14

The overall rate of colitis was 6%, neutropenia was 10%, and liver enzyme (AST/ALT) elevation was 6%. This compares very favorably to other PI3K delta inhibitors. From examining the prescribing information for Zydelig as well as the studies of the other PI3K delta inhibitors, these side effects are often 20% or more. AST/ALT elevation and colitis typically each occur in 20% of Zydelig patients. Colitis was found in 19% of PX-866 patients. Buparlisib had 40% AST/ALT elevation, 34% colitis, 43% hyperglycemia, and 26% depression in a 2015 study. Alpelisib has a 47% rate of severe colitis in a 2016 study. Severe neutropenia occurs in 40% of Zydelig patients and was found in 44% of PX-866 patients. Copanlisib (Aliqopa by Bayer (OTCPK:BAYZF)) had hyperglycemia in 41%, hypertension in 24%, neutropenia in 24%, and lung infections in 16% according to a review article.

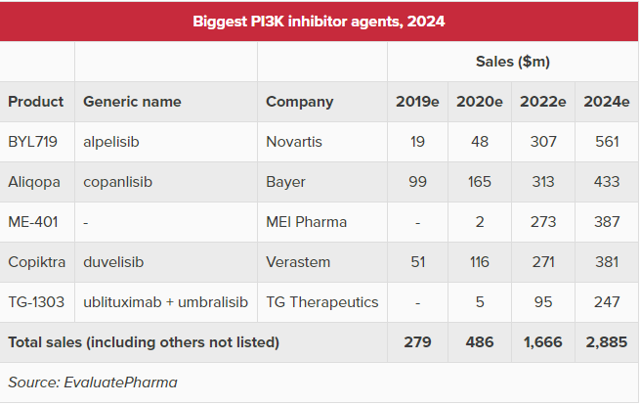

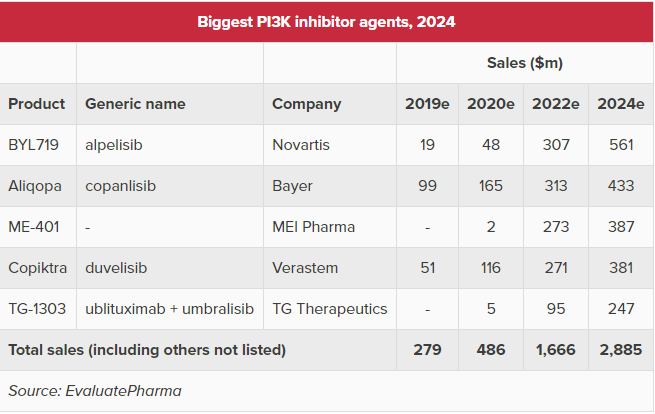

Of those I investigated, only TG Therapeutics' (TGTX) umbralisib was comparable to MEI-401 in terms of rates of neutropenia, colitis, and liver enzyme elevation. Umbralisib showed neutropenia in 13%, AST/ALT elevation in 10%, and no colitis in a recent study. TG Therapeutics is pursuing umbralisib in Marginal Zone Lymphoma, Follicular Lymphoma, and CLL. Umbralisib is currently ahead of MEI-401 in development and represents the primary competition for next-generation PI3K delta inhibitors. Despite this, EvaluatePharma is projecting ME-401 to outsell umbralisib by 2022 as shown in the following graphic from their article:

While TGTX may be a little closer to revenues and has a somewhat deeper pipeline than MEIP, I'm not sure that there is enough difference to justify a market cap that is over 3x larger (as it is currently). I don't necessarily believe that TGTX is overvalued - I make the comparison mainly as evidence that MEIP may be undervalued.

- Partnership with BeiGene (BGNE) - In October 2018, MEIP and BGNE announced a partnership to evaluate the combination of ME-401 and BeiGene's zanubrutinib, a BTK inhibitor, for the treatment of patients with B-cell cancers. This partnership allows the companies to split the cost of studies where a combination of a PI3K Delta Inhibitor and a BTK inhibitor would be an investigational benefit. Details of potential studies of this combination have not yet been released.

- Partnership with Kyowa Hakko Kirin Co., Ltd. (OTCPK:KYKOF) (Tokyo:4151) - In November 2018, MEIP and Kyowa Hakko Kirin announced a partnership for the development and commercialization of MEI-401 in Japan. As part of this partnership, MEI Pharma received a $10 million up-front payment and will be entitled to up to $87.5 million of additional milestone payments and tiered double-digit royalty up to the mid-teens.

- Intent to Commercialize as Monotherapy - In the August 2018 earnings call, CEO Daniel Gold was very excited about MEI-401. This is also reflected in the fact that it is now the first pipeline drug it covers in its investor presentation. The company indicated that it has discussed a monotherapy accelerated approval pathway for relapsed/refractory follicular lymphoma with the FDA and has designed its current study to potentially pursue this pathway. Dr. Gold indicated that the company is working on plans for independent commercialization (while not ruling out partnerships)

ME-344

MEI Pharma is continuing to develop its mitochondrial inhibitor, ME-344, in HER2- breast cancer. The company recently published clinical results at ASCO showing biologic anti-tumor activity through significant reduction of Ki67. Ki67 is a measure of cell proliferation that is significantly correlated with tumor response. Among the most significant results from this is this note: "In ME-344 treated patients, mean relative Ki67 decreases were 23% compared to an increase of 186% in the bevacizumab monotherapy group (P < 0.01)." This study will likely support advancement of ME-344 to Phase 2 studies.

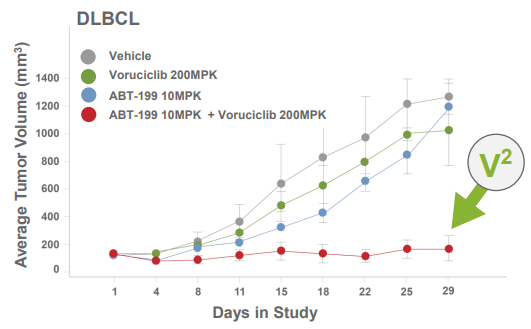

Voruciclib

Voruciclib is a CDK9 inhibitor that was added to MEI Pharma's pipeline since my last article. The company has shown evidence that voruciclib could help venetoclax (Venclexta) by inhibiting MCL1. MCL1 is an anti-apoptotic protein that prevents cell death, which is not a desirable attribute when it comes to cancer cells. Pre-clinical studies have shown improvement in tumor volume with the combination of these two drugs - as seen in the figure below:

MEI Pharma will be presenting a Phase 1b study of voruciclib in combination with venetoclax later this year (this could also be at ASH in December).

Potential Risks for MEI Pharma

Like most biotech companies, MEI Pharma does present several risks. The most significant risks are as follows:

- Risk of failure of pracinostat or ME-401 studies - While this seems unlikely (especially for ME-401 in my opinion), weak or poor results from a study would be devastating for MEI Pharma's stock. Failure of either one of these drugs (especially a failure that results in dropping the compound from the pipeline) could lower the potential market cap by about 40% in my estimation. I would assign fairly equal weight to either of the two drugs at this point. While pracinostat is further in the pipeline and success is more priced in as a result, ME-401 likely represents larger revenue potential for the company.

- Risk of narrowing target population for pracinostat - While the company currently maintains a fairly large potential patient group for the drug, the results of the Phase 3 study could narrow the target patient population if outcomes were different for over 75 group vs. the unfit for intensive chemotherapy group. This could potentially decrease the milestone payments and/or royalties due to MEI Pharma.

- Risk of previously unidentified side effects with ME-401 - The major case for ME-401 being superior to currently available treatments is based on an improved side-effect profile. If a significant side effect showed up in larger studies that was not seen in earlier studies, then it would reduce the marketability of the compound and thus impact potential revenues

- Risk of dilution - Dilution is always a risk for small biotech companies. While MEI Pharma currently has a solid cash position that should last 6-7 quarters, increased R&D expense could accelerate that. If MEI needed to dilute (especially on the open market) in order to raise additional capital, then the stock would likely take a hit in price. However, this could represent an excellent buying opportunity (as the private placement dilution did in 2018).

- Competition from TGTX and larger companies - Competition within the PI3K inhibitor space could result in discounting programs that reduce the top and/or bottom lines for MEI if/when ME-401 makes it to the market

- Congressional/government price controls - Biotechs currently are facing unprecedented pressure from both sides of the political aisle regarding pricing. This could lead to price-controlling legislation that reduces potential revenues. As MEI Pharma is mid to late stage in development, this may not be offset by any reductions in development cost that could come with this legislation

Conclusions

MEI Pharma has advanced its development across the pipeline since my last article. The company has had generally positive data in all of its pipeline compounds and also established some additional partnerships. The stock price and market cap surged within the one-year target after my last article, but have now returned closer to two-year lows (especially with regards to the stock price). The slide in share price and market cap was more fueled by a lack of positive major study surprises and general sector weakness rather than any significant poor data. As a result, the stock price is back to the range where the significant private placement was completed in 2018.

As long as there are no major congressional/government headwinds, I expect that the next 12 months will be positive for MEI Pharma. I believe that ME-401 remains the largest potential source of upside. While the company has stated intentions to independently commercialize ME-401, it could be a prime target for partnership offers. ME-401 could also be the catalyst for a buyout offer by any large pharmaceutical company looking to bolster their oncology pipeline.

As a result of all of this, I again predict that the likelihood of a double (to $4.90 from current price) is much more likely than the likelihood of a 50% decline within the next year.

https://seekingalpha.com/article/4270462-mei-pharma-time-reload-k...

Add to My Watchlist

What is My Watchlist?